|

From the WSGR Database: Financing Trends for Q1 2018

For purposes of the statistics and

charts in this report, our database

includes venture financing

transactions in which Wilson

Sonsini Goodrich & Rosati

represented either the company or

one or more of the investors.

|

While venture financing valuations and deal

sizes were down in the first quarter of 2018

from the record-breaking levels of 2017,

they remained high by historical standards.

In Q1 2018, the percentage of up rounds

for Series B and later financings declined,

and median pre-money valuations and

amounts raised in Series B and later

financings fell moderately. However, in Q1

early-stage financings, there were slight

increases in median pre-money valuation

and amount raised. Notably, and consistent

with what has been reported elsewhere,

deal counts continued to decline in Q1

2018, following a trend toward a fewer

number of deals, even as the deal amounts

are on average larger.

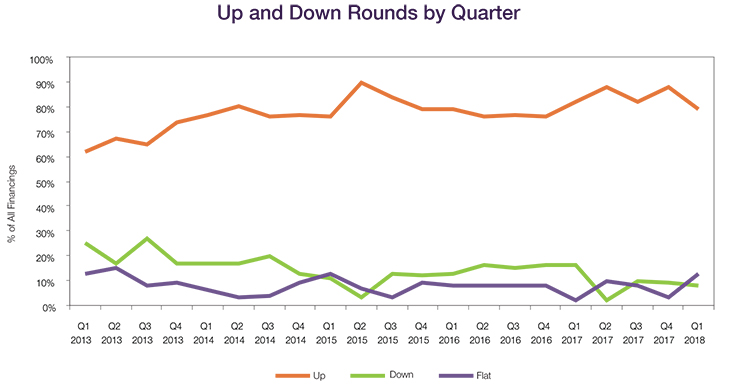

Up and Down Rounds

Up rounds fell as a percentage of all deals

in Q1 2018, constituting 79% of Series

B and later financings versus 88% in Q4

2017. Down rounds represented 8%

of financings in Q1 2018, down slightly

from 9% in Q4 2017. Flat rounds were

somewhat more prevalent in Q1 2018 as

compared to recent quarters, constituting

13% of Q1 2018 financings.

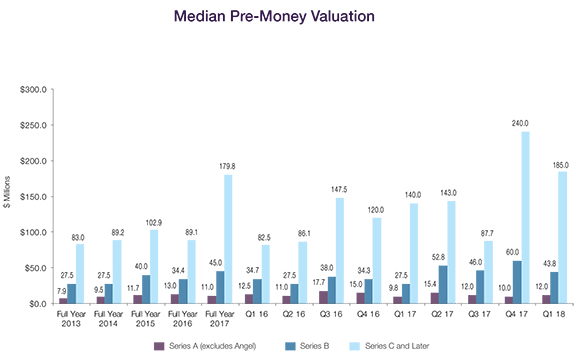

Valuations

Valuations

Early-stage valuations ticked up slightly

in Q1 2018, with the median pre-money

valuation for Seed and Series A financings

increasing to $12.0 million from $10.0

million in Q4 2017. That increase was

not mirrored in the median pre-money

valuations for later rounds. The median

pre-money valuation for Series B rounds

decreased to $43.8 million in Q1 2018

from $60.0 million in Q4 2017. Similarly, the

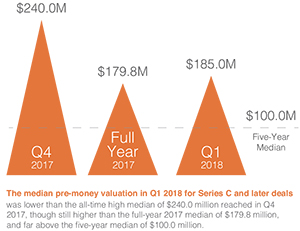

$185.0 million pre-money valuation in Q1

2018 for Series C and later deals was lower

than the all-time high median of $240.0

million reached in Q4 2017, though still

higher than the full-year 2017 median of

$179.8 million, and far above the five-year

median of $100.0 million.

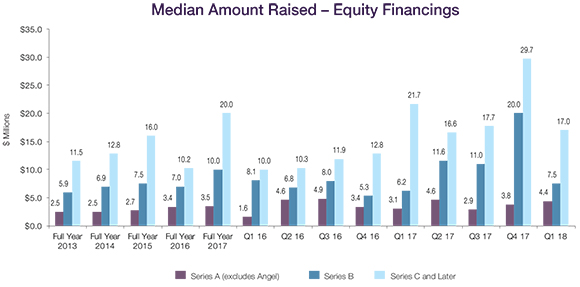

Amounts Raised Amounts Raised

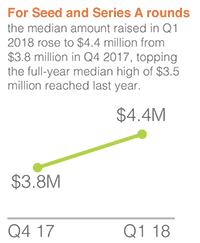

For Seed and Series A rounds, the median

amount raised in Q1 2018 rose to $4.4

million from $3.8 million in Q4 2017,

topping the full-year median high of $3.5

million reached last year. The median

amount raised in Series B financings in Q1

2018 fell to $7.5 million from the all-time

high of $20.0 million reached in Q4 2017.

The median amount raised in Series C

and later financings likewise retreated from

Q4 2017s historic high of $29.7 million to

$17.0 million in Q1 2018, but remained

above the five-year median of $14.6 million.

Deal Terms - Preferred

Senior liquidation preferences in post-Series A rounds were less common in Q1 2018, decreasing from 35% of all such rounds in 2017 to 28% in Q1 2018, the lowest percentage seen in the past five years. Pari passu liquidation preferences increased to 72% of post-Series A rounds in Q1 2018 from 62% in 2017, the highest percentage seen in the past five years.

The percentage of financings having a liquidation preference with participation dipped slightly in Q1 2018, to 14% from 16% of financings in 2017 and 20% in 2016.

Fewer financings provided dividends in Q1 2018 than in prior years, with 73% offering dividends, as compared to 85% of financings in 2017. The use of redemption rights decreased as well, accounting for just 3% of Q1 2018 financings, down from 19% in 2017. The significant drop in the number of deals with redemption rights reflects the continuing leverage that companies have to dictate terms in a strong market. Fewer financings provided dividends in Q1 2018 than in prior years, with 73% offering dividends, as compared to 85% of financings in 2017. The use of redemption rights decreased as well, accounting for just 3% of Q1 2018 financings, down from 19% in 2017. The significant drop in the number of deals with redemption rights reflects the continuing leverage that companies have to dictate terms in a strong market.

Data on deal terms such as liquidation preferences, dividends, and others are set forth in the table below. To see how the terms tracked in the table can be used in the context of a financing, we encourage you to draft a term sheet using our automated Term Sheet Generator, which is available in the Start-Ups and Venture Capital section of the firm's website at www.wsgr.com.

Private Company Financing Deal Terms (WSGR Deals)1

|

2013 |

2014 |

2015 |

2016 |

2017 |

Q1 2018 |

2013 |

2014 |

2015 |

2016 |

2017 |

Q1 2018 |

2013 |

2014 |

2015 |

2016 |

2017 |

Q1 2018 |

All Rounds2 |

All Rounds2 |

All Rounds2 |

All Rounds2 |

All Rounds2 |

All Rounds2 |

Up Rounds3 |

Up Rounds3 |

Up Rounds3 |

Up Rounds3 |

Up Rounds3 |

Up Rounds3 |

Down Rounds3 |

Down Rounds3 |

Down Rounds3 |

Down Rounds3 |

Down Rounds3 |

Down Rounds4 |

Liquidation Preferences - Series B and Later |

Senior |

41% |

40% |

33% |

38% |

35% |

28% |

38% |

32% |

31% |

36% |

31% |

32% |

47% |

68% |

35% |

41% |

63% |

N/A |

Pari Passu with Other Preferred |

55% |

56% |

62% |

57% |

62% |

72% |

60% |

64% |

66% |

62% |

66% |

68% |

37% |

21% |

53% |

45% |

38% |

N/A |

Junior |

0% |

0% |

1% |

1% |

0% |

0% |

0% |

0% |

1% |

0% |

0% |

0% |

0% |

0% |

0% |

5% |

0% |

N/A |

Complex |

3% |

2% |

3% |

4% |

3% |

0% |

2% |

2% |

1% |

2% |

4% |

0% |

11% |

5% |

12% |

9% |

0% |

N/A |

Not Applicable |

1% |

3% |

1% |

0% |

0% |

3% |

0% |

2% |

1% |

0% |

0% |

0% |

5% |

5% |

0% |

0% |

0% |

N/A |

Participating vs. Non-participating |

Participating - Cap |

18% |

12% |

8% |

9% |

6% |

3% |

20% |

14% |

11% |

10% |

7% |

5% |

23% |

13% |

12% |

22% |

31% |

N/A |

Participating - No Cap |

12% |

14% |

11% |

11% |

10% |

11% |

10% |

11% |

12% |

13% |

11% |

11% |

30% |

32% |

35% |

4% |

19% |

N/A |

Non-participating |

70% |

74% |

81% |

81% |

84% |

85% |

69% |

76% |

77% |

77% |

82% |

84% |

48% |

55% |

53% |

74% |

50% |

N/A |

Dividends |

Yes, Cumulative |

12% |

13% |

3% |

6% |

7% |

10% |

12% |

11% |

3% |

7% |

9% |

11% |

13% |

24% |

24% |

22% |

13% |

N/A |

Yes, Non-cumulative |

74% |

72% |

82% |

73% |

78% |

63% |

79% |

74% |

86% |

78% |

78% |

74% |

79% |

71% |

76% |

70% |

81% |

N/A |

None |

14% |

15% |

15% |

21% |

16% |

27% |

9% |

15% |

11% |

15% |

13% |

16% |

8% |

5% |

0% |

9% |

6% |

N/A |

Anti-dilution Provisions |

Weighted Average - Broad |

90% |

85% |

80% |

92% |

94% |

88% |

94% |

90% |

86% |

92% |

96% |

95% |

95% |

92% |

75% |

91% |

100% |

N/A |

Weighted Average - Narrow |

3% |

9% |

13% |

1% |

2% |

3% |

3% |

6% |

12% |

1% |

1% |

5% |

0% |

5% |

19% |

0% |

0% |

N/A |

Ratchet |

1% |

1% |

1% |

1% |

0% |

0% |

0% |

1% |

1% |

2% |

0% |

0% |

3% |

0% |

0% |

0% |

0% |

N/A |

Other (Including Blend) |

1% |

1% |

1% |

3% |

1% |

2% |

1% |

1% |

1% |

3% |

1% |

0% |

0% |

0% |

0% |

9% |

0% |

N/A |

None |

5% |

4% |

5% |

3% |

3% |

8% |

2% |

2% |

1% |

2% |

1% |

0% |

3% |

3% |

6% |

0% |

0% |

N/A |

Pay to Play - Series B and Later |

Applicable to This Financing |

5% |

4% |

5% |

5% |

2% |

4% |

1% |

1% |

3% |

3% |

2% |

0% |

15% |

16% |

18% |

9% |

6% |

N/A |

Applicable to Future Financings |

1% |

0% |

1% |

1% |

0% |

0% |

1% |

0% |

0% |

1% |

0% |

0% |

0% |

0% |

12% |

0% |

0% |

N/A |

None |

95% |

96% |

94% |

94% |

98% |

96% |

98% |

99% |

97% |

96% |

98% |

100% |

85% |

84% |

71% |

91% |

94% |

N/A |

Redemption |

Investor Option |

19% |

17% |

13% |

11% |

12% |

3% |

20% |

22% |

19% |

20% |

19% |

5% |

33% |

24% |

12% |

9% |

20% |

N/A |

Mandatory |

1% |

3% |

2% |

2% |

7% |

0% |

2% |

3% |

3% |

3% |

9% |

0% |

0% |

3% |

0% |

0% |

0% |

N/A |

None |

80% |

80% |

85% |

87% |

81% |

97% |

78% |

75% |

78% |

77% |

72% |

95% |

67% |

74% |

88% |

91% |

80% |

N/A |

| 1 We based this analysis on deals having an initial closing in the period to ensure that the data clearly reflects current trends. Please note the numbers do not always add up to 100% due to rounding. |

| 2 Includes flat rounds and, unless otherwise indicated, Series A rounds. |

| 3 Note that the All Rounds metrics include flat rounds and, in certain cases Series A financings as well. Consequently, metrics in the All Rounds column may be outside the ranges bounded by the Up Rounds and Down Rounds columns, which will not include such transactions. |

| 4 Due to the small number of down rounds in Q1 2018, we did not calculate the deal term percentages in this category. |

| |

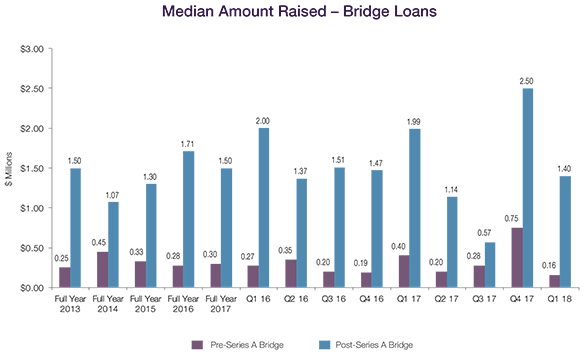

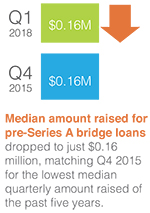

Bridge Loans

The median amounts raised for bridge loans fell sharply for both pre- and post-Series A deals in Q1 2018. The median amount raised for pre-Series A bridge loans dropped to just $0.16 million, matching Q4 2015 for the lowest median quarterly amount raised of the past five years. Post-Series A bridges also raised fewer dollars, with the median amount raised declining to $1.40 million, far lower than the $2.50 million median of Q4 2017, though still close to the full-year 2017 median of $1.50 million.

Deal Terms – Bridge Loans Deal Terms – Bridge Loans

Bridge loan interest rates rose in Q1 2018, with 50% of both pre- and post-Series A bridge loans having interest rates of 8% or greater a significant increase from the corresponding 25% and 44% figures in 2017. Maturity periods increased significantly as well. Eighty-three percent of both pre-Series A and post-Series A bridge loans had maturity periods of more than 12 months in Q1 2018, up from 69% of pre-Series A loans and 41% of post-Series A loans in 2017. All Q1 bridge loans were convertible; 75% of pre-Series A loans and all post-Series A loans received a discount rate of 20% or more on conversion.

Bridge Loans Deal Terms (WSGR Deals)1

Bridge Loans |

2013

Pre-Series

A |

2014

Pre-Series

A |

2015

Pre-Series

A |

2016

Pre-Series

A |

2017

Pre-Series

A |

Q1 2018

Pre-Series

A |

2013

Post-Series

A |

2014

Post-Series

A |

2015

Post-Series

A |

2016

Post-Series

A |

2017

Post-Series

A |

Q1 2018

Post-Series

A |

Interest rate less than 8% |

70% |

72% |

74% |

76% |

75% |

50% |

46% |

43% |

54% |

52% |

56% |

50% |

Interest rate at 8% |

29% |

22% |

19% |

19% |

17% |

50% |

34% |

42% |

33% |

30% |

27% |

17% |

Interest rate greater than 8% |

1% |

6% |

7% |

5% |

8% |

0% |

20% |

15% |

13% |

17% |

17% |

33% |

Maturity less than 12 months |

3% |

12% |

17% |

17% |

22% |

0% |

29% |

24% |

34% |

29% |

41% |

17% |

Maturity at 12 months |

19% |

16% |

9% |

5% |

8% |

17% |

38% |

39% |

8% |

23% |

19% |

0% |

Maturity more than 12 months |

78% |

71% |

74% |

78% |

69% |

83% |

33% |

37% |

58% |

49% |

41% |

83% |

Debt is subordinated to other debt |

25% |

22% |

15% |

20% |

28% |

17% |

56% |

48% |

38% |

45% |

33% |

50% |

Loan includes warrants2 |

4% |

5% |

3% |

8% |

0% |

17% |

34% |

19% |

25% |

17% |

16% |

17% |

Warrant coverage less than 25% |

0% |

20% |

100% |

80% |

N/A |

0% |

50% |

69% |

47% |

23% |

43% |

0% |

Warrant coverage at 25% |

0% |

0% |

0% |

0% |

N/A |

0% |

12% |

0% |

7% |

15% |

14% |

0% |

Warrant coverage greater than 25% |

100% |

80% |

0% |

20% |

N/A |

100% |

38% |

31% |

47% |

62% |

43% |

100% |

Principal is convertible into equity3 |

100% |

98% |

93% |

97% |

97% |

100% |

94% |

94% |

86% |

92% |

92% |

100% |

Conversion rate subject to price cap4 |

68% |

67% |

64% |

79% |

74% |

67% |

14% |

23% |

26% |

29% |

34% |

17% |

Conversion to equity at discounted price5 |

91% |

81% |

78% |

82% |

89% |

67% |

59% |

73% |

71% |

74% |

76% |

83% |

Discount on conversion less than 20% |

17% |

10% |

11% |

12% |

16% |

25% |

16% |

25% |

25% |

25% |

20% |

0% |

Discount on conversion at 20% |

60% |

72% |

73% |

76% |

74% |

50% |

46% |

44% |

47% |

49% |

50% |

80% |

Discount on conversion greater than 20% |

22% |

17% |

16% |

12% |

10% |

25% |

38% |

32% |

27% |

26% |

30% |

20% |

Conversion to equity at same price as other investors |

9% |

16% |

18% |

13% |

3% |

17% |

35% |

24% |

25% |

19% |

24% |

17% |

1 We based this analysis on deals having an initial closing in the period to ensure that the data clearly reflects current trends. Please note the numbers do not always add up to 100% due to rounding.

2 Of the 2013 post-Series A bridges with warrants, 24% also had a discount on conversion into equity. Of the 2014 post-Series A bridges with warrants, 38% also had a discount on conversion into equity. Of the 2015 post-Series A bridges with warrants, 58% also had a discount on conversion into equity. Of the 2016 post-Series A bridges with warrants, 33% also had a discount on conversion into equity. Of the 2017 post-Series A bridges with warrants, 60% also had a discount on conversion into equity. Due to the small number of post-Series A bridges with warrants in Q1 2018, we did not do the comparision

3 Of the 2016 pre-Series A convertible bridges, 93% had automatic conversion and 7% had voluntary conversion. Of the 2017 pre-Series A convertible bridges, 94% had automatic conversion and 6% had voluntary conversion. Of the Q1 2018 pre-Series A convertible bridges, 100% had automatic conversion and 0% had voluntary conversion. Of the 2016 post-Series A convertible bridges, 97% had automatic conversion and 3% had voluntary conversion. Of the 2017 post-Series A convertible bridges, 93% had automatic conversion and 7% had voluntary conversion. Of the Q1 2018 post-Series A convertible bridges, 83% had automatic conversion and 17% had voluntary conversion. The 2016 median dollar threshold for a qualified financing in pre- and post-Series A bridges was $1M and $5M, respectively. The 2017 median dollar threshold for a qualified financing in pre- and post-Series A bridges was $2M and $10M, respectively. The Q1 2018 median dollar threshold for a qualified financing in pre- and post-Series A bridges was $4M and $5M, respectively.

4 The 2016 median price cap in pre- and post-Series A bridges was $6M and $25M, respectively. The 2017 median price cap in pre- and post-Series A bridges was $10M and $25M, respectively.

5 Of the 2013 post-Series A bridges that had a discount on conversion into equity, 15% also had warrants. Of the 2014 post-Series A bridges that had a discount on conversion into equity, 10% also had warrants. Of the 2015 post-Series A bridges that had a discount on conversion into equity, 21% also had warrants. Of the 2016 post-Series A bridges that had a discount on conversion into equity, 8% also had warrants. Of the 2017 post-Series A bridges that had a discount on conversion into equity, 13% also had warrants. Due to the small number of post-Series A bridges with warrants in Q1 2018, we did not do the conversion.

|

[back to top]

The View from Across the Pond: A Data-Driven Comparison of European and U.S. Venture Capital Transactions

By Daniel Glazer (Partner, New York)

|

1. U.S. and European trends are broadly similar, but the changes are more pronounced in the U.S.

Over the past several years, the U.S. and European

venture capital markets have both seen increases

in deal sizes and a drop in the number of deals.

However, the changes in the European markets

have been much more subtle and the venture

capital market is still much smaller than in the U.S.

Venture capital funds in the U.S. have been able

to raise significantly larger amounts than European

funds—U.S. venture capital funds are, on average, three times larger than European venture capital funds. Furthermore, U.S. funds raise, on average, 60-70% of the global venture capital raised.

Meanwhile, later stage private equity funds and

crossover funds that traditionally invested only

in public companies have dramatically increased

their investments in late-stage private companies.

With more funds available than ever before in

both Europe and the U.S. for investment in private

technology companies, we expect these trends

to continue in both markets at least until there is a

significant correction in the broader capital markets.

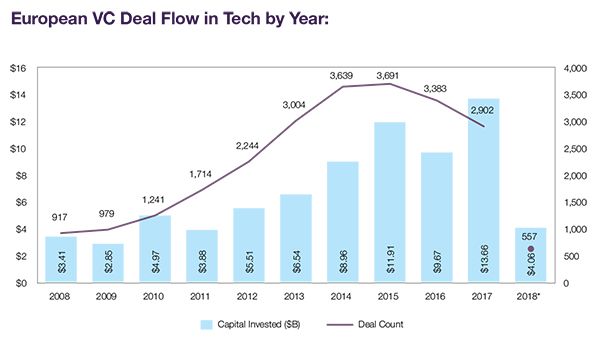

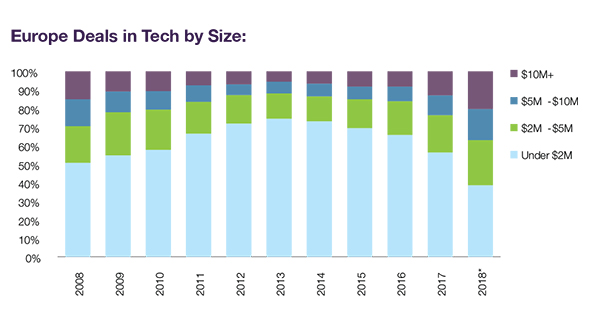

2. In Europe, there are fewer deals but more money overall than in prior years.

In 2017 there were 2,902 venture deals reported in

Europe, which was significantly down from a total

of 3,383 deals in 2016 and 3,691 deals in 2015.

However, the total amount invested increased significantly,

with $13.66 billion raised in 2017, up from

$9.67 billion in 2016 and $11.91 billion in 2015.

This trend of fewer, larger deals has become even

more pronounced in recent years, signaling a maturation

of the European venture finance ecosystem.

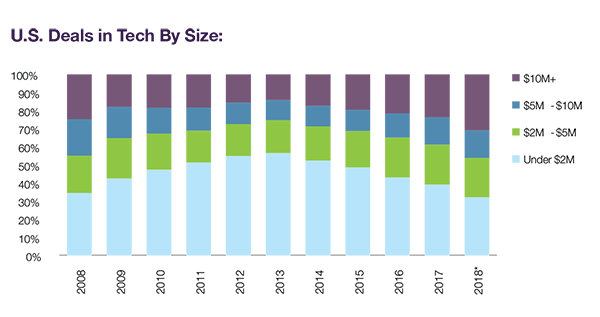

3. A larger percentage of European deals are smaller sized than in the U.S.

Fewer than 40% of U.S. venture capital deals raised under $2.0 million in 2017. In Europe, however, 56% of deals raised under

$2.0 million. Across both markets, the

percentage of smaller deals has been

decreasing, but the majority of European

venture capital deals remain relatively

early-stage.

4. There has been a stark increase in the number of large deals in Europe.

Across both markets, the percentage

of deals valued more than $10.0 million

has continued to increase over the last

several years, particularly in Europe.

These large deals comprised only 8%

of total deals in 2015 and 2016, but

the percentage jumped to almost 13%

of total deals in 2017 and 20% in the

first quarter of 2018. There also has

been an increase in the number of deals

between $5.0 million to $10.0 million,

which made up 17% of the deals in the

first quarter of 2018 and 11% of deals in

2017, up from roughly 7% in 2015 and

2016. The U.S. market also has seen

a steady increase in the percentage of

large deals, but the increase has not

been as dramatic over the last year.

5. Average deal size and pre-money valuation are materially lower in Europe versus the U.S. This gap is even larger when compared solely with the West Coast of the U.S.

European deal sizes and pre-money

valuations are much lower than in the

U.S. In 2017, despite an increase in European

deal size, the average U.S. West

Coast deal was more than twice as large

as the average European deal at every

stage of investment. In 2017, median

deal sizes for early-stage transactions

were nearly three times as large in the

U.S. as compared to Europe and late-stage

deals in the U.S. were 1.4 times

the size of late-stage deals in Europe.

These differences also are apparent in

median pre-money valuations. In 2017,

U.S. pre-money valuations were 2.6

times higher for seed-stage deals, 4.2

times higher for early-stage deals, and

5.8 times higher for late-stage deals.

These multiples are even higher when

compared only against West Coast

deals, with multiples of 2.8 times, 4.9

times and 7.4 times, respectively.

|

[back to top]

Methodology

The Up/Down/Flat analysis is based on WSGR deals having an initial closing in the period reported to ensure that the data clearly reflects current trends. The median pre-money valuation is calculated based on the pre-money valuation given at the time of the initial closing of the round. If the issuer has a closing in a subsequent quarter, the original pre-money valuation is used in the calculation of the median for that quarter as well. A substantial percentage of deals have multiple closings that span fiscal quarters. The median amount raised is calculated based on the aggregate amount raised in the reported quarter. For purposes of this report, Series Seed transactions are included with Series A transactions.

This report is based on detailed deal data provided by the firms corporate and securities attorneys and analyzed by the firm's Knowledge Management department.

To learn more about WSGR's full suite of services for entrepreneurs and early-stage companies, please visit the Start-Ups and Venture Capital section of wsgr.com.

For more information about this report or if you wish to be included on the email subscription list, please email us at EntrepreneursReport@wsgr.com. There is no subscription fee. |

This communication is provided as a service to our clients and friends and is for informational purposes only. It is not intended to create an attorney-client relationship or constitute an advertisement, a solicitation, or professional advice as to any particular situation.

© 2018 Wilson Sonsini Goodrich & Rosati, Professional

Corporation

Click here for a printable version of The Entrepreneurs Report |