|

From the WSGR Database: Financing Trends for 2016

For purposes of the statistics and

charts in this report, our database

includes venture financing

transactions in which Wilson

Sonsini Goodrich & Rosati

represented either the company or

one or more of the investors.

|

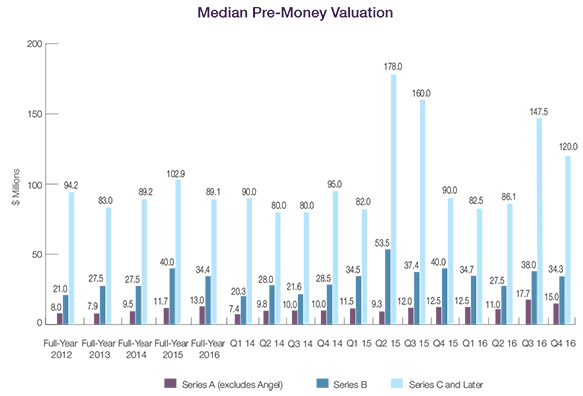

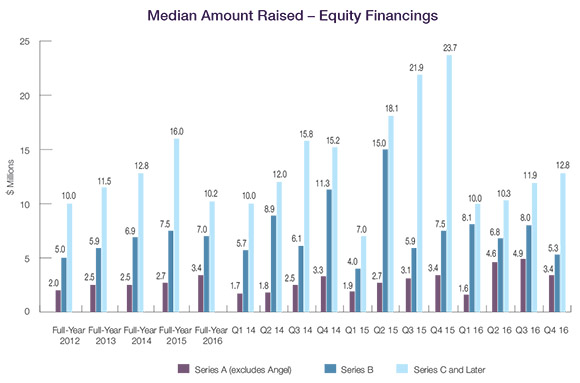

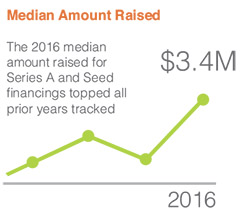

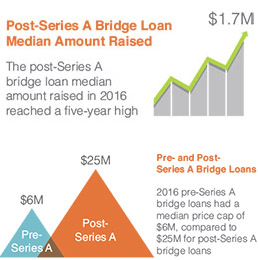

Venture financing data shows that 2016 was an exceptionally strong year for early-stage valuations and amounts raised. Median pre-money valuations for 2016 Series A and Seed financings exceeded those of each of the past five years, while the median amount raised for Series A and Seed financings—$3.4 million—topped all prior years tracked. Similarly, the median amount raised in 2016 post-Series A bridge loans—$1.7 million—set a five-year high. On the other hand, Series C and later rounds saw pre-money valuations and amounts raised decline from the past two years, though they stayed in line with five-year medians.

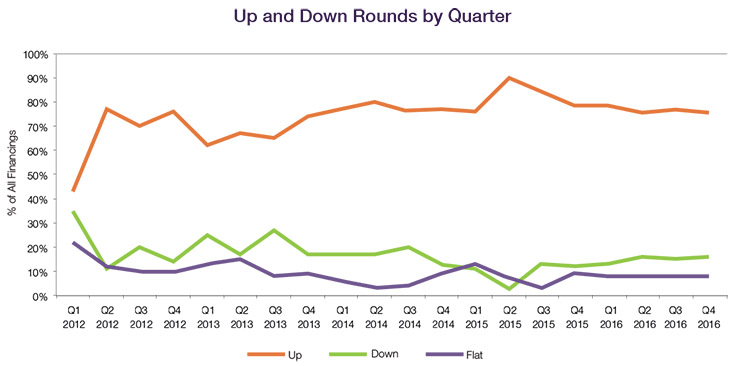

Up and Down Rounds

Up rounds were slightly less prevalent, and down rounds were slightly more prevalent, in Q4 2016 as compared to earlier in 2016 and to 2015. Up rounds represented 76% of Q4 2016 financings, while down rounds represented 16% (as compared to 79% and 13%, respectively, in Q1 2016). For full-year 2016, up rounds represented 77% of all financings, a decrease from full-year 2015s historically high 83%. Conversely, down rounds increased from 9% of 2015 financings to 15% of 2016 financings.

|

Valuations

Early-stage valuations were historically high in 2016. The full-year 2016 median pre-money valuation for Series A and Seed financings was $13.0 million, higher than those of the past five years and well above the five-year median of $8.5 million. The Q4 2016 median pre-money valuation of $15.0 million for Series A and Seed financings was the second-highest quarterly figure in the past five years, lower only than the prior quarters $17.7 million figure. Similarly, while the median pre-money valuation for Series B rounds dropped slightly from $38.0 million in Q3 2016 to $34.3 million in Q4 2016, the full-year 2016 median of $34.4 million outpaced the five-year median of $30.0 million. On the other hand, the median pre-money valuation for Series C and later deals dropped from $147.5 million in Q3 2016 to $120.0 million in Q4 2016, which brought the full-year 2016 median Series C and later valuation to $89.1 million—below the five-year median of $95.0 million.

|

Amounts Raised Amounts Raised

While Q4 2016 median amounts raised for Seed, Series A, and Series B rounds were generally lower than in Q3, full-year 2016 amounts raised were higher than any others in the past five years. Specifically, the $3.4 million median amount raised in 2016 Series A and Seed transactions exceeded median amounts raised in all prior years tracked, even though Q4 2016s $3.4 million figure was markedly down from Q3 2016s all-time high of $4.9 million. The median amount raised in Q4 2016 Series B financings likewise dipped to $5.3 million from the Q3 2016 high of $8.0 million, although the full-year 2016 Series B median amount raised was $7.0 million, exceeding the five-year median of $5.8 million. The median amount raised in Series C and later transactions rose to $12.8 million in Q4 2016, representing the highest value of the years four quarters. The full-year 2016 median for Series C and later transactions fell to $10.2 million from the highs reached in 2015 and 2014, just $1.8 million below the five-year median of $12.0 million. The somewhat lower median amounts raised for Series C and later transactions in 2016 may reflect strategic decisions by private companies to avoid raising relatively large amounts of money at late-stage valuations that are meaningfully below the peaks reached in late 2015.

Deal Terms - Preferred Deal Terms - Preferred

The use of senior liquidation preferences increased modestly in Series B and later rounds, from 33% of all such rounds in 2015 to 38% in 2016. The increase was seen in both up and down rounds, with senior liquidation preferences in up rounds growing from 31% in 2015 to 36% in 2016, and use in down rounds increasing from 35% in 2015 to 41% in 2016. Meanwhile, pari passu liquidation preferences in down rounds decreased from 53% in 2015 to 45% in 2016.

The percentage of financings having a liquidation preference with participation remained steady for all financings at 20%. However, the proportion of down rounds with participating liquidation preferences dropped from 47% in 2015 to 26% in 2016.

Investors received broad-based weighted average anti-dilution protection in 92% of all deals in 2016, a notable increase from the 80% figure in 2015. Conversely, the use of narrow-based weighted average anti-dilution protection fell from 13% of all deals in 2015 to just 1% in 2016.

Data on deal terms such as liquidation preferences, dividends, and others are set forth in the table below. To see how the terms tracked in the table can be used in the context of a financing, we encourage you to draft a term sheet using our automated Term Sheet Generator, which is available in the Start-Ups and Venture Capital section of the firms website at www.wsgr.com.

Private Company Financing Deal Terms (WSGR Deals)1

|

2013 |

2014 |

2015 |

2016 |

2013 |

2014 |

2015 |

2016 |

2013 |

2014 |

2015 |

2016 |

All Rounds2 |

All Rounds2 |

All Rounds2 |

All Rounds2 |

Up Rounds3 |

Up Rounds3 |

Up Rounds3 |

Up Rounds3 |

Down Rounds3 |

Down Rounds3 |

Down Rounds3 |

Down Rounds3 |

Liquidation Preferences - Series B and Later |

Senior |

41% |

40% |

33% |

38% |

38% |

32% |

31% |

36% |

47% |

68% |

35% |

41% |

Pari Passu with Other Preferred |

55% |

56% |

62% |

57% |

60% |

64% |

66% |

62% |

37% |

21% |

53% |

45% |

Junior |

0% |

0% |

1% |

1% |

0% |

0% |

1% |

0% |

0% |

0% |

0% |

5% |

Complex |

3% |

2% |

3% |

4% |

2% |

2% |

1% |

2% |

11% |

5% |

12% |

9% |

Not Applicable |

1% |

3% |

1% |

0% |

0% |

2% |

1% |

0% |

5% |

5% |

0% |

0% |

Participating vs. Non-participating |

Participating - Cap |

18% |

12% |

8% |

9% |

20% |

14% |

11% |

10% |

23% |

13% |

12% |

22% |

Participating - No Cap |

12% |

14% |

11% |

11% |

10% |

11% |

12% |

13% |

30% |

32% |

35% |

4% |

Non-participating |

70% |

74% |

81% |

81% |

69% |

76% |

77% |

77% |

48% |

55% |

53% |

74% |

Dividends |

Yes, Cumulative |

12% |

13% |

3% |

6% |

12% |

11% |

3% |

7% |

13% |

24% |

24% |

22% |

Yes, Non-cumulative |

74% |

72% |

82% |

73% |

79% |

74% |

86% |

78% |

79% |

71% |

76% |

70% |

None |

14% |

15% |

15% |

21% |

9% |

15% |

11% |

15% |

8% |

5% |

0% |

9% |

Anti-dilution Provisions |

Weighted Average - Broad |

90% |

85% |

80% |

92% |

94% |

90% |

86% |

92% |

95% |

92% |

75% |

91% |

Weighted Average - Narrow |

3% |

9% |

13% |

1% |

3% |

6% |

12% |

1% |

0% |

5% |

19% |

0% |

Ratchet |

1% |

1% |

1% |

1% |

0% |

1% |

1% |

2% |

3% |

0% |

0% |

0% |

Other (Including Blend) |

1% |

1% |

1% |

3% |

1% |

1% |

1% |

3% |

0% |

0% |

0% |

9% |

None |

5% |

4% |

5% |

3% |

2% |

2% |

1% |

2% |

3% |

3% |

6% |

0% |

Pay to Play - Series B and Later |

Applicable to This Financing |

5% |

4% |

5% |

5% |

1% |

1% |

3% |

3% |

15% |

16% |

18% |

9% |

Applicable to Future Financings |

1% |

0% |

1% |

1% |

1% |

0% |

0% |

1% |

0% |

0% |

12% |

0% |

None |

95% |

96% |

94% |

94% |

98% |

99% |

97% |

96% |

85% |

84% |

71% |

91% |

Redemption |

Investor Option |

19% |

17% |

13% |

11% |

20% |

22% |

19% |

20% |

33% |

24% |

12% |

9% |

Mandatory |

1% |

3% |

2% |

2% |

2% |

3% |

3% |

3% |

0% |

3% |

0% |

0% |

None |

80% |

80% |

85% |

87% |

78% |

75% |

78% |

77% |

67% |

74% |

88% |

91% |

| 1 We based this analysis on deals having an initial closing in the period to ensure that the data clearly reflects current trends. Please note that the numbers do not always add up to 100% due to rounding. |

| 2 Includes flat rounds and, unless otherwise indicated, Series A rounds. |

| 3 Note that the All Rounds metrics include flat rounds and, in certain cases, Series A financings as well. Consequently, metrics in the All Rounds column may be outside the ranges bounded by the Up Rounds and Down Rounds columns, which will not include such transactions. |

| |

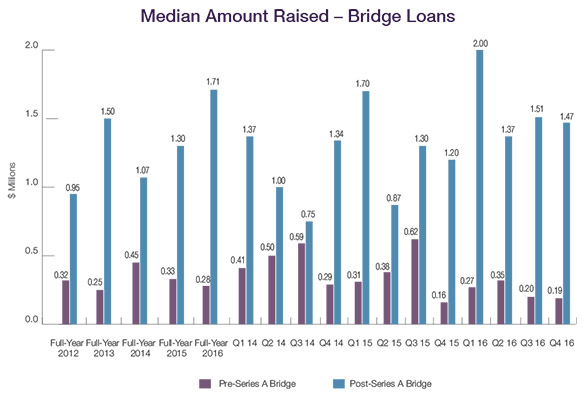

Bridge Loans

The median amount raised for pre-Series A bridge loans remained flat at $0.19 million in Q4 2016 compared to Q3 2016. The full-year median amount raised was $0.28 million, slightly lower than in 2015 and 2014. The median amount raised for Q4 2016 post-Series A bridge loans also remained flat compared to Q3 2016, but the high median amount raised in Q1 2016 brought the years cumulative median to $1.7 million—a five-year high.

Deal Terms – Bridge Loans

Bridge loan interest rates for pre-Series A deals continued a slight downward trend in 2016. Among pre-Series A bridge loans, 76% had interest rates less than 8%, up from 74%, 72%, and 70% in 2015, 2014, and 2013, respectively. Further, only 5% of 2016 pre-Series A bridge loans had interest rates greater than 8% in 2016, slightly fewer than in 2015 and 2014.

Interest rates are typically higher for post-Series A bridge loans, though they havent shown the same gradual increase as earlier-stage deals. For post-Series A bridge loans, rates above 8% climbed slightly from 13% of deals in 2015 to 17% in 2016, while 52% of such loans bore rates of less than 8%, on par with what was seen in 2015.

Price caps and discounts upon conversion became more popular in 2016 for pre-Series A bridge loans. Price caps increased from 64% of deals in 2015 to 79% of deals in 2016, and discounts on conversion of pre-Series A loans also rose slightly, from 78% of deals in 2015 to 82% of deals in 2016. On the other hand, the size of discounts dropped, with the percentage featuring a discount of over 20% declining from 16% of such loans in 2015 to 12% in 2016. Price caps and discounts upon conversion became more popular in 2016 for pre-Series A bridge loans. Price caps increased from 64% of deals in 2015 to 79% of deals in 2016, and discounts on conversion of pre-Series A loans also rose slightly, from 78% of deals in 2015 to 82% of deals in 2016. On the other hand, the size of discounts dropped, with the percentage featuring a discount of over 20% declining from 16% of such loans in 2015 to 12% in 2016.

We recently started tracking whether convertible note conversion was automatic or voluntary, the dollar thresholds for conversion, and the price cap amounts. Of the 2016 pre-Series A convertible bridges, 90% had automatic conversion and 10% had voluntary conversion. The breakdown was similar for 2016 post-Series A deals, with 92% having automatic conversion and 8% having voluntary conversion.

The median dollar threshold for a qualified financing in 2016 pre-Series A loans was $1.0 million, and 2016 pre-Series A bridges had a median price cap of $6.0 million. Not surprisingly, the corresponding amounts for post-Series A deals were notably higher, at $4.0 million and $25.0 million, respectively. We will continue to track these terms and report period-over-period changes.

Bridge Loans Deal Terms (WSGR Deals)

Bridge Loans1 |

2013

Pre-Series

A |

2014

Pre-Series

A |

2015

Pre-Series

A |

2016

Pre-Series

A |

2013

Post-Series

A |

2014

Post-Series

A |

2015

Post-Series

A |

2016

Post-Series

A |

Interest rate less than 8% |

70% |

72% |

74% |

76% |

46% |

43% |

54% |

52% |

Interest rate at 8% |

29% |

22% |

19% |

19% |

34% |

42% |

33% |

30% |

Interest rate greater than 8% |

1% |

6% |

7% |

5% |

20% |

15% |

13% |

17% |

Maturity less than 12 months |

3% |

12% |

17% |

17% |

29% |

24% |

34% |

29% |

Maturity 12 months |

19% |

16% |

9% |

5% |

38% |

39% |

8% |

23% |

Maturity more than 12 months |

78% |

71% |

74% |

78% |

33% |

37% |

58% |

49% |

Debt is subordinated to other debt |

25% |

22% |

15% |

20% |

56% |

48% |

38% |

45% |

Loan includes warrants2 |

4% |

5% |

3% |

8% |

34% |

19% |

25% |

17% |

Warrant coverage less than 25% |

0% |

20% |

100% |

80% |

50% |

69% |

47% |

23% |

Warrant coverage at 25% |

0% |

0% |

0% |

0% |

12% |

0% |

7% |

15% |

Warrant coverage greater than 25% |

100% |

80% |

0% |

20% |

38% |

31% |

47% |

62% |

Principal is convertible into equity3 |

100% |

98% |

93% |

97% |

94% |

94% |

86% |

92% |

Conversion rate subject to price cap4 |

68% |

67% |

64% |

79% |

14% |

23% |

26% |

29% |

Conversion to equity at discounted price5 |

91% |

81% |

78% |

82% |

59% |

73% |

71% |

74% |

Discount on conversion less than 20% |

17% |

10% |

11% |

12% |

16% |

25% |

25% |

25% |

Discount on conversion at 20% |

60% |

72% |

73% |

76% |

46% |

44% |

47% |

49% |

Discount on conversion greater than 20% |

22% |

17% |

16% |

12% |

38% |

32% |

27% |

26% |

Conversion to equity at same price as other investors |

9% |

16% |

18% |

13% |

35% |

24% |

25% |

19% |

1 We based this analysis on deals having an initial closing in the period to ensure that the data clearly reflects current trends. Please note that the numbers do not always add up to 100% due to rounding.

2 Of the 2013 post-Series A bridges with warrants, 24% also had a discount on conversion into equity. Of the 2014 post-Series A bridges with warrants, 38% also had a discount on conversion into equity. Of the 2015 post-Series A bridges with warrants, 58% also had a discount on conversion into equity. Of the 2016 post-Series A bridges with warrants, 33% also had a discount on conversion into equity.

3 Of the 2016 pre-Series A convertible bridges, 90% had automatic conversion and 10% had voluntary conversion. Of the 2016 post-Series A convertible bridges, 92% had automatic conversion and 8% had voluntary conversion. The median dollar threshold for a qualified financing in pre- and post-Series A bridges was $1M and $4M, respectively.

4 2016 pre-Series A bridges had a median price cap of $6M. 2016 post-Series A bridges had a median price cap of $25M.

5 Of the 2013 post-Series A bridges that had a discount on conversion into equity, 15% also had warrants. Of the 2014 post-Series A bridges that had a discount on conversion into equity, 10% also had warrants. Of the 2015 post-Series A bridges that had a discount on conversion into equity, 21% also had warrants. Of the 2016 post-Series A bridges that had a discount on conversion into equity, 8% also had warrants.

|

[back to top]

Methodology for WSGR's Entrepreneurs Report

The Up/Down/Flat analysis is based on WSGR deals having an initial closing in the period reported to ensure that the data clearly reflects current trends. The median pre-money valuation is calculated based on the pre-money valuation given at the time of the initial closing of the round. If the issuer has a closing in a subsequent quarter, the original pre-money valuation is used in the calculation of the median for that quarter as well. A substantial percentage of deals have multiple closings that span fiscal quarters. The median amount raised is calculated based on the aggregate amount raised in the reported quarter. For purposes of this report, Series Seed transactions are included with Series A transactions.

Dow Jones VentureSource Ranks WSGR No. 1 for 2016 Venture Financing Deals

Dow Jones VentureSource's legal rankings for 2016 issuer-side venture financing deals ranked Wilson Sonsini Goodrich & Rosati ahead of all other firms by the total number of rounds of equity financing raised on behalf of clients. WSGR is credited as legal advisor in 207 rounds of financing, while its nearest competitor advised on 136 rounds of financing.

According to VentureSource, WSGR ranked first for 2016 issuer-side U.S. deals in the following industries: cleantech, communications and networking, consumer services, electronics and hardware (tie), energy and utilities, healthcare, industrial goods and materials, information technology, medical devices and equipment, semiconductors (tie), and software. The firm ranked second in biopharmaceuticals and business and financial services, and third (tie) in consumer goods.

|

WSGR Partners with Tech City UK to Provide Resources for Entrepreneurs

Wilson Sonsini Goodrich & Rosati has partnered with Tech City UK, a UK-government-backed organization tasked with accelerating the growth of UK digital businesses, to publish guidance for entrepreneurs on launching, scaling, and raising capital in the United States. This guidance, which will be provided on a regular basis starting in February 2017, will serve as a resource on U.S. expansion and fundraising for the UK technology community. Wilson Sonsini Goodrich & Rosati has partnered with Tech City UK, a UK-government-backed organization tasked with accelerating the growth of UK digital businesses, to publish guidance for entrepreneurs on launching, scaling, and raising capital in the United States. This guidance, which will be provided on a regular basis starting in February 2017, will serve as a resource on U.S. expansion and fundraising for the UK technology community.

For more information, please visit the Tech City UK blog at http://www.techcityuk.com/?post_type=post.

|

To learn more about WSGR's full suite of services for entrepreneurs and early-stage companies, please visit the Start-Ups and Venture Capital section of wsgr.com.

For more information about this report or if you wish to be included on the email subscription list, please email us at EntrepreneursReport@wsgr.com. There is no subscription fee. |

This communication is provided as a service to our clients and friends and is for informational purposes only. It is not intended to create an attorney-client relationship or constitute an advertisement, a solicitation, or professional advice as to any particular situation.

© 2017 Wilson Sonsini Goodrich & Rosati, Professional

Corporation

Click here for a printable version of The Entrepreneurs Report |