|

From the WSGR Database: Financing Trends for 1H 2017

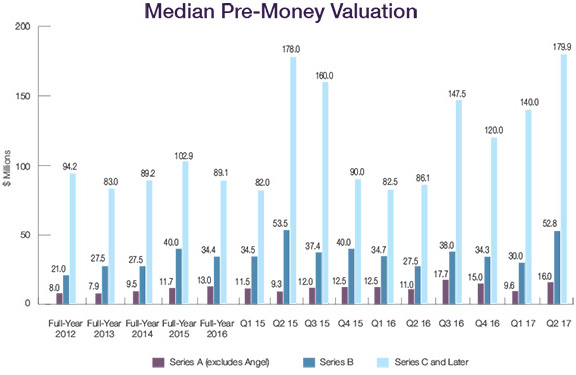

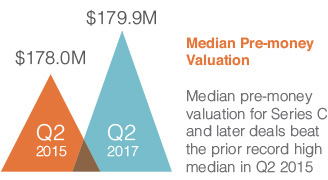

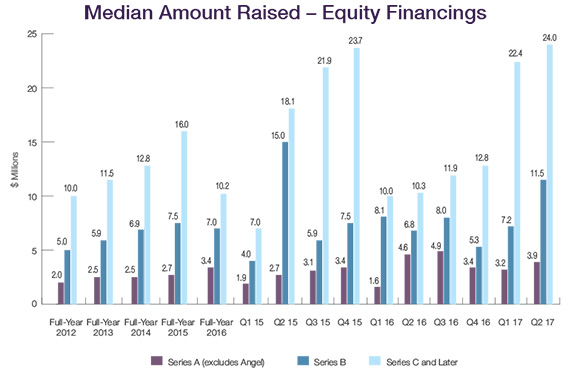

Strong median pre-money valuations for all rounds of financing ushered in nearly unprecedented median amounts raised in 1H 2017, particularly for Series C and later financings. Late-stage companies enjoyed pre-money valuations that far exceeded the five-year median of $97.4 million, with the median valuation rising to $179.9 million in Q2 2017. Amounts raised in Q2 2017 likewise outpaced the five-year median nearly two-to-one, with a median amount raised of $24.0 million, exceeding the very strong median of $22.4 million in Q1 2017.

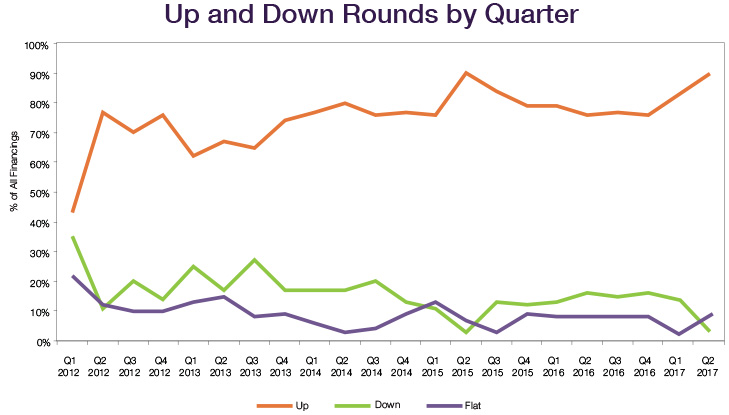

Up and Down Rounds Up rounds rebounded in the first half of 2017, constituting 90% of Q2 2017 Series B and later financings—a high reached only once before, in Q2 2015. The corresponding decrease in down-round and flat-round financings also mirrors that of Q2 2015, with down rounds falling from 14% of financings in Q1 2017 to just 3% in Q2 2017. Flat rounds rose from 2% of financings in Q1 2017 to 8% in Q2 2017.

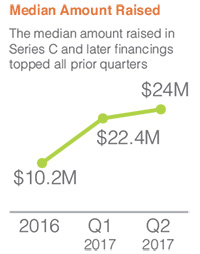

Amounts raised in Q2 2017 were also up across the board. The median amount raised for Seed and Series A rounds increased modestly from $3.2 million in Q1 2017 to $3.9 million in Q2. The median amount raised in Series B financings rose from $7.2 million in Q1 2017 to $11.5 million in Q2—well over the full-year 2016 median of $7.0 million. The median amount raised in Series C and later financings in Q2 2017 topped all prior quarters, reaching $24.0 million—up from $22.4 million in Q1 2017, and more than twice the full-year 2016 median of $10.2 million. A handful of mega-deals raising more than $100 million in Q2 2017 contributed to the high median, but even when excluding those deals , the median amount raised remained above average at $18.5 million, exceeding the five-year median of $12.7 million.

The use of senior liquidation preferences in post-Series A rounds declined slightly, from 38% of all such rounds in 2016 to 31% in 1H 2017. Pari passu liquidation preferences increased from 57% of all such rounds in 2016 to 68% in 1H 2017. The percentage of financings having a liquidation preference with participation fell to 14% in 1H 2017, lower than in any of the prior four full years. Similarly, the percentage of financings with no participation increased from 81% in 2016 to 86% in 1H 2017—a higher percentage than in any of the prior four full years. Data on deal terms such as liquidation preferences, dividends, and others are set forth in the table below. To see how the terms tracked in the table can be used in the context of a financing, we encourage you to draft a term sheet using our automated Term Sheet Generator, which is available in the Start-Ups and Venture Capital section of the firms website at www.wsgr.com.

Private Company Financing Deal Terms (WSGR Deals)1

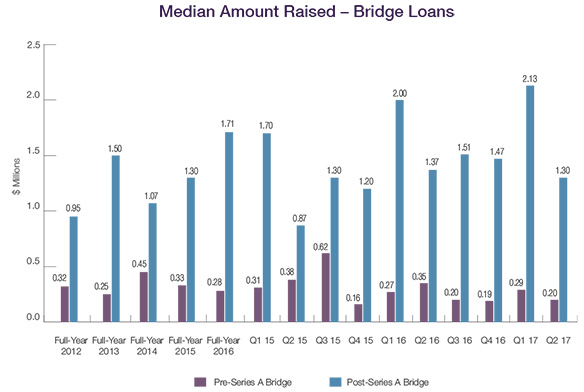

Bridge Loans The median amount raised in bridge loans fell for both pre- and post-Series A deals in Q2 2017, with pre-Series A bridges declining slightly from $0.29 million in Q1 2017 to $0.20 million in Q2, below the $0.28 million median for full-year 2016. The median amount raised in post-Series A bridges similarly fell, declining from $2.13 million in Q1 2017 to $1.30 million in Q2. Deal Terms – Bridge Loans The percentage of pre-Series A bridge loans subordinated to other debt rose from 20% in 2016 to 44% in 1H 2017. The number of pre-Series A bridge loans that are convertible to equity at a discounted prices fell from 82% in 2016 to 75% in 1H 2017, though 91% of those that do convert at a discount received a discount rate of 20% or more on conversion. Twenty-six percent of post-Series A bridge loans had interest rates greater than 8% in 1H 2017—a significant increase from the 17% figure in 2016. In addition, the percentage of loans with maturity periods of less than 12 months increased from 29% in 2016 to 48% in 1H 2017, reflecting a trend toward shorter-term, higher-interest loans. Fewer loans were convertible in 1H 2017, at 89% as compared to 92% in 2016.

Bridge Loans Deal Terms (WSGR Deals)1

Methodology for WSGR's Entrepreneurs Report

An Interview with Greg Gottesman of Pioneer Square Labs

Craig: Tell us about Pioneer Square Labs (PSL). It's not a venture fund. Its not an accelerator or an incubator. Instead, you describe PSL as a start-up studio. Describe how PSL works and how it differs from traditional, early-stage business models for investors. Greg: Thats right. Pioneer Square Labs is a start-up studio. As you know, venture firms raise money to invest in teams that have already developed a specific business opportunity. Then you have accelerators, which choose a select number of teams from hundreds that apply and then take a small amount of equity in return for putting on a program over a short amount of time. PSL is different. We often come up with the idea ourselves, or well work with an entrepreneur at the earliest stages before a company is really formed. Sometimes, theres a kernel of an idea where an entrepreneur comes to us and says, "I've been thinking about this space." Or we may have worked on an idea in a particular space ourselves, and then, either on our own or with an entrepreneur, well create a company, get it validated, raise money, find the right CEO and team, spin it off, and hopefully help make it really successful. Craig: Can you explain how PSL was formed? Greg: PSLs team of managing directors have known each other for a long time. Mike Galgon was one of the co-founders of aQuantive, which was sold to Microsoft in 2007 for over $6 billion. More than 20 years ago, Mike and I went to business school together. In fact, we were section mates and did our field study together. Geoff Entress and I worked together for nine years at Madrona Venture Group. I hired him there and we have always been close friends. It also comes back to how much fun I had working on the early project that became Rover.com. I originally started it within Madrona; I was the early CEO of that company, still doing my day job, and brought in an incredible entrepreneur named Aaron Easterly who was an entrepreneur-in-residence at Madrona. Very early on, he took over and made Rover.com into a truly incredible company, and its now the largest online pet services company in the world. Working with Aaron on that was so enjoyable and invigorating that I thought, Gosh, this seems like fun, maybe we could do this more. I approached my partners at Madrona and said, Hey, we've got some great ideas; maybe we should start our own studio to do more of these Rovers. Paul Goodrich, one of the partners at Madrona, had done something similar with Redfin and a company called Z2Live. I was involved in those, and it was just really fun. So, we started Madrona Venture Labs and spun off some companies there—one called Mighty AI and another called ReplyYes. They were successful, but it always felt like there was an opportunity to really scale and involve more venture firms and angels. I reached out to Geoff, and we agreed to meet at Bakeman's—a well-known cafeteria here in Seattle. We also invited Mike, and expected him to say that we were crazy, but he enthusiastically said he was in. Mike, Geoff, and I, along with Ben Gilbert, a young superstar at Madrona Labs, teamed up, raised some money, and that became Pioneer Square Labs. To date, weve spent roughly $5 million of capital, and the equity value of the companies we've created so far is approximately $100 million. Eventually, to become the best platform in the world for entrepreneurs, we realized we needed to hire an additional managing director. When I was at Madrona, I helped to hire Julie Sandler, who had risen up to become a partner at Madrona. She recently joined us as our fourth managing director. Were really lucky to have her on the team. So currently, Mike, Geoff, Julie, and I are PSLs managing directors. Craig: How has everything gone since you launched in October 2015? Greg: Weve spun off six companies so far, all of which have received meaningful venture funding. We worked extensively on 63 ideas. Of those, we killed 57 and spun out six. Our hit rate is low, but only because we look for an idea that has traction that we can validate with customers. Then, we look for an incredible team that wants to be a part of it and offer the team meaningful equity. Ultimately, we explore whether we can get the concept funded and get customers to actually buy the service or product were trying to sell. Craig: So, of the six companies youve spun out, how many were developed by PSL? Greg: Four ideas were developed by us, whether it was people here at PSL or our investors or friends. The other two ideas came from entrepreneurs or founders who came to us. Craig: I know your original business model was one where PSL comes up with its own ideas, but Im guessing you anticipated there could be people whod come to you with ideas, right? Greg: I expected it to happen, but the frequency and volume has been much greater than I expected. Right now, at least half of the ideas are coming from founders or entrepreneurs who approach us. We currently have five entrepreneurs-in-residence working with us, and typically working on their own ideas. That part of our business has grown much faster than expected, compared to the ideas that we come up with ourselves. Craig: You mentioned that youve eliminated a lot of ideas in addition to those that were eventually spun out as success stories. How do you decide which ideas are going to make it through and which ones to present to potential investors? Greg: During our first year, ideas we killed were dropped because, for example, we found we couldnt get customers to pay for the product, the economics werent as good as we thought, or there was stiff competition. But most ideas fail because customers aren't as interested as wed hoped in paying us for the service were building. We have a talented digital marketer here named Peter Denton who helps us determine how much it's going to cost us to acquire a customer and what the potential value of that customer could be. More often than not, we find that it costs us more money to acquire a customer than we had expected and that customers simply aren't as interested as we had hoped. For example, we looked at the insurance space for a long time and we tried all kinds of Facebook or Google ads and landing pages to get customers to show up, but we just couldn't get them to show up and sign up at a reasonable cost. But sometimes we find that customers are really interested and it's inexpensive to acquire them, and that's when we say, OK, there might be something here. For a company to get spun out, we have to believe there's a real value proposition—that it's going to work for customers, and customers are telling us that theyre interested. We also need to know we can find the right team and the backing to make it successful. Craig: If youre comfortable discussing economics, what does a cap table look like for self-generated ideas and how do you determine how much equity to allocate to PSL versus the founding team? Greg: Theres no set way because every case is different. Of course, both the founder and PSL need to have meaningful equity. For PSL, the balance needs to make sense for us to devote resources to the idea. And the balance also needs to make long-term sense for the founder, because the founder will spend the next several years of his or her life pursuing the idea. In addition, the balance needs to appeal to the venture funding sources that want to see the team and founders have strong incentives going forward. Were flexible and open to any structure that makes sense. Many times, especially if it's the founder's idea, we split equity 50/50, because thats just an easy way to do it. Other times, if its our idea, the split is slanted more towards us. But there are cases when were perfectly willing for the slant to be towards the founder, especially when that person has come to us and is clearly bringing a huge amount to the table. Again, every case is different. Craig: Can you tell us how PSL is structured and funded, and how that translates into what happens to the portfolio companies? Greg: Weve raised money from 13 venture firms and 50 of the top angels in the Seattle area and some from Silicon Valley. Whats great is that, to date, all of the companies that have spun out and received venture funding have had participation and a lead investor from one of PSLs investors. That doesn't need to be the case, and over time we'll have investors lead our deals that were not previously investors in PSL. Our investors are closer to the companies because we make it a point to communicate with them every month about which companies are getting traction and seeking funding. Communication has also helped get the spin-outs funded relatively quickly. Craig: Contractually, do VC funds from PSL get a first look? Greg: Not contractually, but given the nature of the relationship and our frequent communication with them, theyre more informed about whats going on at PSL. Now, there are a lot of other venture firms with whom we also have close relationships, which is to the advantage of our PSL investors because theyre backing us and want PSL to be successful. Were receptive to anyone who wants to invest in PSL companies. Let me add that the decisions about where to take funding are not PSL decisions. The core value of PSL is that it's about the entrepreneur. He or she makes the key decisions. Craig: So, if you and a CEO you brought in to run a company are pursuing funding, youre both engaged in conversations with investors, but the entrepreneur decides how they want to fund the company, right? Greg: Correct. When we bring on an entrepreneur, we make it clear that we work for the entrepreneur. We can influence and give advice, and we may have strong opinions, but ultimately we work for the entrepreneur, and our goal is to make the entrepreneur as successful as possible. When I started PSL, one of the conscious decisions we made was that we wouldn't call ourselves co-founders, because it's about the entrepreneurs, and making them successful. Everyone here believes and understands that. Craig: Are start-up studios a model that can be replicated in Silicon Valley, Boston, Tel Aviv, or Sao Paulo? Greg: Start-up studios are hot all of a sudden. There's Science in LA and BetaWorks in New York. Theres another one in Pasadena called Idealab, which may be the oldest start-up studio. There's one called Expa in Silicon Valley and others in certain markets around the world. All of them do things a bit differently, but they all depend on finding great entrepreneurs to work with. Theres not really a shortage of ideas, but its difficult to find the world's best entrepreneurs and convince them to join in. Craig: Are the entrepreneurs youre working with more experienced at starting companies, or are they first-timers? Greg: Surprisingly, more than half so far have been serial entrepreneurs. We thought most would be first-time entrepreneurs. Of the first-timers, some are, for example, superstars from Amazon who think its time for me to run a company, but Im not sure how to do that, so Ill go to PSL because their experience will make the process smoother. But interestingly, many of our spin-out entrepreneurs are individuals whove run companies several times. They tell us we basically eliminate the harder stuff, and if the company is successful, theres more than enough equity for everyone to make very meaningful returns. Craig: What is it that you're making easier for experienced entrepreneurs that they cant do themselves? Presumably, many of them have started a company, been through the incorporation process, built teams from scratch, raised venture money, and so on. Greg: Some entrepreneurs need help validating their idea, and then quickly spinning up the idea with our developers, designers, or digital marketing team. Robert Schulte, the CEO of LumaTax, told us that the time from when he came to us with an idea to the time he got funded was about three-and-a-half months. He said it would have taken him 18 months if he were doing it himself. So, we cut the idea-to-market-to-funding time down dramatically for him. We also provided high-quality developers and designers, and helped him recruit a team to find funding. It was a pleasure because he knows exactly how to be a CEO, and leveraged our resources effectively. Other entrepreneurs can do the same and get to market faster, and hopefully do so with a much higher valuation than they would otherwise get, because PSL is good at figuring out how to validate ideas in a way that appeals to financing partners. Also, its difficult right now to hire great talent. One of the things that people ask about PSL is how we come up with all these ideas, but thats not the constraint. We have more ideas than we could ever execute on. The real constraint is talent. Then capital. Then ideas. Were not perfect at it, but we do have access to a lot of amazing professionals who have helped every team fill out its ranks. Craig: Looking at the Seattle market, theres significant demand for talent. Both Amazon and Microsoft are here. And nearly every major Silicon-Valley-based tech company has opened an engineering center here and is recruiting. How do you guys help your early-stage start-up companies compete against tech giants that have billions of dollars and are throwing cash at employees? Greg: Its hard for any start-up to compete on the same playing field for talent, at least as to salary. But there are talented people who want to be a part of starting something. Maybe thats as an early founder. Maybe thats as part of a team. They may feel they can make a bigger contribution. Or maybe that person is excited about a certain space. If someone really wants to be at Amazon, Google, or Microsoft, then thats probably where they're going to go or stay. But there are incredibly talented people at those companies who may want to make the leap. We have very high-quality companies that are funded or about to be funded. So, if you're ready to do a start-up, were an incredibly good place to check out to see what we're working on. Out of six spin-outs, we have more than 25 positions open, particularly for engineers and designers, but also for marketing and business folks. Of course, we are always looking for great leaders as well. Craig: Does PSL have an in-house recruiter? Greg: We dont. But thats because we want to get prospects connected directly to decision-makers, and typically those are individuals at each company. Some of our companies have recruiters, especially if theyre hiring more quickly. We may add an in-house recruiter as we scale up. Craig: How many emails do you receive from people who say, Im at Amazon or Microsoft or Google right now and I really want to do a start-up. I read about Pioneer Square Labs. I dont have an idea, but I'm a smart engineer and I want to join a company. Can you help me? Greg: I get several emails like that every week. Usually the emails are from individuals saying they want to start something or join a company. Not everyone is going to be a great fit, but usually there's one company thats looking for someone with a specific skill set. I view this as a long game and will always make connections with people outside of PSL. If we can help get more people into the start-up ecosystem who want to be in the system, thats good for everybody and it's good karma. Craig: How is the market for PSL, in terms of the companies spinning out and raising funding? And more broadly, how do you feel about the funding environment for early-stage companies? Greg: Funding is pretty good for early-stage companies right now. Companies with good ideas and great entrepreneurs get funded. What I've been thinking about lately is how can PSL start thinking more boldly and creatively? The usual path is that a company with a good CEO and idea starts up, raises a couple million dollars from a certain set of funders that everyone else is trying to raise money from. Then they hit their milestones and get additional capital, maybe another $5, $10, or $20 million, again from the same set of funders. Then they go try to hit more milestones and raise more money from the same usual suspects. What Ive been thinking about is who invented the rules of this game weve been playing for 20-plus years, and why are we playing by these rules? It seems like those entrepreneurs and investors in our space that dont play by those rules are typically the most successful people. So one of my questions about fundraising is how can we get more capital sources into our ecosystem? Theres all kinds of wealth sitting on the sidelines and traditionally the individuals who have been able to access that wealth have been a select few. One of the things I want to work on with our companies is, when you start getting real traction, and there's real opportunity, how do you get that alternative non-traditional capital? Craig: What are some examples of those capital sources? Family offices, for example? Greg: There are family offices, sovereign wealth funds, pension funds, foundations, and other types of capital out there. Sometimes it feels like were playing VC Candyland and everyones playing on the same game board. This may not be for every company, but for some companies where there's real traction and a big opportunity, how can we think more boldly about going after capital? A company like Rover clearly has demonstrated incredible traction and has substantial revenue, and thats when non-traditional sources of capital come looking for you. But before that, we can do a better job of letting those capital sources know we're here. How do we continue to play the game with the same players, but also expand the pie? Craig: Any other thoughts about whats ahead for PSL? Greg: Our mission is to create the best platform in the world for entrepreneurs—thats all we think about. What were trying to do is be a place for someone who doesn't have an idea, but is looking for one, or someone who has a kernel of an idea but doesnt know what the next steps are. How do we make it irresponsible (to quote Jeff Bezos) for an entrepreneur in this area to not come and talk to us about a company? We want to be helpful in every possible way, and we want to make it very easy for entrepreneurs to work with us and for them to feel that it can lead to more success. Were willing to give very meaningful equity and to help as much as we can, as long as we feel like we are working with someone who is exceptional and committed.

This communication is provided as a service to our clients and friends and is for informational purposes only. It is not intended to create an attorney-client relationship or constitute an advertisement, a solicitation, or professional advice as to any particular situation. © 2017 Wilson Sonsini Goodrich & Rosati, Professional Corporation Click here for a printable version of The Entrepreneurs Report |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

The high pre-money valuations boosted the percentage of up rounds significantly, to 90% of all Series B and later financings in Q2 2017. The median amount raised in bridge loans fell in Q2 2017, particularly for post-Series A bridge loans, which dropped from $2.13 million in Q1 2017 to $1.30 million in Q2. However, that figure still exceeded the five-year median of $1.25 million.

The high pre-money valuations boosted the percentage of up rounds significantly, to 90% of all Series B and later financings in Q2 2017. The median amount raised in bridge loans fell in Q2 2017, particularly for post-Series A bridge loans, which dropped from $2.13 million in Q1 2017 to $1.30 million in Q2. However, that figure still exceeded the five-year median of $1.25 million.

Amounts Raised

Amounts Raised Deal Terms - Preferred

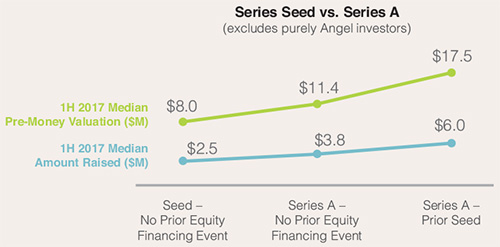

Deal Terms - Preferred Series Seed financings have become far more common in recent quarters, meaning that in many cases the Series A transaction is not a companys first financing event. We bundle Seed and Series A financings together for purposes of tracking trends in this quarterly report, but we have collected enough data to do a breakdown of Series Seed and Series A pre-money valuations and amounts raised in financings with—and without—a prior equity round.

Series Seed financings have become far more common in recent quarters, meaning that in many cases the Series A transaction is not a companys first financing event. We bundle Seed and Series A financings together for purposes of tracking trends in this quarterly report, but we have collected enough data to do a breakdown of Series Seed and Series A pre-money valuations and amounts raised in financings with—and without—a prior equity round.

Wilson Sonsini Goodrich & Rosati partner Craig Sherman recently sat down with Greg Gottesman, co-founder and managing director of Pioneer Square Labs, a Seattle-based studio that creates and launches technology start-ups. Below is a selection of highlights from their discussion.

Wilson Sonsini Goodrich & Rosati partner Craig Sherman recently sat down with Greg Gottesman, co-founder and managing director of Pioneer Square Labs, a Seattle-based studio that creates and launches technology start-ups. Below is a selection of highlights from their discussion.