On April 13, 2026, President Trump signed into law the Small Business Innovation and Economic Security Act, reauthorizing the Small Business Innovation Research (SBIR) and Small Business Technology Transfer (STTR) programs. See our prior alert here. Because of the significance of these programs to small businesses and their ability to sell new and innovative solutions to the federal government, here is a refresher on some of the rules small companies should be aware of before applying for an SBIR or STTR contract.

Background. The SBIR and STTR programs require certain federal agencies to set aside a portion of their research and development budget exclusively for U.S. small businesses to stimulate technological innovation while creating pathways to commercialization. Known as America’s Seed Fund, the programs are an attractive opportunity for startups and small businesses because they offer non-dilutive funding. Eleven agencies have an SBIR program and five have a STTR program.

Both programs consist of three phases. Phase 1 is the concept development phase. Awards are currently valued at up to $323,000 and the period of performance is no more than 6 months. Phase II consists of further research and development activity and prototyping based on the Phase I results (although in some cases there can be a Direct to Phase II, also known as D2P2/DP2). Phase II contracts can last 24 months and are valued up to approximately $2 million. Phase III derives from, extends, or completes the effort begun in Phases I and II, potentially as a commercial application. Phase III contracts have no ceiling limits, and notably are not reserved for small businesses.

Eligibility Criteria. Not all small businesses are eligible for an SBIR/STTR award, regardless of the merit of their ideas. To participate in either program, a company must:

- be organized for profit;

- have a place of business in the U.S.;

- have less than 500 employees; and

- be more than 50 percent owned and controlled by U.S. citizens, permanent resident aliens, or other U.S. small businesses (that themselves are directly more than 50 percent owned by U.S. citizens or permanent resident aliens).

The SBIR/STTR rules can present traps for companies with complex ownership structures and investors. In other words, you may consider your company a small business, and it might have fewer than 500 employees, but it might be ineligible for an SBIR or STTR contract because of issues involving ownership, venture capital operating companies, foreign ownership, and affiliation. Small companies that certify they are eligible for SBIR/STTR funding when they are not, risk not only nonselection for award but also contract termination, suspension and debarment, and liability under the False Claims Act.

Below are scenarios that can jeopardize an innovative small company’s eligibility to receive SBIR/STTR funding or to continue receiving funding due to post-SBIR/STTR award transactions such as a merger or acquisition or a new funding round. For purposes of the below, the company seeking SBIR/STTR awards will be referred to as SBIRCo, natural person means an individual, and ParentCo means the corporate entity that owns a SBIRCo.

Direct Ownership

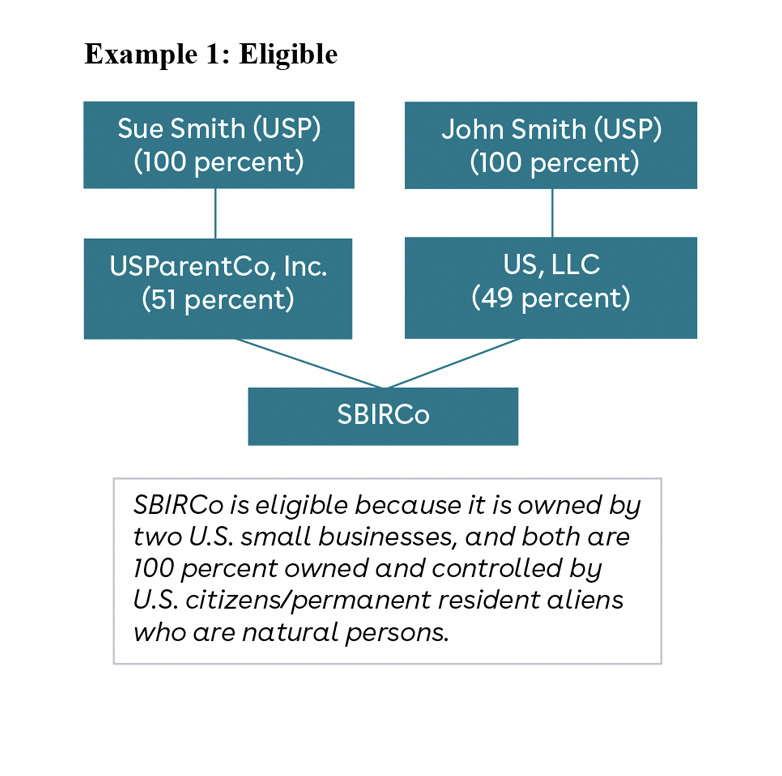

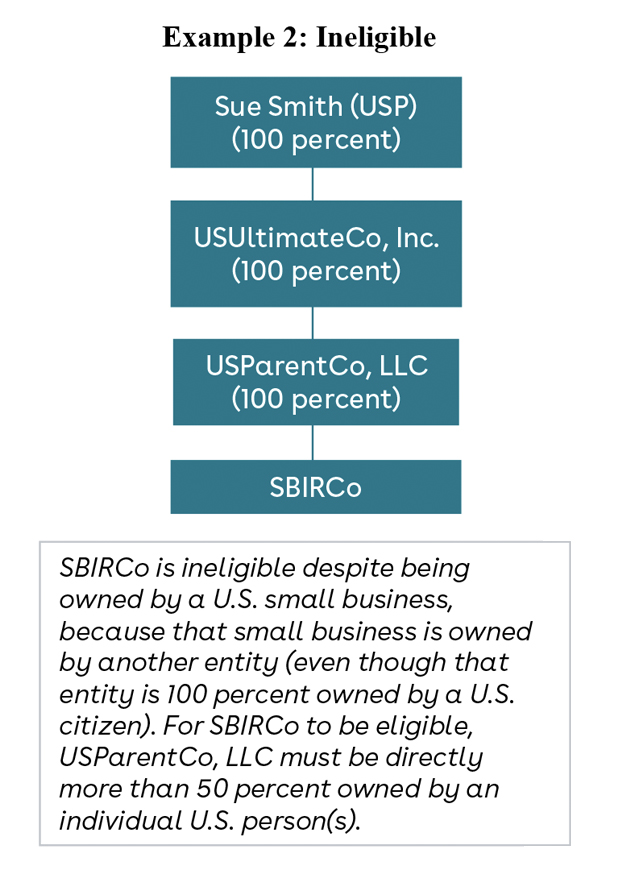

1. Ownership: SBIRCo cannot have more than one layer of corporate ownership. Many SBIRCos are subsidiaries of other companies, which as noted above, is permissible so long as the parent company is a U.S. small business that is directly owned more than 50 percent by U.S. citizens or permanent resident aliens (U.S. persons). However, the SBIR/STTR regulations limit further corporate ownership. SBIRCo’s parent must be owned by a natural person. Thus, it would be problematic for SBIRCo to be owned by small ParentCo where ParentCo is owned by UltimateCo (even if UltimateCo were small and owned by a U.S. citizen individual).

Takeaway: Before applying for an SBIR/STTR opportunity, ensure that there is no more than one layer of corporate ownership. Also, review any merger/acquisition or investment activity after receiving an SBIR/STTR award that adds a second layer of corporate ownership above SBIRCo that could impact continued eligibility.

|

|

|

2. Control: stock options and convertible securities. Investors in SBIRCo might hold outstanding stock options and/or convertible securities that if exercised, would increase their equity share in SBIRCo to more than 50 percent. The SBIR/STTR rules, with few exceptions, give “present effect” to such options and convertible securities and treat them as having been exercised to determine where ownership and control of the company resides. If a large business or foreign entity owns those options or convertible securities that if given present effect would make them the majority equity holder, SBIRCo might not be eligible.

Takeaway: When determining ownership and control, do not overlook giving present effect to assigned but unexercised securities.

Venture Capital Operating Company

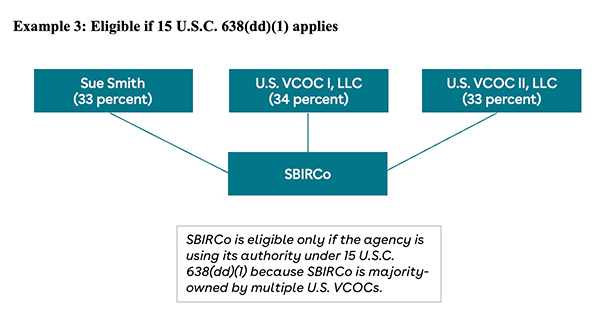

3. Ownership: venture capital operating company (VCOC). Some SBIRCos are portfolio companies of VCOCs or receive investment from multiple VCOCs. To be clear, not all venture capital funds are VCOCs. A VCOC is a fund in which at least 50 percent of the fund’s assets are invested in operating companies in which the fund has direct contractual management rights. SBIRCos thus should make sure to understand when taking on investment from venture capital funds whether they are VCOCs.

When multiple VCOCs invest in SBIRCo, and collectively own more than 50 percent of SBIRCo, the rules can restrict eligibility. SBIRCo is generally ineligible for SBIR awards should multiple VCOCs collectively own more than 50 percent. SBIRCo can be eligible if the awarding agency has and uses authority under 15 U.S.C. 638(dd)(1). It is therefore critical for an SBIRCo more than 50 percent owned by multiple VCOCs to confirm the topic and solicitation provided that the agency is using this statutory authority in making an SBIR award. Currently, only the following agencies are using this authority:

- Department of Health and Human Services (Centers for Disease Control and Prevention, and the National Institutes of Health)

- Department of Energy (Advanced Research Projects Agency)

- Department of Defense (Defense Advanced Research Projects Agency)

- Department of Defense (Department of the Navy)

- Department of Defense (United States Air Force)

- Department of Defense (Army)

- Department of Education

Takeaway: SBIRCos that are more than 50 percent owned by multiple VCOCs must also confirm the agency is awarding the contract using 15 U.S.C. 638(dd)(1) authority.

Affiliation

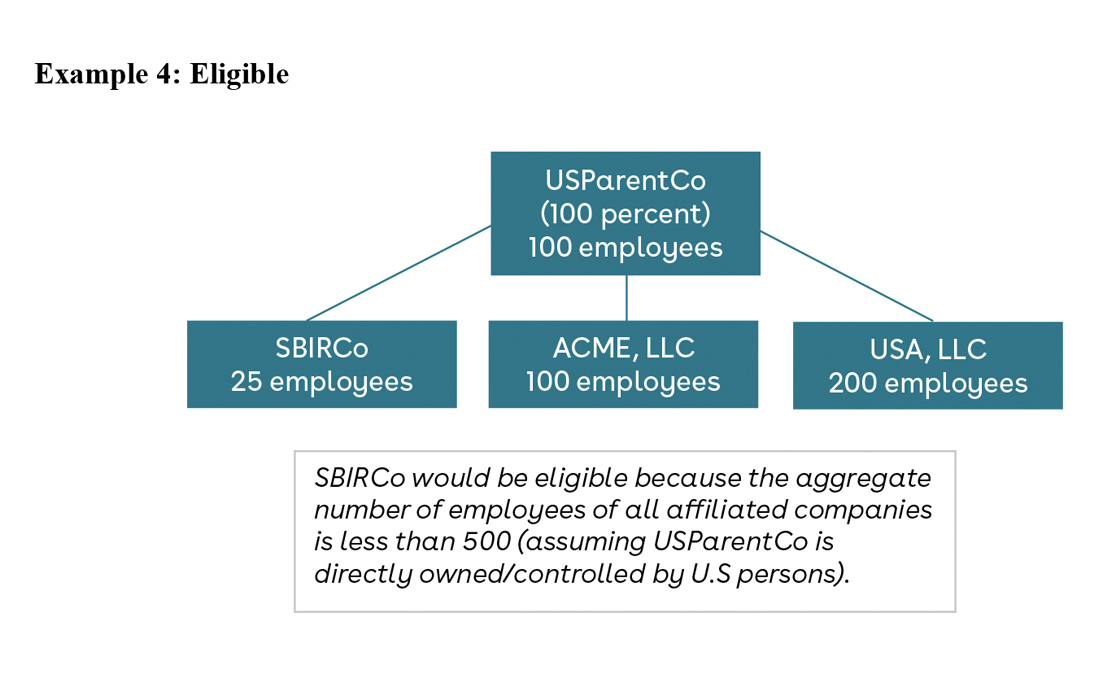

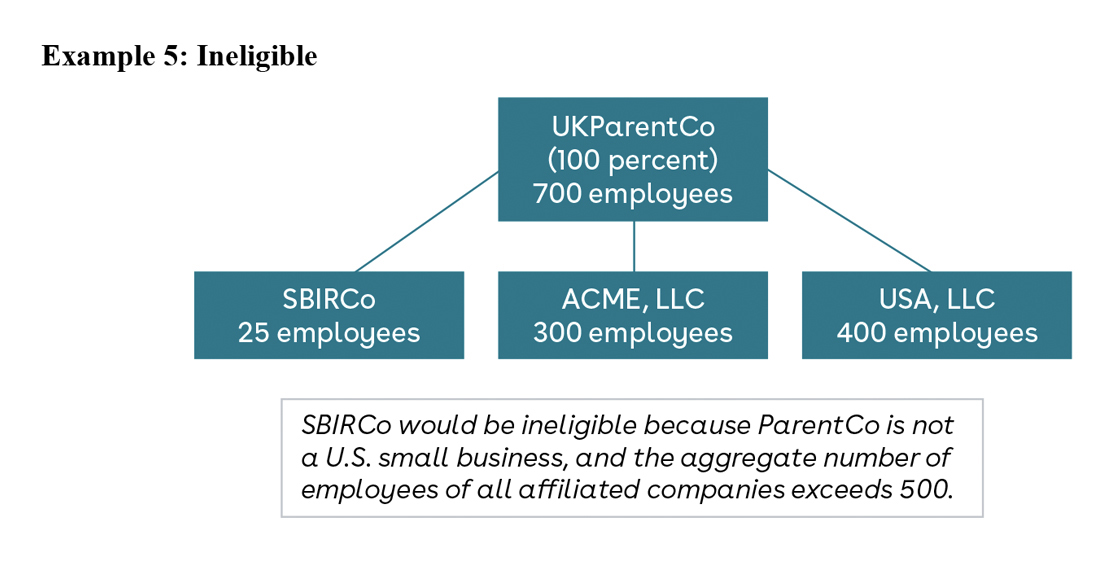

4. Affiliation: employee count of parent and sibling companies. SBIRCo might be one of multiple subsidiaries under a ParentCo. When determining whether SBIRCo has less than 500 employees, the SBIR/STTR rules look to see whether SBIRCo is affiliated with any other companies. Affiliation exists when one company controls the other, or a third party controls them both. If there is affiliation, the 500-employee limit can include the employees in SBIRCo’s parent company and the parent company’s other subsidiaries.

Takeaway: Review SBIRCo’s ownership structure for affiliation prior to submitting an SBIR/STTR application. Though SBIRCo may have 25 employees, if the small business ParentCo has more than a 50 percent ownership interest in each of three other companies, and those companies each have 200 employees, the government could find SBIRCo has more than 500 employees.

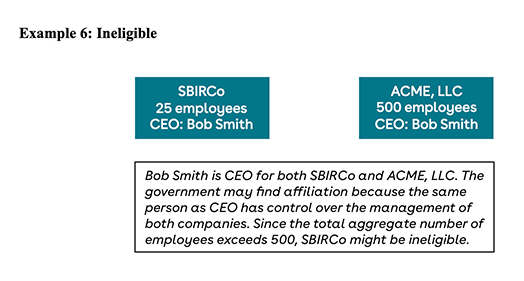

5. Affiliation: common management. Affiliation can also exist when there is common management of two firms. Often, the CEO, president, or managing members of SBIRCo might serve in a position of control or management of another business entity. The SBIR/STTR rules may find both companies affiliated in this situation and count the number of employees for both companies toward the 500-employee maximum.

Takeaway: Avoid having SBIRCo senior management or board members who serve in a similar role in another company.

Foreign Ownership and Control

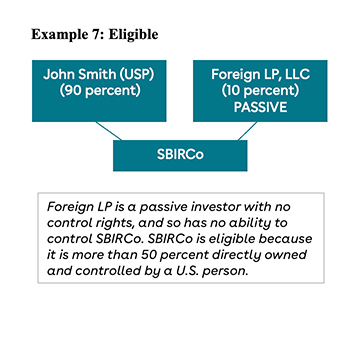

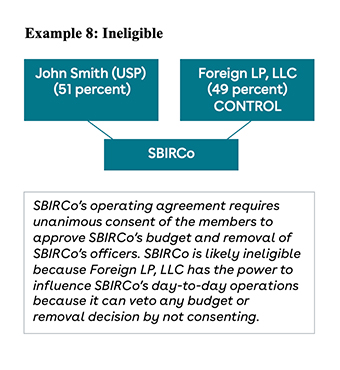

6. Control: foreign owner or investor has voting rights influencing company actions. Eligibility requires that both ownership and control reside with U.S. persons. Therefore, even if a foreign holder is a minority investor, if the operating agreement, by-laws, or shareholder’s agreement gives that foreign investor the ability to block actions such as sale/purchase of high valued property, annual operating and capital expenditure budgets, or incurrence of high value debt, the SBIR/STTR rules could consider the foreign equity owner as having control of SBIRCo under these circumstances, making SBIRCo ineligible.

Takeaway: Before applying for an SBIR/STTR opportunity, see if governance documents give a non-U.S. person the ability to determine the outcome of company actions. Before accepting foreign investment, review terms of the certificate of incorporation and any investor rights agreement that allow a foreign investor to decide, prevent, or otherwise influence actions impacting SBIRCo’s operations.

|

|

|

Final thoughts. SBIR/STTR eligibility is not always straightforward, but it is a requirement to which SBIRCos must certify when receiving funding awards. The eligibility rules, and certification requirement, apply at the time of award for both Phase I and Phase II. Moreover, some agencies may require SBIRCo to recertify continued eligibility at other points in the award lifecycle. The SBIRCo therefore might be eligible at the time of a Phase I award, but can lose that eligibility before applying for Phase II due to any of the scenarios discussed above. SBIRCos should review the SBIR/STTR rules when, among other things, raising equity, taking on debt, considering a merger or acquisition, and having foreign nationals serve as board members or company officers. The rules can be complicated and cause unintended consequences for what might otherwise be a typical company transaction consistent with its strategic objectives. Improper certifications can lead to contract terminations, government investigations and/or liability under the False Claims Act.

The above scenarios are only some areas companies should be mindful of when seeking SBIR or STTR opportunities. There are more. For further help understanding the SBIR and STTR rules, contact Wilson Sonsini’s Government Contracts attorneys.