Spring 2011 New Pressures on the Pharma and Medical Device Industry Highlight the Importance of Compliance Programs By Leo P. Cunningham, Partner, and Lee-Anne Mulholland, Associate (Palo Alto Office) You get the behavior you incentivize. That is why bribes work—and are illegal. And that is why the government offers financial incentives—bribes of its own—for “whistleblowers” who report misconduct. Pharmaceutical and medical device companies have traditionally focused their compliance efforts on federal healthcare laws, such as the anti-kickback statutes and regulations from the Food and Drug Administration and U.S. Department of Health and Human Services. The qui tam provisions of the False Claims Act have created an effective incentive for reporting violations by healthcare companies. But there are other anti-corruption laws out there and other incentives for reporting violations. Healthcare companies should ensure that their compliance efforts factor in all relevant anti-corruption laws and provide their own incentives for internal reporting of potential violations. Domestic anti-kickback laws provide criminal penalties for remunerations, including bribes and kickbacks, paid to doctors or hospitals in return for referrals or purchases reimbursable under government healthcare programs. But companies doing business abroad must also be wary of the Foreign Corrupt Practices Act (FCPA), which prohibits offers or payments to “foreign officials” for the purpose of securing an improper advantage to obtain or retain business. The U.S. government takes the view that doctors practicing in countries with government-subsidized medical care are “foreign officials.” The FCPA also requires public companies to maintain accurate books and records and to devise and maintain an adequate system of internal accounting controls to prevent improper payments. FCPA violations are pursued as criminal matters by the Department of Justice (DOJ) and civil matters by the Securities and Exchange Commission (SEC). Healthcare companies that manufacture, sell, market, import, or export their products abroad must have compliance programs that address the risk of FCPA violations to avoid the harsh penalties that result from them.

Companies doing business abroad have the additional risk of running afoul of foreign anti-corruption laws. The United Kingdom’s Anti-Bribery Act, for instance, goes beyond the FCPA and includes a new strict liability offense for companies that fail to prevent bribery by an employee, agent, or subsidiary. The U.K. law, however, offers a safe harbor for those companies that try to prevent bribery with an effective compliance program. In fact, corrupting payments by U.S. companies to anyone run the risk of violating laws against commercial bribery. Payments that may not violate the technical requirements of the Anti-Kickback Act or FCPA can still violate one of the more general anti-bribery provisions. Most states have laws forbidding commercial bribery, and the general federal anti-fraud statutes have long been used by federal prosecutors to pursue all manner of bribes and kickbacks, whether or not a foreign official or a federal reimbursement program is involved.

While healthcare companies have traditionally focused on qui tam actions, with the enactment of the Dodd-Frank Wall Street Reform and Consumer Protection Act, individuals who assist the SEC in uncovering securities violations, including violations of the FCPA, can receive a payoff of 10 to 30 percent of the fines collected. Given that FCPA-related penalties exceeded $1.8 billion in 2010, the financial incentive for whistleblowers to report FCPA violations to the government is enormous. Healthcare companies have already faced aggressive enforcement of domestic anti-corruption laws. In 2010 alone, the government obtained over $4 billion in penalties from healthcare companies. The increased risk of enforcement under the FCPA and other anti-corruption laws here and abroad, particularly in light of the additional whistleblower incentives under Dodd-Frank, underscores the need to prevent violations before they occur. That means having an effective compliance program. Consider the following improvements to your compliance program if you have not already:

In the current regulatory environment, improving your compliance programs could be an excellent investment.

Marketing Dos and Donts:

What Senior Management of Commercial-Stage Life Sciences Companies Need to Know about Interactions with Healthcare Professionals

By David Hoffmeister, Partner, Farah Gerdes, Associate, Kristen Harrer, Associate, and Jon Nygaard, Attorney (Palo Alto Office) As state and federal governments cover more and more individuals under their various healthcare programs, there is an ever-increasing scrutiny by government prosecutors of payments and compensation arrangements between healthcare professionals (and their institutions) and medical device and pharmaceutical companies. This increased scrutiny is reflected in recent legislation as well as increased enforcement of broad anti-fraud laws, such as the Federal Anti-Kickback Statute and Civil False Claims Act, that has resulted in highly publicized settlements by device and pharmaceutical companies that collectively amount to billions of dollars. Some of the largest settlements involving medical device companies include agreements entered into in 2007 between the federal government and five orthopedic device manufacturers to resolve allegations that the companies paid illegal kickbacks to physicians as inducements for physicians to use their devices. Four of the five manufacturers—Biomet Orthopedics, Inc., DePuy Orthopedics, Zimmer Inc., and Smith & Nephew—collectively agreed to pay the government $311 million to settle the cases. All five manufacturers, including Stryker Orthopedics, also agreed to certain financial disclosure requirements concerning their financial relationship with physicians. In announcing the settlements, the government stated in its press release: “Patients in federal health care programs deserve the best available treatment from physicians and surgeons without the corrupting influence of kickbacks from the medical device companies. We will continue to work closely with our law enforcement partners to vigilantly investigate schemes meant to defraud Medicare, and to prosecute those individuals to the fullest extent of the law.” While many of the more prominent fraud and abuse settlements have involved large-cap, public companies, small device and pharmaceutical companies should not consider themselves immune from investigation and prosecution by virtue of their size. The following are three examples of recent settlements involving smaller public medical device companies:

Not only was each of these cases settled for millions of dollars, each company also likely incurred millions in defense costs, as well as significant disruptions to its business.

Small, privately held, venture-backed companies that are commercializing products are among the companies receiving government subpoenas, and having their marketing programs and relationships with physicians targeted for possible violations of the Anti-Kickback Statute. Therefore, it is important for senior management, boards of directors, and venture investors who fund private, commercial-stage, life sciences companies to understand the broad prohibitions of the Anti-Kickback Statute and the types of interactions with and payments to healthcare professionals that may trigger a prolonged Office of Inspector General (OIG) investigation. Federal Anti-Kickback Statute The Anti-Kickback Statute makes it illegal for device and pharmaceutical companies to offer or give anything of value to any person or entity to purchase any product or service that is reimbursed by the government (e.g., under or by Medicare/Medicaid). It is also unlawful for the companies’ customers—primarily physicians and healthcare institutions—to either solicit items of value from their vendors or to receive them when they are offered. Thus, the law applies to both the vendor of devices and pharmaceuticals and to their healthcare customers. Several “safe harbors” are contained in the statute’s implementing regulations. However, only those who structure their business arrangements to satisfy all the criteria of a safe harbor will be immune from liability and prosecution. Where a business practice does not qualify for a safe harbor, the OIG, the governmental entity that enforces the statute on the civil side, will examine the practice to determine whether it involves “remuneration” and, if so, whether the arrangement appears to involve the sort of abuse the law was designed to combat. In determining whether to institute enforcement action, the OIG will look at a variety of factors, including the following:

No one factor is dispositive, and given the interpretation of the law to date, the OIG has virtually unlimited discretion in selecting cases for enforcement. Additionally, federal courts and administrative bodies considering the law in the context of actual enforcement cases have established several important interpretive principles, including the following, some of which are now codified in recent healthcare reform legislation.

The DOs and DON’Ts of Interactions with, and Payments to, Healthcare Professionals The following is a quick, non-exhaustive list of DOs and DON’Ts for senior management, board members, and venture investors in private, commercial-stage, life sciences companies with respect to interactions with healthcare professionals. Some of these suggestions are codified in various statutes or regulations on the state or federal level. Others are incorporated in model codes of conduct for interactions with healthcare professionals promulgated by such organizations as AdvaMed and PhRMA. PROHIBITION ON ENTERTAINMENT AND RECREATION

MODEST MEALS

GIFTS

EVALUATION PRODUCTS

SALES, PROMOTIONAL, AND OTHER BUSINESS MEETINGS

GRANTS AND CHARITABLE DONATIONS

CONSULTING ARRANGEMENTS

COMPANY-SPONSORED TRAINING AND EDUCATION MEETINGS

EDUCATIONAL CONFERENCES SPONSORED BY ORGANIZATIONS OTHER THAN THE COMPANY

REIMBURSEMENT SUPPORT PROGRAMS

Conclusion Senior management, boards of directors, and investors in private, commercial-stage, venture-backed, life sciences companies must understand that the OIG does not limit its investigative activities to large, publicly traded, life sciences companies. Failure to ensure compliance with current laws and standards for interactions with healthcare professionals can trigger unwanted OIG scrutiny. If you have any questions about these issues, please feel free to contact David Hoffmeister, Farah Gerdes, Kristen Harrer, or Jon Nygaard at Wilson Sonsini Goodrich & Rosati.

Life Science Venture Financings for WSGR Clients By Scott Murano, Associate (Palo Alto Office)

The table below includes data from 2010 life science transactions in which Wilson Sonsini Goodrich & Rosati clients participated. Specifically, the table compares—by industry segment—the number of closings, the total amount raised, and the average amount raised per closing across the first and second halves of 2010.

The data generally demonstrates that venture financing activity declined during the second half of 2010 compared to the first half. Specifically, the total number of financing closings completed across all industry segments during the second half of 2010 decreased by approximately 3.5 percent compared to the first half, from 86 closings to 83 closings. More significantly, the total amount of money raised across all industry segments during the second half of 2010 decreased by more than 29 percent compared to the first half. The biopharmaceuticals and medical device and equipment industry segments, which together represent more than 85 percent of all life science financing closings, suffered the largest declines in average amount raised during the second half of 2010 compared to the first. Biopharmaceutical companies raised approximately 38 percent less money on average in the second half of 2010, while medical device and equipment companies raised approximately 28 percent less money on average.

Other data from our recent transactions suggests that of all financings completed for our life sciences clients in 2010, including equity financings, bridge financings, recapitalizations, and other non-traditional types of financings, the percentage of Series A equity financings remained at 23.3 percent across both the first and second halves of the year; the percentage of Series B equity financings decreased from 15.1 percent in the first half of the year to 13.3 percent in the second half; the percentage of Series C (and later) equity financings decreased from 23.3 percent in the first half to 18.3 percent in the second half; and the percentage of bridge financings decreased from 33.7 percent in the first half to 31.7 percent in the second half.

The decrease in Series B and Series C (and later) equity financings and bridge financings was offset by an increase in the number of recapitalizations and other non-traditional types of financings during the same periods, suggesting that traditional middle-to-later-stage equity financings and bridge financings are in decline—an alarming fact for many middle-to-later-stage companies that require additional capital to achieve regulatory approval or some other value-driving event, which may be critical to securing the next round of financing or a positive liquidity event. The upshot, however, is that later-stage companies that were able to secure equity financing during the second half of 2010 received a higher average pre-money valuation than later-stage companies that secured equity financing during the first half of the year. Recent data from our transactions indicates that the average pre-money valuation of later-stage equity financings increased from $57.1 million in the first half of 2010 to $75 million in the second half. This increase may be explained in part by an increasing presence of less valuation-sensitive, corporate strategic investors, who were the source of 11.5 percent of total venture capital provided to life science companies in the second half of 2010, compared to 3 percent in the first half. On the other hand, our data suggests that the average pre-money valuations for Series A and Series B equity financings dropped from $18.5 million and $44 million, respectively, in the first half of 2010 to $5.9 million and $20 million, respectively, in the second half. That represents a decrease of 68 percent and 54 percent, respectively, and suggests that those early-stage companies that were fortunate enough to raise equity financing during the second half of 2010 endured significantly more dilution, dollar-for-dollar, than similarly situated companies that raised equity financing during the first half of the year. Overall, the data indicates that access to venture capital for life science companies declined in the second half of 2010 compared to the first half, and the fundraising environment remains difficult in early 2011. While it is too early to tell what the remainder of 2011 will hold for life science companies, management and investors may take some comfort in knowing that the sluggishness in venture capital activity is not unique to life science companies, as venture capital activity across all industries slowed down during the second half of 2010 relative to the first half. After all, the percentage of venture capital investments made in life science companies during the second half of 2010 remained unchanged from the first half of the year at approximately 25 percent.

Show Me the Money: The Results of the Therapeutic Discovery Project Tax Credit and Grant Program By Elton Satusky, Partner (Palo Alto Office) Background The Patient Protection and Affordable Care Act1 established a limited-time federal tax credit and grant program designed to reimburse up to 50 percent of eligible R&D expenditures incurred in 2009 and 2010 by small employers for qualifying therapeutic discovery projects (QTDP program). The legislation authorized up to $1 billion in investment tax credits and cash grants through the QTDP program for life sciences companies with no more than 250 employees to help defray the costs of biomedical research. Eligible companies applied for and were selected to receive such credits or grants through a competitive certification process. Selection Criteria The Internal Revenue Service (IRS) required that awards be directed to projects that show reasonable potential to: (1) result in new therapies that either treat new areas of unmet medical need or prevent, detect, or treat chronic or acute diseases or conditions; (2) reduce long-term healthcare costs in the United States; or (3) significantly advance the goal of curing cancer within the next 30 years. Moreover, in selecting award recipients, the IRS took into consideration which projects have the greatest potential to create and sustain (directly or indirectly) high-quality, high-paying jobs in the United States and advance U.S. competitiveness in the fields of life, biological, and medical sciences. In making this determination, the IRS considered to what extent a project would either: (1) produce a new or significantly improved technology, or a new application or significant improvement to existing technology, as compared to commercial technologies currently in service; or (2) lead to the construction or use of a contract production facility in the U.S. in the next five years. For additional details on the QTDP program application process and background, please see the May 24, 2010, WSGR Alert titled “Treasury Department Issues Guidance on Therapeutic Discovery Project Tax Credit and Grant Program for Small Employers,” available at http://www.wsgr.com/wsgr/Display.aspx?SectionName= publications/PDFSearch/wsgralert_irs_notice_2010-45.htm. Show Me the Money The IRS initially estimated that 1,200 companies would submit applications, which, if split evenly, would have resulted in an average award of $0.8 million. The actual number of applicants significantly exceeded this estimate, and far more individual project applications—5,600—were submitted than expected. Without prior guidance, the IRS split the pot equally among all qualified projects, giving out 4,606 awards to 2,923 companies. Although at first blush it would appear that the IRS did not apply the criteria stringently (since 4,606 awards were made out of 5,600 applications, reflecting an 82 percent application success rate), we are aware that applicants went through a selection process, which included in some cases follow-up interviews and questions regarding the substance of the application and the status of the project and the company.

The result of the pot-splitting was an award of $244,479 per project, well short of the expected $0.8 million and the QTDP program’s stated maximum available amount per company of $5 million. That said, there was no limitation placed on the number of projects that a single company was allowed to apply for and many applicants took advantage of this fact. The largest amount of money received by any single company was approximately $3.5 million. Although the IRS’s pre-billing of the QTDP program seemed to focus on a tax credit to help sustain small company research projects, the program also offered cash grants since many qualifying companies would have little taxable income to offset with credits. Of the $1 billion authorized by the program, the overwhelming majority was in the form of cash grants (approximately $19 million, or less than 2 percent, was in the form of tax credits). This is understandable since the QTDP program was designed to provide incentives to smaller, less mature, life science companies that would inherently be in the pre-revenue, R&D stage of their lifecycle. Ultimately, California companies took the largest share of the program’s funds, with more than $281 million. Massachusetts accounted for nearly $127 million, while Maryland, New Jersey, New York, North Carolina, Pennsylvania, Texas, and Washington each received more than $30 million. Wilson Sonsini Goodrich & Rosati Clients

Approximately $100 million of the $1 billion, or 10 percent of the QTDP program’s dollars, was awarded to clients of Wilson Sonsini Goodrich & Rosati (242 companies out of the 2,993 recipients, or 8 percent). And in California, $71 million out of $278 million, or 26 percent, was awarded to our clients. We would like to take this opportunity to congratulate all of our well-deserving client recipients. Conclusion The breadth of the U.S. life sciences industry was evident in the diversity of cash grant and tax credit recipients. Examples include oncology drugs, cardiovascular drugs, Alzheimer drugs, vaccines, stem-cell-based products, implantable products targeting a range of anatomies, drug delivery technologies, molecular diagnostics, imaging tools, catheter-based medical devices to treat a range of diseases, medical equipment, and many more. The $1 billion made available through the QTDP program is equivalent to approximately half of the total investment made by venture capital firms in 234 U.S. medical device companies during the second quarter of 2010—a significant amount of money put into play by the government at a time of economic uncertainty and severe capital-raising challenges. While many recipients were disappointed with the amount received on a per-company basis, we believe that a substantial number of important projects that otherwise struggled to obtain adequate capital in 2010 were given the opportunity to fight another day with the assistance of these additional funds. As a tool to sustain innovation in the United States, the QTDP program may only have played a small role, but given the lack of other available resources for life sciences companies, it may well have been at a critical time.

Medical Technology Innovation Scorecard The Race for Global Leadership By Christopher Wasden, PricewaterhouseCoopers LLP New Dynamic Redefines Medical Technology Innovation The way we assess value in medical technology is changing radically. The old dynamic of the physician as arbiter of value is giving way to a new one: government and private insurers and “self-pay” consumers increasingly determine what sells and at what price. They refuse to pay for incremental innovations that add bells and whistles but do not significantly improve health or reduce cost. The faster, better, smaller, cheaper advances so common in consumer electronics portend the future of medical technology. Emerging-market countries such as China, India, and Brazil, despite comparatively less well-developed healthcare system infrastructures, are quickly taking the lead in developing lean, frugal, and reverse innovation. This type of innovation simplifies devices and processes, retaining essential functions, while applying newer technologies that are more mobile, customized to consumers’ needs, and less costly. The PwC Medical Technology Innovation Scorecard shows that the innovation leaders of today may find their position slipping during the next decade. Three trends are evident:

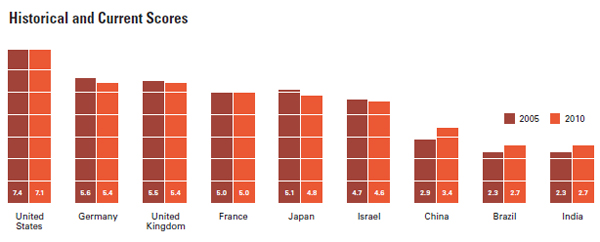

Scorecard Assesses Nine Countries’ Capacity for Innovation The Innovation Scorecard assesses the capacity of nine countries with strong medical technology market potential to adapt to the changing nature of innovation: Brazil, China, France, Germany, India, Israel, Japan, the United Kingdom, and the United States. As well as providing a current view of innovative capacity and capability, the Innovation Scorecard looks at the past five years to gain a historical perspective and projects into the future to present the outlook for 2020.

The Innovation Scorecard combines 86 metrics to calculate the current score and 56 for the historical. These metrics range from objective to subjective and help to identify trends in medical technology innovation. A top-level view of current scores reveals:

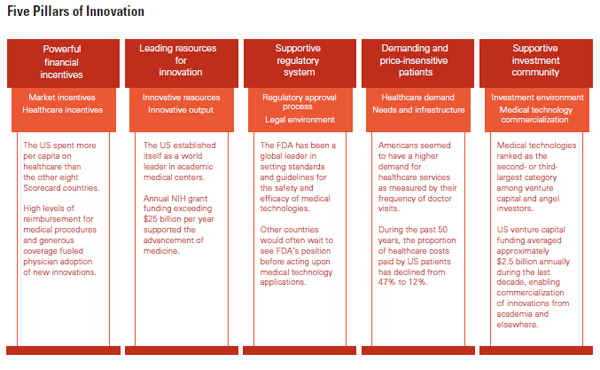

Looking at past scores and the outlook for the future along with current scores changes the perspective and reveals that although the United States will hold its lead, the country will continue to lose ground during the next decade. The Innovation Scorecard also projects declines for Japan, Israel, France, the United Kingdom, and Germany. China, India, and Brazil will experience the strongest gains during the next 10 years. Of the nine countries, China, which has shown the strongest improvement in innovative capacity during the past five years, is expected to continue to outpace other countries and reach near parity with the developed nations of Europe by 2020. The Five Pillars of Medical Technology Innovation During the past 50 years, the United States has provided an ideal innovation ecosystem that has fostered significant advances in medical technology. U.S. dominance of this industry stems from its strength in five innovation pillars, which form a structure for the Innovation Scorecard.

Sources: United Nations Educational, Scientific and Cultural Organization and

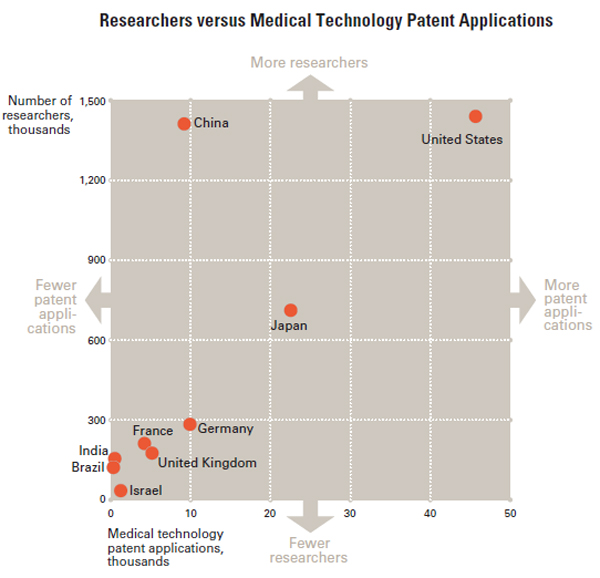

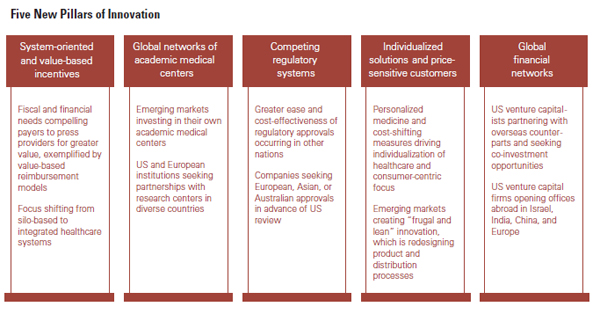

An Example of the Findings China, ranking second in number of research professionals, has nearly as many as the United States and twice the number as Japan. Yet China has not been as productive in obtaining medical technology patents. The United States obtains more patent applications, averaging more than 44,000 per year, but Israel and Japan lead in filing medical technology patent applications on a per capita basis. If China were as productive as the other countries, it could produce the second-largest number of medical technology patents in the world. Who Will Take the Lead in 2020? To develop the type of medical technology ecosystem required for 2020, countries and companies will have to adapt to five new pillars of innovation:

Although the United States should maintain its lead in medical technology innovation for years to come, long-term U.S. dominance is no longer assured. The supportive ecosystem that fostered this dominance creates inherent limits to change, encourages an incremental and less radical path to innovation, and discourages innovations that could transform healthcare’s cost structure and deliver greater value. Radical innovations that have a greater chance to bend the cost curve are more likely to emerge from developing countries such as China, India, and Brazil. View the full report at www.pwc.com/InnovationScorecard. About PwC’s Pharmaceuticals, Medical Device and Life Sciences Industry Group:

Saints Capital Publishes Guide to Secondary Transactions By Michael Coke, Associate (Palo Alto Office) The sale of private company shares on the secondary market is becoming increasingly prevalent as the timeline to reach a liquidity event has lengthened over the last decade. In order to proactively manage secondary transactions, the boards, management teams, and investors of these companies need to be aware of the relevant issues, challenges, and considerations. Unlike public markets, where information-disclosure rules are well established, rights and privileges of existing investors are limited, and securities laws are well defined, the world of secondary share sales in private companies is much less understood. Saints Capital, with contributions from Wilson Sonsini Goodrich & Rosati, has published A Guide to Secondary Transactions: Alternative Paths to Liquidity in Private Companies. Saints Capital has been an industry leader in secondary transactions for over 10 years, and during that period the organization has been approached numerous times with questions about the rationale, process, legal implications, and operational consequences of a secondary transaction. Wilson Sonsini Goodrich & Rosati is pleased to represent Saints Capital in connection with a number

of transactions.

Some of the other topics that are covered in A Guide to Secondary Transactions include the following:

Please visit http://www.saintsvc.com/from.html to view A Guide to Secondary Transactions: Alternative Paths to Liquidity in Private Companies. About Saints Capital: Saints Capital is a leading direct secondary acquirer of venture capital and private equity investments in emerging growth companies around the globe. Saints Capital also makes traditional direct venture capital investments on a primary basis and in special situations in technology, healthcare, consumer, and industrial companies in the United States. Founded in 2000, Saints provides liquidity for private investors in such markets as investment and commercial banks, buyouts, corporate venture capital, and hedge funds. Saints has more than $1 billion of committed capital under management, over 50 completed portfolio transactions, and investments in more than 200 companies. More information about Saints Capital can be found on its website at http://www.saintsvc.com/.

Recent Life Sciences Highlights Gilead Sciences to Acquire Calistoga Pharmaceuticals for $375 Million Boston Scientific Enters into Agreement to Acquire ReVascular Therapeutics Fluidigm Prices Initial Public Offering of Common Stock Endocyte Announces Pricing of Initial Public Offering Medtronic Completes Acquisition of Ardian Teleflex Acquires VasoNova PneumRx Raises $33 Million in Capital iCAD Completes Acquisition of Xoft Lpath Grants Pfizer Exclusive Option for Worldwide License for iSONEP Affymetrix Defeats Patent Infringement Suit Cephalon and Mesoblast Enter Strategic Alliance to Commercialize Therapeutic Products for Regenerative Medicine Pacific Biosciences Announces Pricing of Initial Public Offering of Common Stock VIVUS Announces Sale of MUSE Assets to Meda Amyris Announces Pricing of IPO

Wilson Sonsini Goodrich & Rosati’s Medical Device Conference Wilson Sonsini Goodrich & Rosati’s 19th annual Medical Device Conference, aimed at professionals in the medical device industry, will feature a series of panels and discussions addressing the critical business issues facing the industry today. *Please note the new venue for this year’s event. Phoenix 2011: The Medical Device and Diagnostic Conference for CEOs Phoenix 2011 will mark the 18th annual conference for chief executive officers and senior leadership of medical device and diagnostic companies. The event will provide an opportunity for top-level executives from large healthcare and small venture-backed companies to discuss financing, strategic alliances, and other industry issues.

Click here for a printable version of The Life Sciences Report This communication is provided for your information only and is not intended to © 2011 Wilson Sonsini Goodrich & Rosati, Professional Corporation |