Spring 2012 New Procedures for Challenging Patent Validity By Jim Heslin, Partner, and Doug Portnow, Associate For many years, U.S. patent attorneys have either craved or dreaded implementation of a U.S. Patent and Trademark Office (USPTO) procedure similar to opposition proceedings in Europe. European oppositions are used by companies to narrow the claims of their competitors’ patents when they believe that those claims are either invalid or overly broad. The procedure works very well in Europe, where more than 10 percent of all granted patents historically have been opposed, and where the availability of oppositions is likely one reason (among many) why patent litigation is far less prevalent than in the United States. Last year, as part of the America Invents Act, Congress leapfrogged the European Patent Office by creating two different post grant procedures: post grant review (PGR) and inter partes review (IPR). While similar in many respects, each of these procedures fits a different niche and will be useful under different circumstances.1 PGR is most similar to the European opposition process in that it must be filed within nine months of the patent grant date and allows a wide variety of invalidation arguments, including prior art, lack of support, and claim overbreadth. In fact, PGR may be instituted upon any showing that it is more likely than not that at least one claim challenged is unpatentable. PGR will be performed by the Patent Trial and Appeal Board (PTAB), a new entity within the USPTO that is replacing the Board of Patent Appeals and Interferences (BPAI), and a final decision is supposed to be made within one year. The PGR procedure allows for discovery related to the particular assertions raised in the PGR request and the patentee’s response. The decision made by the PTAB raises “estoppel,” which prevents the party requesting the review from raising arguments that were relied on or could reasonably have been relied on during the PGR proceeding. Thus, while defendants may still raise invalidity and other defenses in subsequent litigation, those defenses cannot be the same as those that were—or could or should have been—raised in PGR. IPR complements PGR, as it becomes available nine months after a patent’s issue date. IPR also may be requested following the termination of a prior PGR, but would have to raise new grounds that were not and could not have been raised in PGR. The scope of discovery is broader with IPR, particularly as it allows the deposition of witnesses who have submitted affidavits (much like present interference proceedings). Other differences with PGR include a threshold determination by the USPTO that the requesting party demonstrate “a reasonable likelihood of prevailing” and grounds for invalidation that are limited to prior art consisting of patents and printed publications, and therefore do not include scope and enablement. As with present-day re-examination procedures, PGR and IPR often will be utilized when a party is faced with threatened or actual litigation. Since PGR must be requested within nine months of a patent grant date, the procedure likely will be used preemptively more often than after litigation has started. In contrast, because IPR can be requested at any time after the close of the PGR request period or the termination of a PGR procedure, IPR likely will be used more often by defendants in patent litigation. IPR must, however, be filed within one year of the patent infringement complaint being served and before any declaratory judgment action is filed by the requestor. Recently, the USPTO has proposed rules to implement both PGR and IPR. Most notable among the rules is the cost. Unlike the European oppositions, where the cost is nominal, the cost of filing both PGR and IPR is significant and based on the number of claims challenged. The basic filing fees for PGR and IPR are $35,800 and $27,200, respectively. These fees, however, can escalate by tens of thousands of dollars in cases where many claims are challenged. While this cost is substantial, it is certainly much less than typical patent litigation costs, so it still may be a bargain in many cases. Nonetheless, cost likely will reduce the number of trivial or pro forma PGRs filed, which has been a shortcoming of European oppositions. The USPTO continues to collect feedback on the proposed PGR and IPR rules, which should be finalized soon.

1 PGR will not be available on patents filed before March 16, 2013, except for some business method patents. As patent applications filed after that date will take some time before they grant, it is likely that few, if any, PGRs will be filed before 2014. IPR, in contrast, will become available on September 16, 2012. Aggressive Healthcare Fraud Enforcement Likely to Continue in 2012 By David Hoffmeister, Partner (Palo Alto), Lee-Anne Mulholland, Associate (Palo Alto), and Nema Milaninia, Associate (New York) On February 14, 2012, Attorney General Eric Holder and Department of Health and Human Services (HHS) Secretary Kathleen Sebelius released a report on the government’s healthcare fraud prevention and enforcement efforts. The report showed that the federal government recovered nearly $4.1 billion in fiscal year (FY) 2011 as a result of these efforts—the highest amount ever recovered in a single year. With healthcare fraud enforcement proving to be a cash cow for a cash-strapped government, we can only expect increased criminal and civil enforcement of healthcare-related offenses.

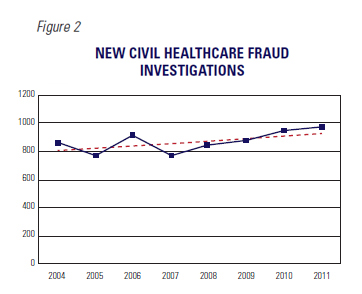

The uptick in enforcement was not limited to criminal cases. As depicted in Figure 2, the Department of Justice’s (DOJ’s) Civil Division in 2009 and 2010 reported (then-record-breaking) highs of 942 and 886 new investigations, respectively. 2011 saw an all-time high of 977 new civil investigations. During this period, the HHS’s Office of Inspector General (OIG) also excluded 2,662 individuals and entities from participating in Medicare and Medicaid programs. These trends are destined to continue: Statements by DOJ and HHS representatives make it clear that the Health Care Fraud Prevention & Enforcement Action Team (HEAT), announced by Attorney General Holder and Secretary Sebelius in May 2009, is getting the resources and attention needed to aggressively investigate and enforce federal healthcare laws. In addition, the Health Care Fraud and Abuse Control Program Report shows the likelihood of a record-breaking number of convictions and penalties going forward. In FY 2011, the DOJ opened 1,110 new criminal healthcare fraud investigations involving 2,561 potential defendants. The DOJ currently has 1,873 criminal healthcare fraud investigations pending that involve 3,118 potential defendants. With 1,069 investigations currently pending, the civil enforcement trend is also up.

As pharmaceutical and medical device companies have increased their international business, the government has used the Foreign Corrupt Practices Act (FCPA) to penalize bribery on the international stage. The FCPA prohibits offers or payments to “foreign officials” (which the DOJ interprets as broadly defined and could include physicians who work for state-owned or partially state-owned entities) for the purpose of securing an improper advantage or to obtain or retain business. The FCPA is enforced criminally by the DOJ and civilly by the U.S. Securities and Exchange Commission. FCPA violations can subject companies to both criminal and civil penalties, including large fines, disgorgement of associated profits, onerous reporting requirements, and federal monitors. Multiple public and private companies already have been targets of the government’s focus on anti-kickback and anti-bribery enforcement, facing hefty fines, significant disgorgement, and the government’s routine use of five-year corporate integrity agreements that include the appointment of an independent review organization. (Please click here for a summary of recent kickback and bribery settlements with medical device and pharmaceutical companies.) This focus on anti-kickback and anti-bribery enforcement actions is set to

increase in 2012, with at least 19 other life sciences companies currently reporting ongoing investigations, including AstraZeneca, Bausch & Lomb, Bristol-Meyers Squibb Company, Eli Lilly and Company, GlaxoSmithKline, Merck & Co., and Pfizer. In light of the government’s aggressive efforts, companies should ensure that they have a properly designed and enforced compliance program that includes, among other things: (1) standards and procedures to prevent and detect unlawful conduct; (2) a person who has actual responsibility for ensuring that prohibited payments are not made; (3) oversight by the company’s governing authority; (4) reasonable efforts to exclude individuals engaged in illegal or unethical conduct from positions of substantial authority; (5) reasonable steps to communicate the company’s standards and procedures to its employees; (6) reasonable steps to ensure that the compliance and ethics program is followed; (7) promotion of the compliance and ethics program consistently throughout the company; and (8) reasonable steps to respond appropriately after unlawful or unethical conduct has been detected. Without taking the proper measures to develop and bolster compliance policies and procedures, companies risk facing the wrath of increasingly aggressive government enforcement in 2012.

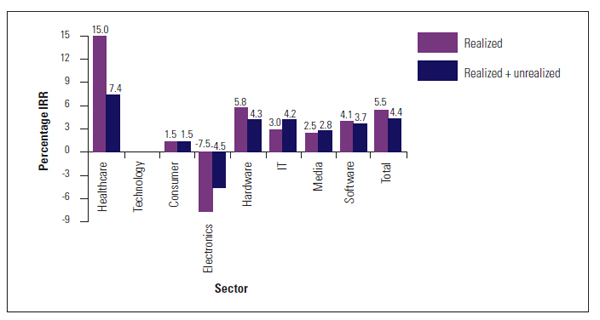

Life Sciences: The Rodney Dangerfield of Venture Capital By Bruce Booth, Partner, Atlas Venture, and Bijan Salehizadeh, Managing Director, NaviMed Capital Most venture capitalists think that IT and Internet investments have been the best source of top venture returns—which is why, in the past few years, unprecedented amounts of capital have poured into Facebook, LinkedIn, Twitter, Zynga, and the like. They may be correct now and in the future—especially with the recent IPOs of several of these companies—but at least over the past decade, they’ve been wrong. In the 2000s, venture capital investments in healthcare and life sciences outperformed venture investments in tech. The venture business is now 12 years into a slump in returns that has discouraged even the most enthusiastic investors and limited partners in the space. Indeed, a look at the data shows that even the top quartile of venture capital firms in aggregate have not returned more than 100 percent of invested limited partner capital since the 1998 vintage. Yet over the past two years, hope has sprung eternal among IT and Internet venture investors, driven largely by a daily barrage of blog and news headlines covering the exponential growth and dramatic returns prospects of a small handful of social-networking and gaming companies. The growth among this small handful of companies is indeed spectacular. Left behind by this good news is the life sciences and healthcare venture capital industry, which, according to PwC MoneyTree/NVCA data, accounted for nearly 30 percent of the $28 billion invested in venture-backed companies in 2011. Widely held notions among GPs, LPs, and entrepreneurs are that life sciences and healthcare venture investments are too challenging, that they have underperformed relative to IT and Internet investments over the past decade, and that they only will continue to do so. Nothing could be further from the truth. It seems that, like Rodney Dangerfield, healthcare venture gets no respect. As outlined in a paper in the July 2011 issue of Nature Biotechnology, healthcare venture investments dramatically outperformed IT venture investments over the past decade. Our study is likely the first widely published, peer-reviewed look at the actual venture returns data for the 2000s comparing tech and life science performance, which we took from the NVCA Benchmarking Database powered by Cambridge Associates. This is the most robust database of its kind, covering returns from nearly 1,300 firms over the past 30 years of venture capital investing. To focus our analysis on actual returns, we primarily looked at companies that achieved first investment and realized an exit in the past decade. Importantly, we looked at the aggregate of individual investments rather than funds, since sector-specific and diversified venture funds exist. Our analysis yielded thousands of data points and unearthed two critically important factors that are widely misunderstood or unknown by the VC ecosystem: the limited partners in the asset class and the media that covers it. 1. Life Sciences Realized Returns (IRR) Dramatically Outperformed IT Overall, life sciences/healthcare venture realized a gross pooled mean IRR of 15.0 percent for the past decade. This is in contrast to 5.5 percent for all venture capital, 3.0 percent for IT, and 4.1 percent for software. In fact, every single subcategory of healthcare venture showed at least 2x-to-3x better realized IRRs than its IT counterparts. Including unrealized exits (or the value of currently active deals) makes the difference less profound, but healthcare’s outperformance of IT still persists. (Definitions: “Realized” deals are actual exits, “pooled” data is the aggregate of the full decade into one data set, “means” are arithmetic means, and “gross” returns are not net of the fees or incentive compensation.)

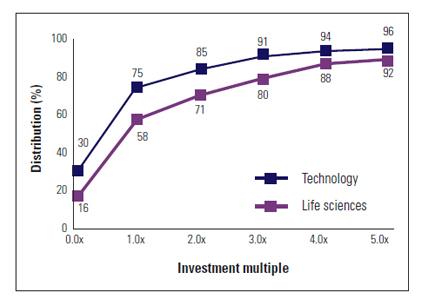

2. Life Sciences Had a Lower Loss Rate and Higher Frequency of 5x+ Returns There’s a perception that many healthcare venture deals lose money. It’s true. Fifty-eight percent of healthcare venture deals returned less than their invested capital. But surprisingly, the failure rate for IT companies is much higher. Almost 75 percent of IT-related investments realized a return of 1x or less in the past decade. Furthermore, the frequency of 5x or greater returns is higher in life sciences—8 percent, versus 4 percent for IT. The tech distribution curve surely extends much further out at the top end (reflecting the likely 100x-to-1000x returns of a small handful of companies), but the data set didn’t allow for that analysis (e.g., the top 1 percent of IT deals almost certainly have higher multiples than the top 1 percent of healthcare deals).

But, as one would expect, not all of the news for healthcare is rosy. Life Sciences IPO Performance Is Poor Compared to IT As of mid-2011, nearly 60 percent of life sciences IPOs from the past four years are trading below their issue price versus roughly 30 percent of tech IPOs. Also, post-IPO performance has been dramatically better in IT than it has been in life sciences. IT companies that go public tend to be more mature businesses with revenues and, often, significant earnings; in biotech, most of the companies remain cash-burning for the foreseeable future. This difference in IPO results is important and is a big part of the negative perception of the life sciences sector. IPOs are media darlings, and they help create buzz about specific sectors. In healthcare, we aren’t likely to have that type of buzz anytime soon. This data and analysis do have some shortcomings. For instance, they are based on a look backward over the past decade and do not include the recent 2011 class of tech IPOs, which will surely improve IT returns—perhaps significantly. However, it has been shown by others that the recent web high-flyers mostly are concentrated in the portfolios of a small group of venture firms, so they may have a less profound impact on the overall tech venture landscape.

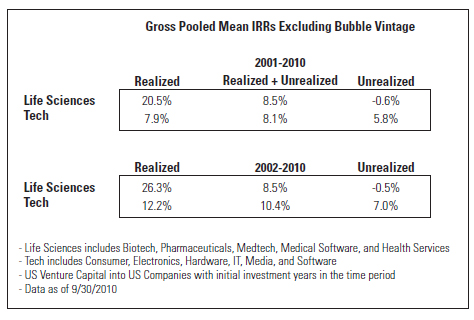

Would the Results Differ if We Excluded Dot-Com Bubble-Era Data? As illustrated in the table to the right, excluding the year 2000 (the year the dot-com-era bubble popped) from our analysis does not change the results with respect to realized exits, which is the best measure of performance. Life sciences and healthcare continue to show a sizable lead over IT, and unrealized returns are equivalent. If one excludes 2001 as well, realized returns continue to favor healthcare and life sciences, but the inclusion of unrealized investments gives a slight edge to IT due to the fact that unrealized healthcare holdings (i.e., current active portfolio companies) are not valued as highly as unrealized IT holdings. As was outlined in the Nature paper, significant mark-ups from round to round tend not to occur in healthcare companies. Instead, even well-performing healthcare companies tend to be held at or near cost until an exit occurs, leading to punitively low unrealized healthcare IRRs. IT companies that perform well, however, can get large round-to-round mark-ups, which help significantly in driving the value of an unrealized tech portfolio. Why Is This Data Different than Cambridge Associates’ Quarterly Benchmark Data by Sector? First, the quarterly Cambridge Associates data combines realized and unrealized returns; the biggest differences noted in our analysis are in the realized exits. Second, our analysis is for U.S. VC firms’ investments in U.S. companies. It is believed that Cambridge Associates includes U.S. VC firm investments in all companies (including companies housed outside the U.S.). Adding international investments by U.S. firms, especially recent investments in China, does improve the unrealized and realized venture returns in all sectors, but particularly in tech. Third, and most importantly, by pooling 2000 through 2010, our analysis attempts to eliminate vintage-year anomalies that the quarterly Cambridge data can show when looking at individual vintage years. This pooling clearly weights the analysis toward years with more financings and away from those years with fewer financings. With these realized returns relative to technology venture capital, why has such a negative perception of healthcare VC emerged in the past few years? We think that there are several reasons: 1. Complexity: Healthcare and biotech in particular are inherently complex sectors, and investing in venture-stage companies in this space requires a blend of deep science and medical understanding, plus a strong stomach to withstand the ups and downs of product development. It’s not revenues and margins, but long-term value creation. And it’s only getting more complex—headlines around tightening regulations at the FDA, the impact of healthcare reform, and reimbursement cuts at Medicare can be scary if not put in proper context. 2. It’s the cycle, stupid: Ten to twelve years ago during a prior IT bubble period, there was a lot of talk about how lackluster an investment area healthcare was relative to IT. In fact, several high-profile firms ditched their healthcare practices during that time. Much of that talk seems to have made a comeback in recent months, driven by the perception that healthcare is a laggard, and multiple firms have shuttered or scaled back their healthcare investing efforts. It’s déjà vu. 3. No 100x’ers: Unlike the IT sector, in which 100x returns are possible and have driven great outcomes in companies like Skype and Google, life sciences never will have these wild “Black Swan” outliers. These 100x’ers are the companies that draw press attention, new talent, and more capital into the IT space. 4. It takes money to get to an answer: Healthcare companies usually require more money to get to an answer than IT (and particularly Internet) companies. The dogma in IT VC these days is that funding lean start-ups is the right way to go. Despite exciting new efforts by a few firms to build asset-light bio-pharma companies, it will never be as capital-efficient to develop a drug, a diagnostic, or a new medical device as it is to build a mobile app or a web service. 5. Poor marketing: Our IT brethren are much savvier marketers, in terms of promoting their new investments and getting glowing pieces about their latest and greatest new investments into mainstream media. This is not the case in healthcare, where only a small handful of VCs and an even smaller group of CEOs use social media or leverage the press effectively. And, of course, most healthcare and life sciences companies don’t translate as well in widely read press outlets such as Forbes or TechCrunch. In conclusion, we think that IT and life sciences venture investing are fundamentally different businesses. However, these sectors actually complement each other quite well within a single venture firm or limited partner portfolio, providing much-needed diversification within the asset class. IT venture investing is all about the hunt for the Black Swan: It’s about getting a high market share of top-quality deal flow and working with only the best syndicates. Placing many small, seed-stage bets creates optionality and allows firms to double-down on those achieving real scalability and market traction. Step-ups in valuation between rounds occur with regular frequency in winning companies, and the tantalizing possibility of a 100x return in a short period of time is always there when you invest in an early-stage company. Healthcare, on the other hand, has been a steadier business, with a lower failure rate and a higher frequency of 5x+ returns. Because of the nature of the healthcare venture market and the capital intensity in biotech, differential venture performance is not really about the market share of new deal flow, as most syndicate formation isn’t competitive. It’s about thoughtful scientific and clinical risk assessment, coupled with disciplined titration of capital and active governance, and can lead to very attractive investments over time. *This article originally was co-written as a blog post by Bruce Booth and Bijan Salehizadeh, who co-authored an article in the July 2011 issue of Nature Biotechnology detailing the differences in returns between life sciences and IT investing. Portions of the original post have been modified for clarity. Bruce Booth is a partner in the life sciences group at Atlas Venture and focuses on novel biopharmaceutical products, therapeutic platforms, and biomedical technologies. He helped build the Pharma R&D practice at McKinsey after studying HIV as a Marshall Scholar. Bruce blogs at www.LifeSciVC.com. Bijan Salehizadeh is a managing director at NaviMed Capital and focuses on investments in commercial-stage companies in health services, healthcare IT, and medical products and technologies. Prior to co-founding NaviMed, Bijan had several years of operating and clinical experience in healthcare. Bijan blogs at www.thebij.com. Life Sciences Venture Financings for WSGR Clients By Scott Murano, Partner (Palo Alto) The table below includes data from 2011 life sciences transactions in which Wilson Sonsini Goodrich & Rosati clients participated. Specifically, the table compares—by industry segment—the number of closings, the total amount raised, and the average amount raised per closing across the first and second halves of 2011.

The data generally demonstrates that venture financing activity declined marginally during the second half of 2011 compared to the first half. Specifically, the total number of financings completed across all industry segments during the second half of 2011 decreased by approximately 2.8 percent compared to the first half, from 108 closings to 105 closings. More significantly, the total amount of money raised across all industry segments during the second half of 2011 decreased by more than 6.2 percent compared to the first half. The medical device industry segment, which represented more than 65 percent of all life sciences closings in 2011, suffered the only decline in total amount raised during the second half of 2011 compared to the first, decreasing by approximately 36 percent, from $571.96 million to $363.5 million. Other industry segments showed strong gains in financing activity during the second half of 2011, including biopharmaceuticals, which represented more than 15 percent of all life sciences closings in 2011, and diagnostics, which represented more than 9 percent of all life sciences closings in 2011. The total amount raised by biopharmaceutical companies during the second half of 2011 increased by approximately 60 percent over the first half, from $147.14 million to $235.91 million, while the total amount raised by diagnostics companies increased by 118 percent, from $27.11 million to $59.36 million. In conclusion, the data indicates that overall access to venture capital for life sciences companies declined somewhat in the second half of 2011 in relation to the first half. The medical device industry segment suffered the only loss in terms of total amount raised by a life sciences industry segment, while other industry segments—notably biopharmaceuticals and diagnostics—realized gains. Although the fundraising environment remains difficult for all companies, life sciences companies should take comfort in the fact that our data indicates that life sciences remained the most attractive industry for investment during both halves of 2011. During the first half of the year, the life sciences industry represented 27.9 percent of closings across all industries, followed by the software industry at 19.2 percent and clean technology and renewable energy at 11.7 percent. Similarly, during the second half of the year, the life sciences sector represented 25.2 percent of closings across all industries, followed by the software industry at 23.9 percent and clean technology and renewable energy at 11.2 percent.

Government Funding for Large and Small MedTech Companies By William S. Baron, Ph.D. The government’s research and development budget is accessible to medical technology companies at all stages of development. Federal support for research and development is available through a variety of funding mechanisms that are used by a wide range of federal agencies, each with their own mission. The below update provides a brief review of select federal funding mechanisms that are available to “small businesses” and companies that are not eligible for “small business” status, including major corporations and start-up companies that are majority owned by venture capital, hedge fund, or private equity firms. Grants versus Contracts Broadly speaking, government funding is awarded via either contracts or grants. A fundamental difference between the two mechanisms is who initially defines the project—the government or the business. Companies considering contracts should determine how their research and development goals align with government solicitation topics, since contracts generally call for a highly focused, product-oriented project. Grants, on the other hand, typically are defined by the investigator via the grant application. Because the company is initiating the project definition, grant projects are easily aligned with a company’s business and technology objectives. To optimize multiple award funding opportunities, care is needed in defining the scope of each application. Companies should submit grant applications having non-overlapping project goals in order to qualify for multiple awards. All federal agencies use both grant and contract funding mechanisms, but the emphasis varies substantially among agencies. The National Institutes of Health (NIH) uses both grants and contracts, with an emphasis on grants, while the Department of Defense (DOD) emphasizes contracts, even when funding investigator-initiated projects. The federal government has been working to aggregate its grant and contract solicitations into a few sites: www.grants.gov for grants, www.fbo.gov for contracts, and www.SBIR.gov for small business grants and contracts. Browsing these sites can yield a quick idea of the breadth of funding opportunities sponsored by various federal agencies. Army Medical Research and Materiel Command The DOD funding mechanism operated by the United States Army Medical Research and Materiel Command (USAMRMC) as described in the DOD’s Broad Agency Announcement for Extramural Medical Research, BAA 12-1, which was released in October 2011, merits special attention by medical technology companies. This solicitation invites investigator-initiated projects that are responsive to a very broad range of immediate medical technology military needs as well as platform technologies to support future breakthroughs. The stage of project development can range from proof-of-concept to field/clinical testing. In fiscal year 2011, awards under this solicitation were capped at $5 million and five years. There is no budgetary cap in the FY 2012 solicitation, although the five-year project period remains. Funding through BAA 12-1 is available to both for-profit organizations other than small businesses as well as small businesses. Non-domestic or non-profit entities also may apply. Research funding for BAA 12-1 is primarily managed through seven programs. The scopes of the individual program missions are defined around: infectious diseases, combat casualty care, operational medicine research, clinical and rehabilitative medicine, medical biological defense, medical chemical defense, and telemedicine and advanced technology. A special projects program oversees projects that fall outside the scope of these seven defined research programs when such projects are relevant to health-related issues for military personnel, military dependents, veterans, and the American public in general. These include projects relating to health care delivery; the detection, diagnosis, control, or eradication of specified diseases, conditions, or syndromes; or the advancement of military medical interests. Pre-proposals for BAA 12-1 are accepted on a revolving basis—i.e., there are no submission deadlines while the solicitation is open. Unless instructed otherwise, organizations are required to explore USAMRMC interest in a specific idea or project by submitting a preliminary research proposal. A pre-proposal of interest to USAMRMC is followed by an invitation to the company to submit a full formal proposal requesting funding. Pre-proposal topics are kept in a database that can be searched by military personnel at later dates, when needs may change USAMRMC’s funding priorities. A major advantage to working with the DOD is that the agency may become a large first customer for the developed product. SBIR/STTR Funding Programs The Small Business Innovation Research (SBIR) and Small Business Technology Transfer Research (STTR) funding mechanisms are attractive due to their structured application processes and multiple awards. Although the legislated award guidelines for the SBIR/STTR programs are $1,150,000 for a base Phase I/II award path, the actual awards, when justified, can be higher. The average NIH funding for a SBIR Phase I/II award path in FY 2011 was nearly $1.6 million. The SBIR/STTR programs were funded in 2009 with approximately $2.5 billion in legislated set-aside monies. Historically, when programs grow, awards and award rates increase. On December 31, 2011, the SBIR/STTR programs were reauthorized for an additional six years. In the coming months, the funding agencies are expected to issue guidelines implementing the provisions of the new legislation. The new legislation includes higher award amounts, larger set-asides, and provisions for funding companies that are majority owned by venture capital, hedge fund, or private equity firms. The NIH issued nearly $700 million worth of SBIR/STTR awards in FY 2010, almost exclusively for medical technology. The DOD paid out roughly $1.24 billion in SBIR/STTR awards in 2009, sponsored by various DOD components: the Department of the Army, the Department of the Navy, the Department of the Air Force, the Defense Advanced Research Projects Agency, the Defense Threat Reduction Agency, the Missile Defense Agency, the National Geospatial-Intelligence Agency, and the Office of the Secretary of Defense; many of the awards were for medical technology projects. Other agencies funding medical-technology-related projects include the National Science Foundation (NSF), the Department of Energy (DOE), the Department of Transportation (DOT), and the United States Department of Agriculture (USDA). In summary, federal funding for medical technology research and development is alive and well, with attractive portals available to all companies, regardless of their investor portfolio. William Baron has been helping companies raise government funding for over 20 years and can be reached at Vision Metrics, Inc., in Menlo Park, California, at (650) 328-8149 or wsbaron@pacbell.net. Recent Life Sciences Highlights Par Pharmaceutical, Generic Drug Makers Obtain Federal Circuit Victory Heartflow Raises $75 Million in Series C Funding Round Acutus Medical Raises $5.4 Million in Series A Financing Extend Health Files for Proposed IPO Intellikine to Be Acquired by Takeda ForteBio Announces Acquisition by Pall Corporation HMS Holdings to Acquire HealthDataInsights for $400 Million Mylan Announces Settlement Agreement for its Generic Version of Vivelle-Dot Alchemia Completes $15 Million Placement of New Shares

Wilson Sonsini Goodrich & Rosati’s Medical Device Conference Wilson Sonsini Goodrich & Rosati’s 20th annual Medical Device Conference, aimed at professionals in the medical device industry, will feature a series of panels and discussions addressing the critical business issues facing the industry today. rEVOLUTION Symposium rEVOLUTION 2012 will mark the seventh annual symposium for chief scientific officers focused on drug R&D issues. The event will examine the organization and management of R&D to uncover new models to accelerate the discovery and development of new drugs. Phoenix 2012: The Medical Device and Diagnostic Conference for CEOs Phoenix 2012 will serve as the 19th annual conference for chief executive officers and senior leadership of medical device and diagnostic companies. The conference will provide an opportunity for top-level executives from large healthcare and small venture-backed companies to discuss financing, strategic alliances, and other industry issues.

Click here for a printable version of The Life Sciences Report This communication is provided for your information only and is not intended to © 2012 Wilson Sonsini Goodrich & Rosati, Professional Corporation |

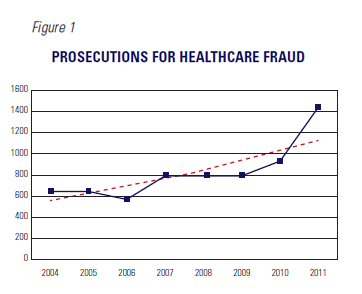

The government’s Health Care Fraud and Abuse Control Program Report showed not only record revenues from enforcement, but also a record volume of enforcement. As reflected in Figure 1, the number of companies and individuals charged with fraud-related healthcare crimes in 2011 reached an all-time high of 1,430. This historic high was significantly more than in prior years.

The government’s Health Care Fraud and Abuse Control Program Report showed not only record revenues from enforcement, but also a record volume of enforcement. As reflected in Figure 1, the number of companies and individuals charged with fraud-related healthcare crimes in 2011 reached an all-time high of 1,430. This historic high was significantly more than in prior years.  The statistics for 2011 provide a clue as to HEAT’s future focus. In mid-2011, high-level officials from the DOJ and HHS stated publicly that they would be focusing their attention on violations of anti-kickback and anti-bribery laws by medical device and pharmaceutical companies. Those laws in the domestic context primarily include the Anti-Kickback Statute, Civil Monetary Penalties Law, and Stark Law, which provide civil and criminal penalties for remunerations, including bribes and kickbacks, paid to doctors or hospitals in return for referrals or purchases reimbursable under government healthcare programs. These are enforced by the DOJ’s criminal and civil divisions and OIG. Penalties for violations can include large fines and disbarment from participating in federal healthcare programs.

The statistics for 2011 provide a clue as to HEAT’s future focus. In mid-2011, high-level officials from the DOJ and HHS stated publicly that they would be focusing their attention on violations of anti-kickback and anti-bribery laws by medical device and pharmaceutical companies. Those laws in the domestic context primarily include the Anti-Kickback Statute, Civil Monetary Penalties Law, and Stark Law, which provide civil and criminal penalties for remunerations, including bribes and kickbacks, paid to doctors or hospitals in return for referrals or purchases reimbursable under government healthcare programs. These are enforced by the DOJ’s criminal and civil divisions and OIG. Penalties for violations can include large fines and disbarment from participating in federal healthcare programs.

We would bet that only a small percentage of GPs and LPs in venture capital actually are aware of healthcare’s outperformance of IT in the past decade, and we think that greater transparency around the actual returns data in the venture industry is a good thing.

We would bet that only a small percentage of GPs and LPs in venture capital actually are aware of healthcare’s outperformance of IT in the past decade, and we think that greater transparency around the actual returns data in the venture industry is a good thing. Some questions arise from an examination of this data:

Some questions arise from an examination of this data: