From the WSGR Database: Financing Trends for Q1-Q3 2013

For purposes of the statistics and

charts in this report, our database

includes venture financing

transactions in which Wilson

Sonsini Goodrich & Rosati

represented either the company or

one or more of the investors.

|

As widely reported, the aggregate dollar volume of venture financings held fairly steady from Q2 2013 to Q3 2013 (see, e.g., Venture Capital Valuation and Trends from PitchBook, Q4 2013). An analysis of transactions in which Wilson Sonsini Goodrich & Rosati represented either the company or investors suggests that the market remains positive, with up rounds remaining at roughly two-thirds of all venture deals in both Q2 and Q3. Median pre-money valuations and amounts raised both generally rose in Q3 as compared with Q2. Specifically, pre-money valuations increased for Series A1 and Series C deals that had closings in Q3, whereas valuations for Series B rounds continued the decline that began in Q1 2013. Median amounts raised in WSGR deals increased across the board, except for post-Series A bridge loans.

Deal terms remained broadly similar for the period Q1-Q3 2013 as compared with 2012, with the notable exception of a continued decline in the usage of participation rights in both up and down rounds.

1Seed transactions are included with Series A deals.

Up and Down Rounds

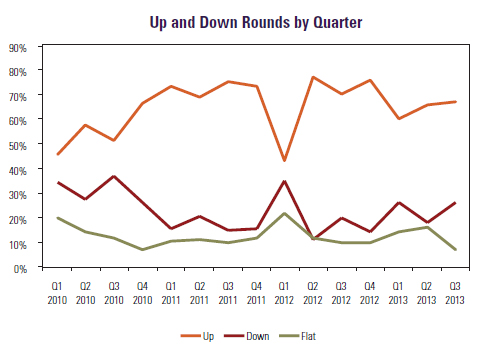

Up rounds represented 67% of all new financings in Q3 2013, a similar proportion as in Q2. Of the remainder, the percentage of down rounds increased sharply at the expense of flat rounds. Flat rounds dropped from 16% of all new deals in Q2 2013 to 7% in Q3, while down rounds increased from 18% to 26%. |

|

|

Valuations

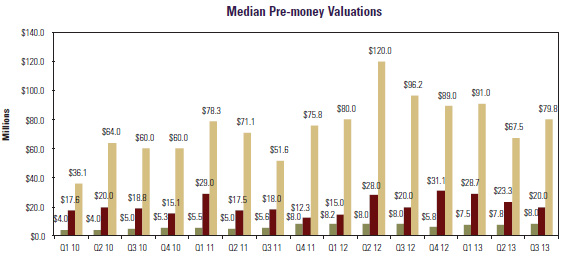

Company valuations in Series A deals backed by venture and corporate strategic investors rose modestly, from a median of $7.8M in Q2 2013 to $8.0M in Q3. The median pre-money valuation for Series B rounds declined from $23.3M in Q2 2013 to $20.0M in Q3, a figure that is also below the 2012 median Series B pre-money valuation of $21.0M. Conversely, the median pre-money valuation for companies completing Series C and later rounds rose from $67.5M in Q2 2013 to $79.8M in Q3.

|

Amounts Raised

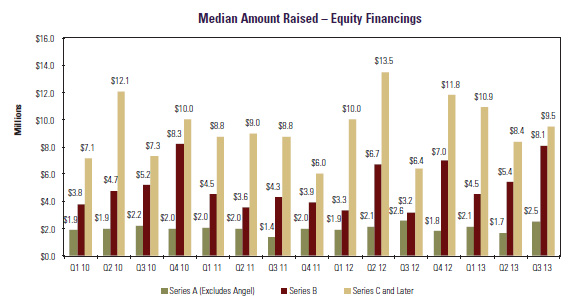

Median amounts raised in equity financings increased across the board, especially in Series B financings. For non-angel-backed Series A deals, the median amount raised increased from $1.7M in Q2 2013 to $2.5M in Q3. For Series B financings, the median amount raised increased substantially, from $5.4M in Q2 2013 to $8.1M in Q3, a level last exceeded in Q4 2010. For Series C and later transactions, the median amount raised increased from $8.4M in Q2 2013 to $9.5M in Q3. |

|

Deal Terms

Liquidation preferences. Deals with senior liquidation preferences continued to be slightly more prevalent in 2013 than in 2012, rising from 37% of all rounds in 2012 to 39% in Q1-Q3 2013. For up rounds, the proportion of financings with senior liquidation preferences rose from 30% in 2012 to 38% in Q1-Q3 2013, whereas in down rounds, the use of such preferences declined from 56% in 2012 to 40% in Q1-Q3 2013. As reported in previous quarters, this decline was partially offset by a large increase in the use of complex preference structures in down rounds, which rose from 0% of all deals in 2012 to 10% in Q1-Q3 2013.

Participation rights. The use of participating preferred decreased from 33% of all deals in 2012 to 28% in Q1-Q3 2013. Much of this decline was in up rounds (which comprised the majority of all deals), where usage declined from 33% of all deals in 2012 to 24% in Q1-Q3 2013. For down rounds, the decrease in the use of participating preferred was smaller, from 58% of all deals in 2012 to 53% in Q1-Q3 2013.

Dividends. The use of cumulative dividends rose from 9% of all deals in 2012 to 13% in Q1-Q3 2013.

Anti-dilution provisions. There was a small increase in the use of broad-based weighted-average anti-dilution provisions, from 92% of all rounds in 2012 to 95% in Q1-Q3 2013.

Pay-to-play provisions. The use of pay-to-play provisions declined in Q1-Q3 2013 as compared with 2012, dropping from 8% of all deals to 5%.

Redemption. The overall use of redemption provisions declined slightly, from 23% of deals in 2012 to 20% in Q1-Q3 2013. In up rounds, the use of investor-option redemption in deals dropped from 23% in 2012 to 19% in Q1-Q3 2013, while the use of investor-option redemption in down rounds remained at 35% over the same period.

To see how the terms tracked in the table below can be used in the context of a financing, we encourage you to draft a term sheet using our automated Term Sheet Generator. You’ll find a link in the Entrepreneurial Services section of wsgr.com, along with information about the wide variety of services that Wilson Sonsini Goodrich & Rosati offers to entrepreneurs and early-stage companies.

Private Company Financing Trends

(WSGR Deals)1

|

2011 |

2012 |

Q1-Q3 2013 |

2011 |

2012 |

Q1-Q3 2013 |

2011 |

2012 |

Q1-Q3 2013 |

All Rounds2 |

All Rounds2 |

All Rounds2 |

Up Rounds3 |

Up Rounds3 |

Up Rounds3 |

Down Rounds3 |

Down Rounds3 |

Down Rounds3 |

Liquidation Preferences - Series B and Later |

Senior |

47% |

37% |

39% |

34% |

30% |

38% |

79% |

56% |

40% |

Pari Passu with Other Preferred |

51% |

58% |

57% |

64% |

67% |

60% |

18% |

39% |

43% |

Complex |

1% |

2% |

3% |

1% |

2% |

1% |

3% |

0% |

10% |

Not Applicable |

1% |

3% |

1% |

1% |

1% |

0% |

0% |

5% |

7% |

Participating vs. Non-participating |

Participating - Cap |

16% |

14% |

17% |

17% |

13% |

16% |

22% |

17% |

25% |

Participating - No Cap |

26% |

19% |

11% |

24% |

20% |

8% |

46% |

41% |

28% |

Non-participating |

58% |

67% |

72% |

59% |

67% |

76% |

32% |

41% |

47% |

Dividends |

Yes, Cumulative |

11% |

9% |

13% |

11% |

10% |

13% |

19% |

12% |

10% |

Yes, Non-Cumulative |

78% |

78% |

73% |

79% |

81% |

77% |

73% |

78% |

84% |

None |

11% |

13% |

14% |

10% |

9% |

10% |

8% |

10% |

6% |

Anti-dilution Provisions |

Weighted Average - Broad |

91% |

92% |

95% |

91% |

92% |

94% |

80% |

85% |

97% |

Weighted Average - Narrow |

4% |

3% |

2% |

7% |

3% |

5% |

6% |

5% |

0% |

Ratchet |

3% |

3% |

1% |

2% |

2% |

0% |

6% |

8% |

3% |

Other (Including Blend) |

3% |

3% |

1% |

1% |

3% |

1% |

9% |

3% |

0% |

Pay to Play - Series B and Later |

Applicable to This Financing |

6% |

5% |

4% |

1% |

1% |

1% |

20% |

23% |

13% |

Applicable to Future Financings |

6% |

3% |

1% |

4% |

3% |

1% |

11% |

3% |

0% |

None |

88% |

92% |

95% |

94% |

96% |

98% |

69% |

74% |

88% |

Redemption |

Investor Option |

22% |

22% |

19% |

25% |

23% |

19% |

32% |

35% |

35% |

Mandatory |

2% |

1% |

1% |

2% |

1% |

1% |

3% |

3% |

0% |

None |

77% |

77% |

80% |

73% |

76% |

80% |

65% |

63% |

65% |

| 1We based this analysis on deals having an initial closing in the period to ensure that the data clearly reflects current trends. Please note that the numbers do not always add up to 100% due to rounding. |

| 2Includes flat rounds and, unless otherwise indicated, Series A rounds. |

| 3Note that the All Rounds metrics include flat rounds and, in certain cases, Series A financings as well. Consequently, metrics in the All Rounds column may be outside the ranges bounded by the Up Rounds and Down Rounds columns, which do not include such transactions. |

| |

Bridge Loans

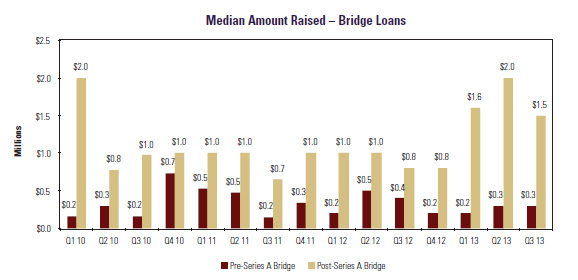

The median amount raised in pre-Series A bridge financings remained unchanged at $300K between Q2 and Q3 2013 but declined in post-Series A loans, from $2.0M in Q2 2013 to $1.5M in Q3. The median amount raised in pre-Series A bridge financings remained unchanged at $300K between Q2 and Q3 2013 but declined in post-Series A loans, from $2.0M in Q2 2013 to $1.5M in Q3.

Interest Rates. Data for Q1-Q3 2013 confirmed the previously reported trend of generally declining interest rates for pre-Series A bridge loans but generally increasing interest rates for post-Series A bridge loans. The percentage of pre-Series A bridges with annual rates under 8% increased markedly, from 64% of all deals in 2012 to 76% in Q1-Q3 2013. By contrast, the percentage of post-Series A bridge loans with annual interest rates above 8% increased from 15% of all deals in 2012 to 24% in Q1-Q3 2013. The percentage of post-Series A bridges with rates of less than 8% increased slightly, from 44% in 2012 to 45% in Q1-Q3 2013.

Maturities. Maturities for pre-Series A bridge loans remain substantially longer than for post-Series A loans. The percentage of pre-Series A deals with maturities of 12 months or more increased from 92% in 2012 to 98% in Q1-Q3 2013. For post-Series A loans, maturities of one year or more increased from 66% of loans in 2012 to 72% in Q1-Q3 2013.

Subordinated Debt. The use of subordinated debt increased between 2012 and Q1-Q3 2013 for both pre- and post-Series A bridge loans, rising from 13% of pre-Series A loans in 2012 to 28% in Q1-Q3 2013, and from 39% of post-Series A loans in 2012 to 57% in Q1-Q3 2013.

Warrants. Only a small percentage of pre-Series A loans have warrants, so we did not examine trends in warrant coverage for those deals. For post-Series A bridge loans, the use of warrants increased from 32% of all such deals in 2012 to 36% of deals in Q1-Q3 2013. In 2012, 33% of the post-Series A deals with warrants had 25% warrant coverage. This percentage declined to 7% in Q1-Q3 2013, while deals with more than 25% warrant coverage increased from 14% of deals with warrants in 2012 to 41% of such deals in Q1-Q3 2013.

Conversion. The percentage of pre-Series A bridge loans subject to an explicit price cap on conversion grew from 65% of deals in 2012 to 69% in Q1-Q3 2013; 88% of such deals in Q1-Q3 2013 were convertible at a discounted price, up substantially from the 79% figure in 2012. Conversely, the percentage of post-Series A bridge loans subject to a price cap on conversion fell from 24% in 2012 to 11% in Q1-Q3 2013, while the percentage of such deals convertible at a discounted price increased modestly to 57% of deals in Q1-Q3 2013 as compared with 52% in 2012.

Multiples. Provision for repayment at a multiple of the loan value in the event of an acquisition increased for pre-Series A loans from 16% of deals in 2012 to 28% in Q1-Q3 2013. The percentage of post-Series A loans with such a feature declined slightly, from 22% in 2012 to 21% for Q1-Q3 2013.

Bridge Loans1 |

2012

Pre-Series A |

Q1-Q3 2013

Pre-Series A |

2012

Post-Series A |

Q1-Q3 2013

Post-Series A |

Interest rate less than 8% |

64% |

76% |

44% |

45% |

Interest rate at 8% |

30% |

22% |

41% |

31% |

Interest rate greater than 8% |

5% |

2% |

15% |

24% |

Maturity less than 12 months |

8% |

2% |

34% |

28% |

Maturity 12 months |

30% |

23% |

36% |

41% |

Maturity more than 12 months |

62% |

75% |

30% |

31% |

Debt is subordinated to other debt |

13% |

28% |

39% |

57% |

Loan includes warrants2 |

8% |

4% |

32% |

36% |

Warrant coverage less than 25% |

20% |

0% |

42% |

52% |

Warrant coverage at 25% |

40% |

0% |

33% |

7% |

Warrant coverage greater than 25% |

20% |

100% |

14% |

41% |

Warrant coverage described as variable or "other" |

20% |

0% |

12% |

0% |

Principal is convertible into equity3 |

99% |

100% |

97% |

92% |

Conversion rate subject to price cap |

65% |

69% |

24% |

11% |

Conversion to equity at discounted price4 |

79% |

88% |

52% |

57% |

Discount on conversion less than 20% |

17% |

20% |

15% |

14% |

Discount on conversion at 20% |

54% |

61% |

46% |

44% |

Discount on conversion greater than 20% |

29% |

20% |

39% |

42% |

Conversion to equity at same price as other investors |

12% |

13% |

38% |

37% |

Repayment at multiple of loan on acquisition |

16% |

28% |

22% |

21% |

1We based this analysis on deals having an initial closing in the period to ensure that the data clearly reflects current trends. Please note that the numbers do not always add up to 100% due to rounding.

2Of the 2012 pre-Series A bridges that had warrants, 40% also had a discount on conversion into equity. Half of the 4% of the 2013 pre-Series A bridges that had warrants also had a discount on conversion into equity. Of the 2012 post-Series A bridges with warrants, 17% also had a discount on conversion into equity. Of the 2013 post-Series A bridges with warrants, 23% also had a discount on conversion into equity.

3 This includes notes that provide for voluntary as well as automatic conversion.

4Of the 2012 pre-Series A bridges that had a discount on conversion into equity, 4% also had warrants. Of the 2013 pre-Series A bridges that had a discount on conversion into equity, 2% also had warrants. Of the 2012 post-Series A bridges that had a discount on conversion into equity, 13% also had warrants. Of the 2013 post-Series A bridges that had a discount on conversion into equity, 16% also had warrants. |

[back to top]

An Introduction to Management Carve-Out Plans

By Scott McCall, Partner, Palo Alto, and Sriram Krishnamurthy, Associate, New York

The primary way to incentivize executives and key employees of privately held technology and life science companies is through the use of stock options. In particular, stock options often serve to compensate employees for their efforts to build company value with a successful merger and acquisition exit. Unfortunately, companies are sometimes forced to sell themselves in M&A transactions where the deal proceeds are insufficient to result in a meaningful return on outstanding stock options (i.e., an “underwater sale”). This situation typically arises due to a large amount of the transaction proceeds being required to satisfy the company’s liquidation preferences for preferred stockholders, leaving little to no purchase price remaining for holders of common stock or stock options covering common stock. Consequently, companies are often left with executives and key employees who are necessary to complete the M&A transaction but lack the requisite financial motivation to do so. This can create a disconnect between management and stockholders, with management wanting to stay the course, hoping to create a profitable return on common stock, and stockholders wanting to realize immediate liquidity by consummating an underwater sale.

A common incentive tool to address this potential disconnect is to put in place a so-called “carve-out” bonus plan. In a typical carve-out plan, a certain percentage of the deal proceeds or a fixed amount that otherwise would be paid to the company’s stockholders is set aside as a bonus pool to incentivize executives and other key employees to remain with the company through the closing of the M&A transaction. Thus, some value related to the transaction is realized by participants in the carve-out plan even though their common stock or options may have limited or no value.

This article discusses certain matters companies should consider when designing or adopting a carve-out plan. (Please note, for the sake of simplicity, this article does not provide a comprehensive analysis of all the corporate, tax, securities, accounting, and other issues involved with carve-out plans.)

Plan Eligibility: Management and Other Key Employees Only, or All Employees?

Companies typically limit participation in carve-out plans to executives and certain key employees who are necessary to drive the company towards completion of the M&A transaction. Allowing participation among a larger group of employees could either make the plan more costly to stockholders (because a larger percentage of deal proceeds is necessary to incentivize everyone) or result in allocations that are insufficient to properly incentivize all of the plan participants (because the bonus pool is being diluted among a greater number of people). Nevertheless, there are companies that culturally believe that all employees should be treated similarly, from executives down through the entire organization, and will create a carve-out plan that rewards employees beyond those critical to completing the M&A transaction.

Disclosure

Compensatory payments to officers and other executives may be required to be disclosed in connection with the M&A transaction as part of stockholder approval of the transaction or a Tax Code 280G stockholder approval of the payments (discussed in greater detail below). That means that employee stockholders who are not participants in the carve-out plan may learn of the bonuses through required stockholder disclosures or discussions with other employees and stockholders. Companies should be aware of the disclosures that may be required and consider how employee morale may be impacted.

280G

Also commonly referred to as the “golden parachute tax,” 280G is a penalty tax that can apply to certain individuals (officers, highly compensated individuals, and 1% stockholders) of a company involved in an M&A transaction. Put simply, if payments contingent upon an M&A transaction to such an individual equal or exceed three times his or her average compensation (or the 280G threshold) at the company over the prior five years, then the individual is subject to a 20% excise tax on the total contingent payments, in excess of one times his or her average compensation. This tax would be in addition to any other taxes that may be due on these contingent payments. In addition, the paying corporation is denied a U.S. federal income tax deduction equal to the same amount by which the individual is subject to the tax. Therefore, most transaction agreements will require a selling company to make representations and covenants that there will be no 280G issue.

Bonuses paid under a carve-out plan likely will be viewed as being contingent upon the M&A transaction, which will necessitate that the seller perform an analysis to see whether 280G might be triggered. If it is, privately held companies are able to “cleanse” the 280G issue if an individual’s right to receive or retain transaction-related payments in excess of the 280G threshold is subject to approval of more than 75% of the company’s disinterested stockholders (that is, shares held by or attributed to the individuals with the 280G issue being voted upon are excluded from the vote). Cleansing the 280G issue results in no excise tax for the individual and full availability of the tax deduction for the paying corporation. A 280G stockholder approval requires, among other things, that all material facts of 280G payments be disclosed to all stockholders entitled to vote, and not just a small subset of stockholders whose vote would be sufficient to satisfy the 75% approval requirement.

Accordingly, companies and their executives should prepare for the likelihood that certain allocations in a carve-out plan will become disclosed to all stockholders (which, depending on the company’s capitalization table, may include a significant number of rank-and-file employees).

Determining the Bonus Pool: Fixed Amount or Percentage of Proceeds?

The carve-out plan bonus pool generally is structured either as a fixed dollar amount or a percentage of the underlying proceeds from the M&A transaction. Currently, the predominant practice is to determine the bonus pool based on a percentage of the net proceeds received by stockholders in the transaction. Typical structures have a flat percentage of net proceeds (for instance, 10%) or a percentage of net proceeds after a minimum threshold has been achieved, with a sliding scale based upon increases in net proceeds above the minimum threshold amount (e.g., 10% for net proceeds in excess of $10 million increasing to 15% for net proceeds in excess of $25 million).

As net proceeds increase, the common stock ultimately may derive enough value for the need for the carve-out plan to lessen or disappear entirely (i.e., with enough proceeds, the outstanding stock option awards could have sufficient incentive value on their own). To address the possibility of overpayment or double-dipping (i.e., an employee receiving consideration in the carve-out plan as well as payments with respect to his or her stock options), companies may consider a structure in which the bonus payment phases out after a certain amount of net proceeds have been received, or provide for a dollar-for-dollar reduction of bonus payments to a participant by any amounts received with respect to his or her stock or options in the M&A transaction.

Payment Trigger: Closing of Transaction or Post-Closing?

As noted earlier, the purpose of a carve-out plan is primarily to motivate executives and key employees to remain at the company through an M&A transaction. Another motivation may be to incentivize plan participants to remain employed for some period following the transaction to help ensure a smooth transition and to make the transaction more attractive for the buyer.

Most plans require continued employment only through the closing of the M&A transaction. Companies taking this approach generally believe that the carve-out plan is to benefit seller stockholders and any post-transaction retention issues are the concern—and financial responsibility—of the buyer.

Sometimes, though, there are sellers willing to fund a portion of the post-transaction retention arrangement. For example, where the transaction involves deal consideration that is contingent on achieving post-transaction performance objectives (e.g., certain revenue targets), requiring continued employment through a defined period following the transaction can motivate plan participants to achieve the performance objective to maximize the amount of the bonus payment, as well as the amount of net proceeds to be paid to stockholders.

Timing of Payments and Section 409A

While some carve-out plans are set up to pay a fixed amount at the closing of the M&A transaction, it is more typical to pay bonuses at the same time and subject to the same terms and conditions as the corresponding net proceeds are paid to stockholders. Because most M&A transactions involve contingent post-transaction payments (e.g., amounts set aside in escrow to be available for any breaches of representations and warranties made by the seller in connection with the transaction, or earn-out payments contingent on achieving some performance goal following the transaction), some portions of carve-out plan bonuses generally are paid following the closing of the transaction.

As noted above, many carve-out plans only require continued employment through the date of the closing of the M&A transaction, raising the possibility that bonus payments could be earned in one calendar year but be payable in subsequent calendar years. This raises potential deferred compensation concerns under Tax Code Section 409A, or the deferred compensation penalty tax, which need to be considered when designing the carve-out plan.

Section 409A is an Internal Revenue Code provision meant to address abusive deferred compensation arrangements. It provides a set of rules for deferring compensation and receiving distributions of deferred compensation. The failure to comply with Section 409A rules on how to defer and receive deferred amounts can result in the person providing services to the company paying penalty taxes in addition to the regular taxes he or she would otherwise have to pay (20% additional federal income tax and, for those individuals who are California taxpayers, a 20% additional state income tax before 2013 and 5% from January 1, 2013), not to mention potential penalties and interest. Carve-out plans are usually structured to be exempt from Section 409A through use of the short-term deferral exception or to comply with its rules.

Compensation will be exempt from Section 409A as a short-term deferral if it is paid shortly following the date it is earned (payment should be made before the later of March 15 of the calendar year following the year in which it is earned or the 15th day of the third month following the end of the company’s fiscal year in which the payment is earned). Bonuses paid with respect to carve-out plans where employment is required through the closing date of the M&A transaction generally will fall within the short-term deferral exception. Regarding the portion of bonuses payable post-closing with respect to contingent consideration, there is an argument that such payments should not be considered earned until the amounts become due to be paid to stockholders, in which case they would fall within the short-term deferral exception. However, because continued employment is not required through the date the contingent payment becomes payable, there is some uncertainty as to whether the payments are considered earned as of the date of the change of control or the date the net proceeds become payable to stockholders. For this purpose, Section 409A provides a transaction-based rule that provides that if the bonus payments are paid at the same time and subject to the same terms and conditions as the corresponding net proceeds are paid to stockholders, then the bonuses will be deemed to comply with Section 409A and avoid the imposition of penalty taxes. This rule, however, is limited to net proceeds payable within five years of the closing of the M&A transaction, so if there may be contingent payments paid beyond that time, thought should be given as to how to cause the bonuses to comply with Section 409A.

Conclusion

While a carve-out plan can be an effective way of addressing the decreased employee incentive to help facilitate the close of an M&A transaction that results in low or no value for the holders of common stock, there are several points to consider before implementing such a plan. The above considerations are only a brief introduction.

[back to top]

Pros and Cons of Raising Seed Funding via Convertible Notes vs. Preferred Stock

By Sundance Banks, Associate, Palo Alto & SOMA

There’s a certain point in almost every pitch meeting between the founders of a start-up and potential investors where the conversation turns to how the company plans to raise its seed funding—via a convertible note financing or a priced preferred stock financing. They are the two primary methods for start-ups to raise seed funding, with convertible note financings becoming increasingly popular and likely the predominant vehicle for raising early-stage seed funding. It is a significant decision for both founders and investors, and it is important for each to understand the pros and cons.

This is the second in a series of articles comparing the impacts of issuing convertible notes vs. preferred stock in initial equity financings. In this article, we’ll explore in detail the pros and cons of raising seed financing via convertible notes vs. preferred stock from both the founders’ and investors’ perspectives.

Background

Traditionally, investors have dictated the form and terms of their investments; however, due to recent growth in the number of early-stage investors (such as angel investors, “super-angels,” and VC funds specifically focused on early-stage deals), founders have gained more leverage in these decisions (especially in particularly “hot” deals). As a result, the use of convertible notes in seed financings has increased significantly.

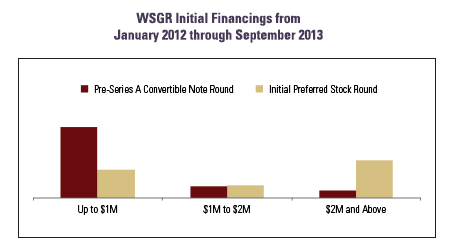

That said, it is also important to recognize that the size of the investment round may determine whether investors want to invest via convertible notes or in a priced preferred stock round. It is common for larger investments to be structured as preferred stock financings, as the investors will want to lock in a specific valuation, as well as the full range of control rights associated with preferred stock. Convertible notes are used much more frequently in smaller rounds, particularly in deals raising $1 million or less, while preferred stock financings are more common in deals raising $2 million or more. That said, it is also important to recognize that the size of the investment round may determine whether investors want to invest via convertible notes or in a priced preferred stock round. It is common for larger investments to be structured as preferred stock financings, as the investors will want to lock in a specific valuation, as well as the full range of control rights associated with preferred stock. Convertible notes are used much more frequently in smaller rounds, particularly in deals raising $1 million or less, while preferred stock financings are more common in deals raising $2 million or more.

When deciding whether to raise funds via convertible notes or preferred stock, it is important to understand the fundamental differences between them, including the near-term practical implications and the investors’ long-term objectives. While a convertible note is a debt instrument that pays interest and has a maturity date, the goal of the investor is not to be repaid with interest, but instead for the note to convert into preferred stock at a favorable valuation. The investors are putting money into the company in the form of debt, but with the long-term goals of an equity investment. However, the fact that the investment will be in the form of debt for a certain period of time (and that the notes may never automatically convert into equity) makes it very different from an initial equity investment in several ways. This presents a number of advantages and disadvantages to both the founders and investors.

Founders’ Perspective: Pros of a Convertible Note Financing

- Convertible Note Financings Are Generally Cheaper and Quicker: The leading rationale for raising seed funding via convertible notes is that convertible note financings are generally cheaper and faster to negotiate than preferred stock financings. The base documentation associated with a convertible note financing requires only limited documentation, and there are typically only a handful of key negotiation points between the parties. A preferred stock financing typically entails amending the company’s certificate of incorporation and entering into five or more additional agreements that spell out the specific terms of the sale of the preferred stock and the many rights that the preferred holders will have going forward (such as voting rights, registration rights, information rights, and pre-emptive rights).1 For instance, the total page count of the agreements executed in connection with a convertible note financing would typically be less than 25 pages, whereas the total page count of the agreements in a full-blown preferred stock financing would typically be 100 to 150 pages.2 As a result, legal fees for note financings are substantially less than for preferred stock financings.

- No Need to Establish the Valuation of the Company at the Time of the Note Financing: Raising funds via a preferred stock financing requires setting a valuation for the company, effectively determining the percentage ownership that the investors will receive. In many cases, it can be challenging for the founders and investors to agree upon a valuation for an early-stage company. For investors, it can be difficult to value a company that is little more than a few founders and a business plan; for founders, it can be difficult to justify a higher valuation if the product has yet to be built or is still in its beta testing. Thus, both investors and founders may have reasons to defer putting a valuation on an early-stage company and let a future investor (often a more seasoned venture capital firm) value the company in connection with a larger equity financing when there will be many more data points available to help establish the valuation. While convertible note financings do not require establishing a valuation for the company, in recent years most note financings have come to include a valuation cap provision that places a ceiling or “cap” on the pre-money valuation at which the notes will convert,3 and these valuation cap provisions can similarly become a sticking point in negotiations. Before the rise in popularity of valuation cap provisions, one common argument for raising funds via convertible notes was that it saved time because there was no need for the parties to negotiate the valuation. This rationale may not be entirely accurate in the current market, as any time saved by bypassing negotiations of a true valuation in a note financing may end up being spent negotiating the valuation cap.4

- Postponing a Valuation Can Help Keep Option Prices Low: Stock option grants are a key part of how start-ups compensate employees, and it is to the company’s advantage to be able to grant options with a low exercise price when possible, as the potential for a large increase in value creates a strong financial incentive. However, IRS regulations effectively require that the exercise price of an option grant be equal to the fair market value of the company’s common stock on the date of grant. Because equity financings require valuing the company, the company is then effectively bound to issue options with a correspondingly higher exercise price. Since convertible notes do not require a valuation, there is potentially an extended opportunity for the company to grant options with a lower exercise price, which can be a real advantage in recruiting and retaining talent.5

- Typically No Board Seat Given in Note Financings: Investors typically do not receive a board seat in connection with a note financing, which provides the founders with greater control prior to a preferred stock round, where the company would typically provide the lead investor with a board seat.

- Notes Don’t Typically Have Voting or Control Provisions: Investors in preferred stock financings typically negotiate several detailed provisions regarding voting and control matters, which give the investors a veto right over certain actions, such as an acquisition or the issuance of senior securities. Convertible notes typically do not have such provisions, providing the founders with more autonomy. For instance, in a preferred stock financing, the “protective provisions” in the certificate of incorporation would typically allow the preferred holders to block a future financing, which is not the case with most note financings. Conversely, if the company has not yet issued preferred stock, there is no need for the founders to worry about the need to obtain consent from the preferred stockholders for other matters that may otherwise require approval of the preferred stockholders, such as an increase in the company’s option pool.

Founders' Perspective: Cons of a Convertible Note Financing

- Noteholders Are Not Diluted by Equity Issuance Prior to Conversion: As a general matter, if there has to be a dilutive event to the company’s stock, it is advantageous to the founders for that dilution to be shared by all investors equally. For instance, if the company decided to increase the size of its option pool prior to the conversion of any outstanding convertible notes, the founders and other current stockholders would be diluted, but the noteholders would not be diluted. In contrast, in a scenario where investors had purchased preferred stock and the company then decided to increase the size of its option pool, all stockholders of the company would be diluted equally, meaning the founders would suffer less of the dilutive impact.

- Conversion of Notes in a Downside Scenario Can Be Very Dilutive: Convertible notes typically include a valuation cap that sets a ceiling on the valuation that would be used to calculate the price per share for conversion of the notes, but it is uncommon for convertible notes to include a floor on the conversion price. As a result, if the company’s business does not prosper and the notes convert at a low valuation, the noteholders will receive a much larger percentage of the company than if they had originally made their investment in the form of preferred stock.6

- Noteholders Will Have Strong Leverage upon Maturity if the Notes Have Not Converted: If the company cannot raise a preferred round that would trigger the conversion of the notes prior to the maturity date of the notes and the company does not have cash on hand to repay the notes (which would be very rare), upon maturity of the notes, the noteholders will have the right to demand repayment of the note as a creditor (despite the fact that most convertible notes are unsecured debt). Even if the noteholders do not force the company into bankruptcy or involuntary liquidation, they may require a recapitalization that is highly dilutive to the founders and other existing stockholders. If relations with the noteholders are cordial, the noteholders may agree to amend the notes to further extend the maturity date; however, this can be an awkward situation for founders, and it is something founders should consider several months prior to the maturity of the notes.7

- Note Conversion Discounts and Valuation Caps Can Create Extra Liquidation Preference upon Conversion: Pursuant to the terms of most convertible notes, the conversion discounts and valuation caps will result in a company effectively creating more liquidation preference upon conversion than the amount of money that the noteholders have invested. This results in the converting noteholders effectively having a liquidation preference greater than the standard of 1x the initial investment amount; if this differential is too large, it may not sit well with the new investors. One solution to avoid this type of “liquidation preference overhang” is to use a conversion discount formula in the convertible notes that provides that the “discount shares” are issued in the form of common stock (which would not have a liquidation preference), while the principal and interest on the convertible notes would convert into preferred stock without a discount. Another solution is to have the notes convert into an alternate series of preferred stock that is identical to the preferred stock issued to the new-money preferred investors, except that it has a lower per-share liquidation preference than the preferred stock issued to the new-money preferred investors. The converting noteholders’ per-share liquidation preference would be equal to (a) the total principal and accrued interest of the convertible notes divided by (b) the total number of shares the converting noteholders would receive upon conversion.8

Investors’ Perspective: Pros of a Convertible Note Financing

- Convertible Note Financings Are Generally Cheaper and Quicker: Same advantages as described above.

- No Dilution for Issuance Prior to Conversion: During the period prior to conversion of the notes, the noteholders won’t be diluted by any company increases to its option pool or other equity issuances.

- Possibility of Demanding Repayment upon Maturity: Assuming the notes have not automatically converted prior to maturity, in a scenario where the investors want to cut their losses, the investors can demand repayment of the notes upon maturity. However, this is a relatively rare scenario, as the company would not likely have the cash on hand needed to repay the notes and the investors would be effectively bankrupting the company.

- Potentially Higher Repayment upon Acquisition Prior to Conversion: Some investors negotiate for economic protections in convertible notes to provide an enhanced return in a scenario where the company is acquired prior to the conversion of the notes—for instance, a payout of 2x or 3x the original principal amount if the company is acquired prior to conversion of the notes. Such provisions can provide a better return to investors than they would have received in an equity deal, where the preferred stockholders may only receive the standard 1x liquidation preference in the event of an early-stage acquisition.9

Investors' Perspective: Cons of a Convertible Note Financing

- Limited or No Control Rights: Unless special terms are negotiated in a side-letter agreement, noteholders typically would not have any rights to control how the company is managed, while in a preferred stock financing, the investor would typically have certain veto rights and, potentially, the right to a board seat.

- Possibility of Limited Say on Terms of Next Preferred Round: Most convertible note financings address the specifics of the conversion price of the notes (typically by including a conversion price discount and/or a valuation cap); however, note financings typically do not specify the other terms of the preferred stock that will be issued upon conversion. If the noteholders won’t be leading the preferred round in which the notes will be converting, they may not have a say regarding several of the fundamental rights of preferred stock.10

- Often No Pro Rata Pre-emptive Rights: Most convertible notes do not entitle noteholders to receive pre-emptive rights to purchase their pro rata share of securities offered by the company in future financings. Pre-emptive rights are commonly provided to investors in preferred stock financings, and they can be very valuable to investors in upside scenarios.

- Notes May Not Price-In Risks as Effectively as Preferred Stock: A preferred stock financing requires setting a valuation on the company, which allows the investors the opportunity to price-in any and all risks associated with the investment. While the use of valuation caps has given investors more certainty regarding the economic conversion terms of convertible notes, there are still several uncertainties and risks that cannot be adequately priced-in to the investment. For instance, an early angel investor in a note financing round faces the risk that the company may not be able to raise the rest of the note financing round or a future preferred round.

- Notes Do Not Start the Clock for “Qualified Small Business Stock” Tax Treatment: The investor five-year holding period for “qualified small business stock” tax treatment under Internal Revenue Code Section 1202 does not start until the notes have been converted into equity, which can present adverse tax consequences for investors if there is an early exit.11

Conclusion

In most cases, investors will still have a very large role in the decision about whether to raise an equity or a debt round; however, it is essential for founders to understand the advantages and disadvantages of raising funding via convertible notes vs. preferred stock and to discuss with their investors how they want to raise funds early in the process. Please email sbanks@wsgr.com or another member of the firm’s entrepreneurial services practice if you have any specific questions regarding seed financings and recent market trends.

WSGR Resources

1 Some counter that the rationale that note financings are quicker and cheaper than preferred stock financings is not true when compared with preferred stock financings using stripped-down “series seed” financing agreements. By removing certain provisions that have typically been included in preferred stock financing agreements (e.g., registration rights and anti-dilution rights) and standardizing other provisions, such agreements can provide an efficient, cost-effective alternative for certain early-stage preferred stock financings. However, there can be several challenges to realizing the cost savings of such standardized documents. For instance, the parties may negotiate terms that deviate from standard off-the-shelf forms and require significant customization. Additionally, these documents may not scale well to future preferred financings, as many of the more detailed rights that are not included in such agreements at the seed financing stage will be required by the investors leading the company’s next preferred financing round.

2 In the past, many note financings also included the issuance of warrants to purchase common stock. However, due to the added complexity of issuing warrants, many investors no longer request them. (For instance, in pre-Series A note financings during Q1-Q3 of 2013 in which WSGR represented one of the parties, only 4% of all note financings included the issuance of warrants.) As a result, the primary economic sweeteners of convertible notes are only (a) the accruing interest on the note and (b) the potential benefit of a conversion discount and/or valuation cap.

3In pre-Series A note financings during Q1-Q3 of 2013 in which WSGR represented one of the parties, 69% of all note financings included a valuation cap. See the "Bridge Loans" table on page 5 of this report for more information on recent trends in note financings.

4 To avoid prolonged negotiations over the valuation cap, it can be helpful to recall that a valuation cap is not a stand-in for the company’s valuation at the time of the note financing—instead, it is the maximum valuation at which the investor would be willing to convert his or her note at the time of the company’s next preferred equity financing, without requiring compensation of additional shares.

5 It should be noted that some attorneys and independent valuation firms continue to debate whether the issuance of convertible notes should affect the valuation of a company’s common stock.

6 See the Q1 2013 issue of The Entrepreneurs Report for a detailed illustration of the potential dilutive impact of convertible notes in a downside scenario.

7 Raising funds via the issuance of “convertible equity” or a “convertible security” is an alternative to using convertible notes that avoids this problem. In short, convertible equity is a type of security that is very similar to convertible debt, but it does not include provisions providing for the payment of interest or repayment upon maturity. Convertible equity maintains many of the features of convertible notes that are geared toward conversion into preferred stock and can include a conversion price discount, a valuation cap, and many other common terms associated with convertible notes. While the use of convertible equity is increasing in the venture community, it is not currently used as frequently as convertible notes or preferred stock.

8 For example, if the new-money investors were purchasing Series A Preferred Stock for $1.00 per share and there were also convertible notes converting into preferred stock with a 20% conversion discount, the noteholders would convert into Series A-1 Preferred Stock, which would have a liquidation preference based upon an $0.80 price per share but would otherwise be identical in terms to the Series A Preferred Stock. However, there are two potential complications to this strategy. First, it can require amending the notes prior to the financing to permit conversion to an alternative series of preferred stock. The second potential complication applies to situations where a company has issued notes with different conversion discounts and/or valuation caps (an increasingly common trend). This can result in a scenario where these different notes would be converting into preferred stock at multiple different conversion prices. Using the above strategy to eliminate the liquidation preference overhang in such scenarios requires issuing multiple series of preferred stock (e.g., Series A, Series A-1, Series A-2, etc.), resulting in a cluttered capitalization table and other administrative complexities.

9 Holding debt instead of equity can also provide an advantage for investors in a downside liquidation scenario, as the company will have a legal obligation to repay all debt before making any distributions to equity holders (even preferred stockholders).

10 Some investors address this uncertainty by spelling out certain minimum rights that the preferred stock to be issued upon conversion must have (typically in a preferred stock term sheet that is attached to the notes as an exhibit). However, negotiating the specific terms of the preferred stock in advance can detract from the primary advantages of a convertible note financing—keeping the investment quick, simple, and economical.

11 With respect to capital gains tax, in general, the holding period of a convertible note prior to conversion can potentially be counted towards the long-term capital gains tax holding period, assuming the note converts into preferred stock pursuant to its terms.

PitchBook and Dow Jones VentureSource Rank WSGR No. 1 in Venture Financings

PitchBook has released their inaugural Venture Capital Valuations & Trends report, in which Wilson Sonsini Goodrich & Rosati ranked first for early- and late-stage venture deals completed in the 12-month period from Q4 2012 to Q3 2013. The firm was credited with 137 early-stage and 108 late-stage deals, while its nearest competitors advised on 81 early-stage and 76 late-stage deals during the period. These rankings and the full report can be accessed at http://pitchbook.com/4Q2013_VC_Valuations_and_Trends_Report.html.

In addition, Dow Jones VentureSource's legal rankings for issuer-side venture financing deals in Q1-Q3 2013 placed Wilson Sonsini Goodrich & Rosati ahead of all other firms by the total number of rounds of equity financing raised on behalf of clients. The firm is credited as legal advisor in 151 rounds of financing, while its nearest competitor advised on 101 rounds of equity financing. According to VentureSource, WSGR ranked first nationally in Q1-Q3 2013 issuer-side deals in the following industries: information technology, healthcare, business and financial services (tied), clean tech, communications and networking, consumer services, electronics and computer hardware, energy and utilities (tied), industrial goods and materials, medical devices and equipment, and software. |

For more information on the current venture capital climate, please contact any member of Wilson Sonsini Goodrich & Rosati's entrepreneurial services team. To learn more about WSGR's full suite of services for entrepreneurs and early-stage companies, please visit the Entrepreneurial Services section of wsgr.com.

For more information about this report or if you wish to be included on the email subscription list, please contact Eric Little. There is no subscription fee. |

This communication is provided for your information only and is not intended to constitute professional advice as to any particular situation. Please note that the opinions expressed in this newsletter are the authors' and do not necessarily reflect the views of the firm or other Wilson Sonsini Goodrich & Rosati attorneys.

© 2013 Wilson Sonsini Goodrich & Rosati, Professional

Corporation

Click here for a printable version of The Entrepreneurs Report |