|

First-Mover Advantage: The Case for Investing in Life Science

By Jonathan Norris, Managing Director, Silicon Valley Bank

There has been extensive discussion about tough times in life science venture investing and the impending decrease in the number of venture firms. While we agree that the number of venture funds and the overall amount of capital deployed must decrease over the next few years, we remain very upbeat about the prospects of lucrative returns in life science venture from investors who have fresh capital to deploy.

In the last three years, we have observed significant value creation in life science venture-backed M&A. In 2011, both the number and total value of “Big Exits” (defined as private, venture-backed exits with upfront of at least $50 million in device and $75 million in biotech) reached seven-year highs. We believe the life science venture industry is in a position to continue this up cycle. Those funds with first-mover advantage—funds deploying fresh capital now and over the next few years—are best suited to exploit the upward swing. The time to invest is now, as favorable trends have developed enough to demonstrate the ability to achieve significant outsized returns. In this article we will explore the current trends that make the life science sector an attractive place for investment.

Background: Disconnect Between Capital Deployed and Raised Will Lead to a Reduction in Life Science Venture Investment

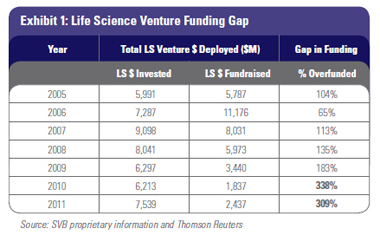

While many experts have commented on the downward trend in life science investing, the amount of capital invested into venture-backed life science companies has actually been fairly constant between $6 and $8 billion since 2005.1 Life science investment as a percentage of all venture investment has also been consistent, averaging 27 percent of all venture investment over the last five years.2 However, life science venture fundraising is at odds with life science dollars invested, which has outpaced fundraising in every year since 2007 (Exhibit 1).

The chart below includes all venture life science funds by vintage year, as well as all multi-focused funds’ allotment to life science per our best educated guess.

In total, since 2005, there has been a 25 percent gap in life science venture dollars raised versus life science venture dollars invested. For the last two years (2010-2011) the ratio has been more than 3:1 in dollars deployed versus dollars raised. Even with corporate venture and non-venture equity funding filling some of the gap, the current trend of $6 billion-plus per year invested into life science companies cannot continue. The last $6 billion-plus fundraising year was 2007—and that vintage year is at or near the end of its active new investment cycle and close to fully invested. Since 2009, fundraising has averaged only $2.6 billion per year. That trend will continue, and we believe that life science funds will raise between $2.5 and $3.5 billion per year going forward. A smaller percentage of high-performing funds will be able to fundraise, many of them at smaller dollar amounts than previous funds. With less capital to invest in the market, life science dollars deployed will also come down, likely reduced to the $4-5 billion range. In total, since 2005, there has been a 25 percent gap in life science venture dollars raised versus life science venture dollars invested. For the last two years (2010-2011) the ratio has been more than 3:1 in dollars deployed versus dollars raised. Even with corporate venture and non-venture equity funding filling some of the gap, the current trend of $6 billion-plus per year invested into life science companies cannot continue. The last $6 billion-plus fundraising year was 2007—and that vintage year is at or near the end of its active new investment cycle and close to fully invested. Since 2009, fundraising has averaged only $2.6 billion per year. That trend will continue, and we believe that life science funds will raise between $2.5 and $3.5 billion per year going forward. A smaller percentage of high-performing funds will be able to fundraise, many of them at smaller dollar amounts than previous funds. With less capital to invest in the market, life science dollars deployed will also come down, likely reduced to the $4-5 billion range.

These downward trends enable firms that have fresh capital to invest to achieve significant returns in this sector. In the following section we will detail the trends that position life science venture as an attractive investment area.

Why Life Science Is an Attractive Place to Deploy Capital (Both for VCs and LPs)

1.) Self-Selection of Proven Funds (or Investors)

Fundraising in the life science sector is difficult. In order to attract attention and LP dollars, venture funds need to show substantial distributions back to LPs. In this investment cycle, distributions that garner LP interest and their commitments for the next fund are typically shown in two different ways: 1) a very high distribution to paid in capital (DPI) percentage in a firm’s most recent fund (busting through the J-curve), or 2) substantial distributions across multiple funds demonstrating that the investment thesis over time is now yielding results. Either way, the funds that will be successful raising money in this environment will need to show a solid track record for achieving exits and distributing money back to investors. As these firms raise their next funds and others do not, the new subset of active life science venture funds will be high-quality, proven exit makers. These investors will form highly competent syndicates that know how to create value in this environment and form companies that will compete against a smaller number of venture-backed competitors in their space.

Our Big Exit data supports that notion of a concentrated group of life science venture firms responsible for an outsized portion of Big Exits. If we examine the 170 Big Exits in biotech and device since 2005, the top 10 life science venture funds measured by number of Big Exits were responsible for 52 percent of all Big Exits. If we expand that to the top 20 life science venture firms, that number increases to a 66 percent share of all life science Big Exits. This analysis accounts for any double dipping (if more than one top firm is involved in the exit, it only gets counted once). If we count every Big Exit for the top 10, these firms generate 128 exits—almost 13 Big Exits per firm. The takeaway here is that already a smaller subset of firms account for the vast majority of life science Big Exits. These are the firms that will be able to show enough exit activity to support raising their next fund.

2.) Quality New Deals, Attractive Existing Deal Flow 2.) Quality New Deals, Attractive Existing Deal Flow

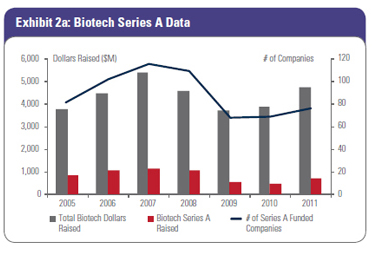

With a smaller set of solid, Big Exit-minded firms with newly committed capital, the number of companies funded will go down but the quality should go up. While the number of companies receiving Series A investment ($500,000-plus investment size is our criteria) has held relatively stable over the last two years (Exhibit 2a), our prediction is that we will likely see a 15-25 percent drop in the number of companies receiving their first round of equity investment over the next few years and through this current cycle.

The number of these newly funded companies will decline based on less capital available to deploy. However, valuations in these companies will be attractive for investors, as limited access to capital enables investors with fresh capital to be in an advantageous position to  negotiate equity valuations. In addition to creating new companies, the firms with this fresh capital have first look at the abundance of later-stage, VC-backed companies that have achieved technical goals but still need venture funding. There are more than a thousand life science companies that have been created since 2000 that are still private and likely need additional equity. Many of these companies have existing syndicates that are unable to support the company with additional equity to get to the next value inflection milestone. This presents a great opportunity for new, deep-pocketed capital to come in at attractive valuations. The subset of these older companies that attract fresh capital will move forward with advanced development and stand an increased chance of achieving quicker, high-multiple exits for the last-round investors. negotiate equity valuations. In addition to creating new companies, the firms with this fresh capital have first look at the abundance of later-stage, VC-backed companies that have achieved technical goals but still need venture funding. There are more than a thousand life science companies that have been created since 2000 that are still private and likely need additional equity. Many of these companies have existing syndicates that are unable to support the company with additional equity to get to the next value inflection milestone. This presents a great opportunity for new, deep-pocketed capital to come in at attractive valuations. The subset of these older companies that attract fresh capital will move forward with advanced development and stand an increased chance of achieving quicker, high-multiple exits for the last-round investors.

3.) Compelling Increase in Overall Exits

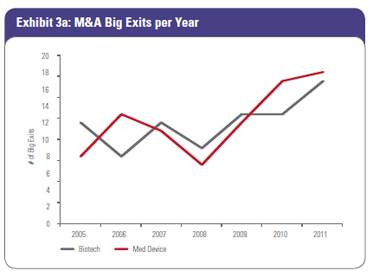

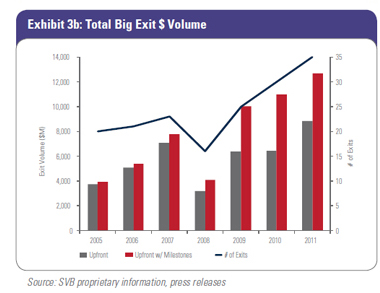

2011 was a great year for the number of biotech and device Big Exits (35) and total deal value ($12.7 billion). The number of Big Exits (Exhibit 3a) and Big Exit deal value with and without milestones (Exhibit 3b) have continued the upward trend between 2009 and 2011, with 2011 achieving the highest value in both categories since SVB started tracking this data in 2005. The three-year trendline shows increased exit activity and deal value. Specifically in biotech, the looming patent cliff, large cash reserves, and declining internal R&D of acquirers support the idea of building pipeline value from both early and later-stage venture-backed companies.

Since the transition to the structured-deal era in 2009, overall biotech Big Exit deal values have actually increased. In 2011, average upfront deals, excluding milestones, were $320 million and average total deal value, including milestones, was $519 million. 2011 also had the biggest number of biotech Big Exits, with 17. In device, the average upfront deal value in 2011 was $198 million, which compares very favorably to device total deal values from 2005 to 2008, but the number of device Big Exits in 2011 (18) dwarfs the average number of exits per year (10) achieved between 2005 and 2008. Trends in number and dollar volume continue to move up and to the right. Since the transition to the structured-deal era in 2009, overall biotech Big Exit deal values have actually increased. In 2011, average upfront deals, excluding milestones, were $320 million and average total deal value, including milestones, was $519 million. 2011 also had the biggest number of biotech Big Exits, with 17. In device, the average upfront deal value in 2011 was $198 million, which compares very favorably to device total deal values from 2005 to 2008, but the number of device Big Exits in 2011 (18) dwarfs the average number of exits per year (10) achieved between 2005 and 2008. Trends in number and dollar volume continue to move up and to the right.

4.) SVB Life Science LPI Index Points to Positive Industry Returns since 2009

Life Science Industry Returns – Introduction to SVB LPI Index Life Science Industry Returns – Introduction to SVB LPI Index

Acknowledging that we live in a sector where we are investing much more than we raise, a simple question emerges: Is the industry receiving value back from capital invested? We analyzed life science sector performance using a simple cash in/cash out, liquidity-to-invested capital analysis.

We created the SVB LPI Index to track life science venture performance year over year. “LPI” is defined as the ratio of liquidity to paid-in capital invested. The numerator (the liquidity part of the equation) tracks Big Exit upfront value. We do not include any milestones to be earned and also do not include any public market exits that provide returns to LS venture funds. We did not include milestones to be earned in order to provide a true measure of value returned at the close of the transaction—the “bird in the hand” analysis. While the IPO market and public market M&A are important sources of returns for investors, especially more recently on the biotech side, it is difficult to measure performance. We would rather understate the liquidity generated than overstate returns. The Big Exit liquidity number is a good indicator of private M&A value created, albeit a lower number than actual liquidity earned by life science funds. The denominator (the “paid-in capital invested” part of the equation) measures the amount of venture dollars invested into device and biotech companies per year.

The SVB LPI Index is merely an indicator of the health of the life science venture industry. In this overfunded sector, many who know life science would guess that the industry is investing substantially more into companies than it is receiving back in real exit value. The results in 2011 and over the last three years are surprising.

Substantial Positive SVB LPI Index in 2011, and Positive for the Industry Between 2009 and 2011

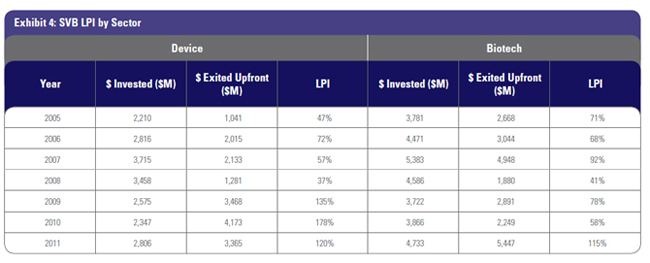

Even with the understated “liquidity” numerator and the overfunded “paid-in capital” denominator, the SVB LPI provides positive results. In 2011, the third-highest year in life science venture investment since 2005, the SVB LPI was positive in both device and biotech, with each clocking in with returns above 1.15X. This means that upfront Big Exit M&A value received (not including any to-be-earned milestones) was more than the substantial capital invested last year. The hot exit environment referenced earlier in this article is the reason for this positive SVB LPI, and points to a very viable upward trendline. Even more surprising, device has had a positive SVB LPI every year since 2009, with a very solid three-year SVB LPI of 1.44X. In a very difficult regulatory environment, and despite the perception of device investing as “challenged,” returns from venture-backed device companies are consistently beating capital invested.

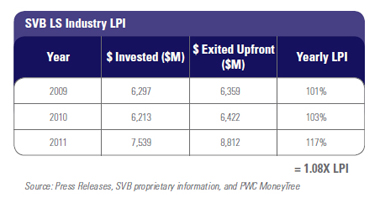

Over the last three years, the SVB LPI for the entire venture life science industry is positive at 1.08X. If we include to-be-earned milestones, the LPI grows to 1.7X. Strong results from the last three years do not substantially change the overall 10-year life science return data, but they do provide validation that the industry is achieving positive results. Investors looking at the 1.08X might not be impressed, but it is the trendline that is important here. For example, in 2005 device provided just over $1 billion in upfront Big Exit returns. Between 2005 and 2008 that number fluctuated from $1 to $2 billion per year. Since 2009, upfront Big Exit returns have grown significantly, achieving over $3 billion each year. Last year, biotech reached its highest value returned since we started tracking this data, at over $5.4 billion. This is a trendline to watch. Overall, 2011 was a banner year for venture-created liquidity, with $8.8 billion in value created just in upfront Big Exit values. Those who say there is no liquidity generated in venture life science are clearly mistaken.

However, a positive SVB LPI does not point to a vibrant, healthy life science venture industry as a whole. Combined with the data above showing that the majority of Big Exits cluster among a small group of funds, it points to a subsection of funds that are receiving an outsized portion of these distributions. As discussed earlier, these are the very funds that will be able to raise their next fund. However, a positive SVB LPI does not point to a vibrant, healthy life science venture industry as a whole. Combined with the data above showing that the majority of Big Exits cluster among a small group of funds, it points to a subsection of funds that are receiving an outsized portion of these distributions. As discussed earlier, these are the very funds that will be able to raise their next fund.

Summary: Good Time to Invest in Life Science

Indicators point to an increasingly attractive investment environment for investors with capital, as there will be less competition for funding great technologies. Less overall capital in the market translates to attractive valuations for investors. Big acquirers will continue to buy more, not less, at attractive valuations. We believe the SVB Life Science LPI will continue to be positive as capital deployed decreases and M&A appetite continues to be robust—especially in biotech, where poor R&D efficiency and patent cliffs will remain significant drivers for big pharma to keep acquiring. This should continue the trend of robust returns in the life science sector. Life science venture firms that recently closed a new fund or are able to fundraise in the next 12 months will be in prime position to reap these rewards. The first-mover advantage has arrived—the time to invest is now.

|

Jon Norris is a managing director with SVB Capital's Venture Capital Relationship Management team, specializing in life sciences. He oversees strategic relationships with select life science venture capital firms on the West Coast, sourcing and advising on direct equity co-investment, limited partnership, and portfolio company banking and lending opportunities. In addition, he helps life science companies with equity fundraising strategy. Jon may be reached at (650) 926-0126 or jnorris@svb.com.

|

1PricewaterhouseCoopers MoneyTree data, 2005-2011.

2PricewaterhouseCoopers MoneyTree data, 2005-2011.

[back to top]

Medical Device User Fee Amendments of 2012: A Fact Sheet

By David Hoffmeister, Partner (Palo Alto)

Medical device companies are required to pay medical device user fees—first established by Congress in 2002—to the U.S. Food and Drug Administration (FDA) when they (i) register their establishment and list their devices with the agency, (ii) submit an application or a notification to market a new medical device in the United States, and (iii) provide certain other submissions. The recently enacted Food and Drug Administration Safety and Innovation Act includes the Medical Device User Fee Amendments of 2012, or MDUFA III, which takes effect on October 1, 2012. MDUFA III will sunset in five years, on October 1, 2017. Ultimately, MDUFA III represents a commitment between the United States medical device industry and the FDA to increase the efficiency of the regulatory process in order to reduce the time it takes to bring safe and effective medical devices to the U.S. market.

MDUFA III is the result of more than a year of public input, negotiations with industry representatives, and discussions with patient and consumer representatives. Under MDUFA III, the FDA is authorized to collect user fees that will total approximately $595 million over five years. With this additional funding, the FDA will be able to hire more than 200 full-time-equivalent workers over the five-year course of MDUFA III.

In exchange, the FDA has committed to meet certain performance goals outlined in the Secretary of Health and Human Services’ letter to Congress (the MDUFA III commitment letter). Set forth below are some of the key provisions of MDUFA III.

Review Performance Goals

The MDUFA III commitment letter includes the following performance goals for FDA decision-making with respect to a variety of submission types:

- Original Pre-market Approval (PMA) Applications Not Requiring Advisory Committee Input – The FDA will issue a decision within 180 FDA Days for 70 percent of submissions received in FY 2013, 80 percent of submissions received in FY 2014 and 2015, and 90 percent of submissions received in FY 2016 and 2017.

- PMA Applications Requiring Advisory Committee Input – The FDA will issue a decision within 180 FDA Days for 50 percent of submissions received in FY 2013, 70 percent of submissions received in FY 2014, 80 percent of submissions received in FY 2015 and 2016, and 90 percent of submissions received in FY 2017.

For all PMA submissions for which a decision is not reached within 20 days after the applicable FDA-Day goal, the FDA will provide written feedback to the applicant to be discussed in a meeting or teleconference, including all outstanding issues with the application that are preventing the FDA from reaching a decision.

- 180-Day PMA Supplements – The FDA will issue a decision within 180 FDA Days for 85 percent of submissions received in FY 2013, 90 percent of submissions received in FY 2014 and 2015, and 95 percent of submissions received in FY 2016 and 2017.

- Real-Time PMA Supplements – The FDA will issue a decision within 90 FDA Days for 90 percent of submissions received in FY 2013 and 2014 and 95 percent of submissions received in FY 2015 through 2017.

- 510(k) Submissions – For submissions received in FY 2013, the FDA will issue a decision for 91 percent of submissions within 90 FDA Days. For submissions received in FY 2014, the FDA will issue a decision for 93 percent of submissions within 90 FDA Days. For submissions received in FY 2015 through 2017, the FDA will issue a decision for 95 percent of submissions within 90 FDA Days.

For all 510(k) submissions for which a decision is not reached within 100 FDA Days, the FDA will provide written feedback to the applicant to be discussed in a meeting or teleconference, including all outstanding issues with the application that are preventing the FDA from reaching a decision.

Shared Outcome Goals

The FDA and the medical device industry agreed to a joint commitment to reduce the total elapsed time from acceptance of a submission to an FDA decision on clearance of a 510(k) or approval of a PMA Application. The total elapsed time includes the time during which the submission is actively under review by the agency, as well as the time during which the submission is not under active review because the applicant is responding to FDA requests for additional information.

Improved Review Experience

The MDUFA III program is expected to result in enhanced accountability, predictability, and transparency for the medical device industry through a more structured pre-submission process, earlier interactions between the FDA and device applicants, and increased communication during the review process.

Independent Assessment of Pre-market Review Process

An independent consulting organization will evaluate the FDA’s pre-market review program and will recommend improvements to the program.

Process Improvements

- Submission Acceptance Criteria: To make the pre-market review process more efficient, the FDA will implement revised submission acceptance criteria through guidance. The guidance will include objective criteria for updated “refuse to accept”/”refuse to file” checklists that will be used to evaluate submissions when they are received to ensure that FDA resources are focused on reviewing complete submissions. These checklists will take effect once the final guidance is published.

- Interactive Review: The FDA continues to encourage—and is committed to continuing—informal communication between FDA staff and device applicants in order to collect appropriate additional information and meet review timelines. The MDUFA III commitment letter reaffirms the FDA’s and industry’s commitment to these interactions.

- Guidance Document Development: MDUFA III user fees will support the FDA’s development of guidance documents, published on the FDA’s website, which represent the agency’s current thinking on a topic. Under the MDUFA III program, the FDA will build an improved process for tracking guidance development and will communicate to both industry and the public the agency’s priority list of topics for guidance development.

- Third-Party Review: The third-party review program is intended to improve the efficiency and timeliness of the FDA’s 510(k) review processes for specific device types by having an accredited third-party reviewer conduct the primary review of a 510(k) submission and then submit the review to the FDA for final determination. MDUFA III reauthorizes the third-party review program.

- Patient Safety and Risk Tolerance: The FDA will fully implement final guidance on factors to consider when making benefit-risk determinations in medical device pre-market review. This guidance focuses on factors to consider in the pre-market review process, including patient tolerance for risk, the magnitude of the device’s benefit, and the availability of other treatments or diagnostic tests. Over the five-year course of MDUFA III, the FDA will meet with patient groups to better understand and characterize the patient perspective on disease severity and unmet medical needs. In addition, the FDA will increase its utilization of its Patient Representatives as Special Government Employee consultants to obtain patients’ views early in the medical product development process and ensure that those perspectives are considered in regulatory discussions.

- Emerging Diagnostics: Under the MDUFA III program, the FDA will work with industry to develop a transitional approach for the regulation of emerging diagnostics.

Strengthening FDA Infrastructure

The performance goals outlined in the MDUFA III commitment letter challenge the FDA to meet new milestones for pre-market review of medical devices and will require an investment in staff and technology. User fees will provide the FDA with additional resources to recruit, train, and retain employees with the expertise needed to meet these goals, as well as additional resources to update the agency’s information technology systems to facilitate the achievement of the performance goals.

[back to top]

Life Science Venture Financings for WSGR Clients

By Scott Murano, Partner (Palo Alto)

The table below includes data from life science transactions in which Wilson Sonsini Goodrich & Rosati clients participated during the second half of 2011 and the first half of 2012. Specifically, the table compares—by industry segment—the number of closings, the total amount raised, and the average amount raised per closing across the second half of 2011 and the first half of 2012.

Life Sciences Industry Segment |

2H 2011

Number of Closings |

2H 2011

Total Amount Raised ($M) |

2H 2011

Average Amount Raised ($M) |

1H 2012

Number of Closings |

1H 2012

Total Amount Raised ($M) |

1H 2012

Average Amount Raised ($M) |

Biopharmaceuticals |

15 |

235.91 |

15.73 |

13 |

115.97 |

8.92 |

Diagnostics |

11 |

59.36 |

5.4 |

8 |

31.03 |

3.88 |

Genomics |

2 |

18.28 |

9.14 |

2 |

8.35 |

4.18 |

Healthcare Services |

2 |

8.45 |

4.22 |

2 |

34.5 |

17.25 |

Medical Devices |

69 |

363.5 |

5.27 |

69 |

389.18 |

5.64 |

Medical Information Systems |

5 |

38.96 |

7.79 |

6 |

39.66 |

6.61 |

Miscellaneous |

1 |

2.9 |

2.9 |

2 |

1.49 |

0.75 |

Total |

105 |

727.36 |

|

102 |

620.18 |

|

The data generally demonstrates that venture financing activity declined during the first half of 2012 compared to the second half of 2011. Specifically, the total number of financings completed across all industry segments during the first half of 2012 decreased by approximately 2.9 percent compared to the second half of 2011, from 105 closings to 102 closings. More significantly, the total amount of money raised across all industry segments during the first half of 2012 decreased by 14.7 percent compared to the second half of 2011, from $727.36 million to $620.18 million.

Biopharmaceuticals, the second-largest industry segment, experienced one of the largest declines in total amount raised from the second half of 2011 to the first half of 2012, decreasing by 50.8 percent, from $235.91 million to $115.97 million. Similarly, diagnostics, historically the third-largest industry segment, suffered a large decline in total amount raised during the first half of 2012 compared to the second half of 2011, decreasing by 47.7 percent, from $59.36 million to $31.03 million. In contrast, medical devices, the largest industry segment—representing 62.8 percent of the total amount raised across all industry segments in the first half of 2012—experienced a marginal uptick in fundraising activity during the first half of 2012 compared to the second half of 2011, increasing by 7.1 percent, from $363.5 million to $389.18 million. However, it is worth noting that this total remains far below the $571.96 million raised by medical device companies during the first half of 2011.

In addition, our data suggests that Series A financing activity is down compared to later-stage equity financings and bridge financings. Specifically, the number of Series A closings as a percentage of all closings during the second half of 2011 compared to the first half of 2012 decreased from 33.02 percent to 21.82 percent, whereas the number of Series B closings during the same periods increased from 13.21 percent to 17.27 percent and the number of Series C and later closings increased from 19.81 percent to 20 percent. Moreover, there was a greater presence of venture-capital-led equity closings during the first half of 2012 compared to the second half of 2011 across all stages of investment. During those periods, the percentage of venture-capital-led Series A closings increased from 63.3 percent to 70.8 percent, the percentage of venture-capital-led Series B closings increased from 58.3 percent to 66.7 percent, and the percentage of venture-capital-led Series C and later closings increased from 68.4 percent to 80 percent.

Other data taken from transactions in which all Wilson Sonsini Goodrich & Rosati clients participated during the second half of 2011 and the first half of 2012 suggests a shift in investment money from life sciences to other industries. In the second half of 2011, life sciences was the most attractive industry for investment among our clients, representing 28 percent of total funds raised, followed by clean technology and renewable energy at 21.1 percent, and software at 15.6 percent. In the first half of 2012, software eclipsed life sciences as the most attractive industry for investment among our clients, increasing from 15.6 percent to 21.92 percent of total funds raised. Life sciences fell to second place, dropping from 28 percent to 19.12 percent of total funds raised, and was followed by clean technology and renewable energy at 14.97 percent.

Overall, the data confirms that access to venture capital for life science companies declined during the first half of 2012 compared to the second half of 2011. And while life sciences remains a popular industry for investment among our clients, it no longer stands as the highest-grossing industry for investment, likely due in part to the recent consolidation and loss of venture funds dedicated to life sciences. Attracting early-stage investment continues to be an uphill battle for many companies, but the upshot may be the increased presence of venture-capital-led financings at all stages, suggesting that those funds that do have money are leading more deals.

[back to top]

Eight Issues to Consider When Setting Company Policies for Trade Secrets and Employee Mobility

By Charles T. Graves, Partner (San Francisco)

One area of law that frequently causes problems for companies—and too often results in expensive litigation—is the law surrounding trade secrets, restrictive covenants, and other issues related to employee mobility. At the same time, paying attention to a few, mostly common-sense points can drastically reduce such risks. We present eight of these points here.

1. Watch Out for IP Ownership Terms in Business Contracts: Because many trade secret disputes involve departing employees, it is easy to forget that disputes also arise when business partnerships or license agreements fall apart. When companies share information, contract terms too often are fuzzy on who owns what when employees of one company modify, improve, or add to confidential information shared under a business contract. Paying attention to IP ownership terms in these types of contracts is important.

2. Use the Right Words in Employee Invention Assignment Contracts: Virtually every company uses employee invention assignments to protect inventions and trade secrets, and to be certain that the company will own any patents resulting from employee inventions. Outdated agreements may not contain the terms that courts deem sufficient to effect a present transfer of future inventions, however. Be certain that you use an up-to-date invention assignment agreement to avoid any ambiguity on this topic.

3. Enforce a Search-and-Purge Requirement for Incoming Employees: Too many lawsuits start because a new hire downloaded information from his or her former employer’s computer system before leaving. One way to cut down on this problem is to create a company policy where all new hires are instructed to search for—and return or destroy—anything belonging to a former employer before starting work.

4. Enforce a Search-and-Purge Requirement for Departing Employees: Just as incoming employees should be instructed to search for and return (or destroy) material belonging to former employers before beginning work, departing employees should receive a similar instruction to ensure that they return all company property before leaving. A written certification is a useful way to accomplish this goal.

5. Provide Meaningful Training for Incoming Employees: Employees sometimes do not understand the rules governing trade secrets and invention assignments and thereby create problems without meaning to do so. To help employees understand what they can and cannot use from prior jobs, as well as what they can and cannot take to future jobs, consider implementing workforce trade secret training sessions. A good time to do so is the date on which employee harassment and discrimination training is provided.

6. Be Aware of Regional Differences in Contract Terms: It is widely known that California does not permit employee non-competition covenants and places limits on the scope of customer non-solicitation covenants, but the laws of other states differ and few states take the same approach when it comes to these issues. Companies hiring employees from other states or that have employees in other states should be aware of state-specific rules and should not assume that a one-size-fits-all employment contract will work.

7. Take Clean Rooms Seriously: Companies often choose to develop their own technology after (or while) licensing similar technology from another company. To avoid trade secret accusations, companies should implement a proper clean-room process for truly independent development.

8. Hold on to Electronic Evidence: When employees leave, companies too often repurpose work computers immediately without performing checks for potential problems. Consider enacting a two-to-three-week hold period to preserve potential electronic evidence.

If you are contemplating discussions with a strategic partner where one or both sides will share confidential information, or if you need guidance on any issues relating to trade secret law or employee mobility, please contact a member of Wilson Sonsini Goodrich & Rosati’s life sciences practice or trade secret and employee mobility practice.

[back to top]

U.S. Commerce Department to Open Regional U.S. Patent Office in Silicon Valley

By Doug Portnow, Associate (Palo Alto), Jim Heslin, Partner (Palo Alto), and Esther Kepplinger, Chief Patent Counselor (Washington, D.C., and San Diego)

On July 2, 2012, Acting U.S. Commerce Secretary Rebecca Blank and Under Secretary of Commerce for Intellectual Property and Director of the U.S. Patent and Trademark Office (USPTO) David Kappos announced that additional regional USPTO offices will be opened in Dallas, Texas; Denver, Colorado; and Silicon Valley, California. Silicon Valley is a natural choice for the new office since about a quarter of all U.S. patent applications are filed from California and more than half of those are from Silicon Valley. Over half a million patent applications were filed last year.

The three new satellite offices are expected to open next year and will join the Detroit, Michigan, satellite office that opened on July 13, 2012. Thus, for the first time in its 200-year history, the USPTO will have offices outside of the Washington, D.C., metropolitan area. The new offices are required due to a provision in the recently enacted America Invents Act that mandates the establishment of regional offices in order to help modernize the U.S. patent system.

Six hundred cities applied to host the satellite offices or had recommendations filed on their behalf.1 The sites were selected following the review of 50 metropolitan areas, and the final decision was based on a number of factors, including geographical diversity, regional economic impact, ability to hire and retain employees, and ability to engage the intellectual property community. The regional offices will allow the USPTO to draw from local talent that previously was required to relocate to the Washington, D.C., area, enabling positions such as patent examiner and administrative patent judge to be filled. The establishment of satellite offices and the hiring of locally based individuals is expected to help with employee retention, as well as increase the quality of patent examination and reduce the backlog of over 600,000 patent applications that are currently in the queue awaiting examination.

Specific site selection and timelines for opening the new satellite offices have not been finalized, but the USPTO is required by law to open the offices by September 2014. It seems likely that the Silicon Valley office will be established in San Jose, California, but the USPTO only acknowledges that the new office will be in the general San Jose area. Other potential contenders include cities such as Santa Clara, Palo Alto, Cupertino, and Sunnyvale.

While operational details for the Silicon Valley office remain under development, the office is expected to have functions similar to those of the newly opened Detroit office. Patents will be examined in the satellite office and patent applicants will be able to have in-person examiner interviews—or video-conference interviews with examiners at other locations—and hold patent appeals or other patent reviews. This will allow local patent practitioners to conduct business more directly with the USPTO even if the decision makers are based in other offices, and may help facilitate a trend of decentralizing patent examination. It also will make the patent procurement process more convenient for patent applicants who otherwise would have to conduct business by telephone or fly back to Washington, D.C. The Silicon Valley office will be similar in size to the Detroit office, which is expected to have approximately 120 employees in its first year of operation. There are currently about 25 patent examiners and several administrative patent judges (APJs) assigned to the Detroit office, and roughly 75 more examiners are expected to be added over the next year.

Additionally, the technology that the new Silicon Valley office will handle has not been finalized. However, Esther Kepplinger, former Deputy Commissioner for Patent Operations in the USPTO (and WSGR’s current chief patent counselor), believes that the new office likely will focus on technologies related to the skill sets of the employees who can be hired in Silicon Valley. Thus, it seems likely that the Silicon Valley office will emphasize electronics, software, and biotech. This is encouraging for California patent applicants, but even assuming that the new office has the technical expertise to examine a patent application, there is no guarantee that a California-based patent applicant will be assigned to a patent examiner in the Silicon Valley office.

Though the patent community generally has been supportive of the new offices, some concern has been expressed. For instance, some believe that having regional patent offices will create different patentability standards among the different offices. Thus, what may be patentable in Detroit may not be patentable in Silicon Valley. However, USPTO training and internal quality assurance should ensure standardized procedures and examination.

The USPTO currently has about 6,000 patent examiners and therefore the hiring of only 100 or so new USPTO employees may not have a huge or immediate impact on reducing the backlog of patents or shifting prosecution to the West Coast, but it is a step in the right direction.

1 “Speed Is Goal for Patent Office,” San Francisco Chronicle, page D4, July 3, 2012.

[back to top]

Recent Life Sciences Highlights

Becton, Dickinson and Company Acquires Sirigen Group Limited

On August 27, 2012, Becton, Dickinson and Company (BD), a leading global medical technology company, announced that it has acquired Sirigen Group Limited, a developer of unique polymer dyes that are used in flow cytometry and can be applied to other technologies. The acquisition will expand BD’s life science research reagent platform. Wilson Sonsini Goodrich & Rosati represented Sirigen in connection with the transaction. For additional details, visit http://www.bd.com/contentmanager/b_article.asp?Item_ID=26845&ContentType_ID=1&BusinessCode=20001&d=&s=press&dTitle=

Press&dc=&dcTitle=.

CardioDx Completes $58 Million Equity Financing

Also on August 27, CardioDx, a pioneer in the field of cardiovascular genomic diagnostics, announced the completion of a $58 million two-tranche equity financing. The financing included Singapore-based investor Temasek, as well as existing investors Longitude Capital, Artiman Ventures, Kleiner Perkins, J.P. Morgan, Mohr Davidow Ventures, TPG Biotech, Intel Capital, Acadia Woods Partners, Bright Capital, Pappas Ventures, DAG Ventures, Asset Management Group, and GE Capital. WSGR advised Temasek in the financing. For more information, please see http://www.cardiodx.com/about-cardiodx/newsroom/press-releases/58-million-equity-financing.

Mylan and Pfizer Establish Exclusive, Long-Term Strategic Collaboration to Sell Generics in Japan

On August 22, 2012, Pfizer and Mylan announced that they have signed a definitive agreement establishing an exclusive, long-term strategic collaboration to develop, manufacture, and commercialize generic drugs in Japan. Earlier in August, Mylan Specialty, a subsidiary of Mylan, and Pfizer announced that Mylan Specialty had exclusively licensed its proprietary EpiPen products to Pfizer for the Japanese market as well. WSGR represented Mylan in connection with both matters. To learn more, please visit http://investor.mylan.com/releasedetail.cfm?ReleaseID=701929.

Fluidigm Prices $52.2 Million Public Offering of Common Stock

On August 16, 2012, Fluidigm Corporation, a supplier of microfluidic systems for growth markets in the life science and agricultural biotechnology industries, announced the pricing of an underwritten public offering of 3,660,000 shares of its common stock at a price to the public of $14.25 per share, for gross proceeds of $52.2 million. Wilson Sonsini Goodrich & Rosati represented Fluidigm in the transaction. Additional details are available at http://www.fluidigm.com/august162012.html.

Nodality Enters into Multi-Year Strategic Collaboration with Pfizer

On August 9, 2012, Nodality announced a strategic collaboration with Pfizer for the use of Nodality's proprietary Single Cell Network Profiling (SCNP) technology as a tool for the development of Pfizer compounds. The agreement establishes a multi-year, collaborative effort. Wilson Sonsini Goodrich & Rosati represented Nodality in the transaction. For more information, please visit http://www.nodality.com/company/news/pr017.phtml.

Amgen Completes Acquisition of KAI Pharmaceuticals

On July 5, 2012, Amgen announced that it has completed its $315 million acquisition of KAI Pharmaceuticals. The acquisition includes KAI’s lead product candidate KAI-4169, a novel agent being studied for the treatment of secondary hyperparathyroidism in patients with chronic kidney disease who are on dialysis. WSGR represented KAI Pharmaceuticals in connection with the transaction. To read Amgen’s press release, please see http://www.amgen.com/media/media_pr_detail.jsp?releaseID=1712187.

Practice Fusion Raises $34 Million in Series C Financing Round

On June 28, 2012, Practice Fusion, America’s largest physician-patient community, announced that it has secured a $34 million Series C round of financing led by Artis Ventures, with participation from longtime investors Felicis Ventures and Band of Angels, as well as Glynn Capital, Ali and Hadi Partovi, Founders Fund, Morgenthaler Ventures, Scott Banister, SV Angel, Ghost Angel, Barton Asset Management, and a number of other institutional and individual investors. WSGR advised Practice Fusion in the financing. More information can be found at http://www.practicefusion.com/pages/pr/artis-ventures-leads-emr-financing-round.html.

AstraZeneca Completes Acquisition of Ardea Biosciences

On June 21, 2012, AstraZeneca announced that it has completed its acquisition of Ardea Biosciences, a biotechnology company focused on the development of small-molecule therapeutics, for $1.26 billion. WSGR advised Ardea Biosciences on intellectual property matters associated with the acquisition. In addition, the firm represented Ardea's financial adviser, Bank of America Merrill Lynch. Additional information can be found at http://www.astrazeneca.com/Research/news/Article/20120620--az-completespartnering.

KineMed Announces Biomarker Discovery Collaboration with GlaxoSmithKline

On June 18, 2012, KineMed announced a multi-year R&D collaboration with GlaxoSmithKline that will apply KineMed’s proprietary biomarker discovery platform in therapeutic areas of interest to GSK. The collaboration will seek to identify, optimize, and validate novel biomarkers that would enable more informed and timely decision-making in clinical trials of compounds for muscle wasting, fibrosis, and metabolic diseases. WSGR represented KineMed in the matter. More information is available at http://www.kinemed.com/Media/Press_Release_KineMed_GSK_18_June_2012.pdf.

Auxogyn Raises $18 Million in Series B Financing

On June 5, 2012, privately held reproductive health company Auxogyn announced that it has raised $18 million through a Series B financing. The financing was led by new investor SR One and included participation from Series A investors Kleiner Perkins Caufield and Byers, TPG Biotech, and Merck Serono Ventures. WSGR represented SR One, the independent corporate venture capital arm of GlaxoSmithKline, in the transaction. For more information, please visit http://www.auxogyn.com/assets/press-releases/2012-06-05.series-b-financing.pdf.

Towers Watson Completes $435 Million Acquisition of Extend Health

On May 29, 2012, Towers Watson, a leading global professional services company, announced the completion of its $435 million acquisition of Extend Health, which operates the largest private Medicare exchange in the United States. WSGR represented Extend Health in the transaction. Further details are available at https://www.extendhealth.com/about/press-center/towers-watson-completes-acquisition-of-extend-health.

PneumRx, Inc. Acquires Key Assets from Broncus

On May 21, 2012, PneumRx, a medical device company dedicated to bringing innovation and improvements to the treatment of lung disease, announced that it has expanded its intellectual property portfolio by acquiring key patents and domain names from Broncus Technologies. Wilson Sonsini Goodrich & Rosati advised PneumRx in connection with the transaction. For more information, please see http://www.prnewswire.com/news-releases/pneumrx-inc-acquires-key-assets-from-broncus-152260025.html.

Mylan Secures Favorable District Court Ruling in Patent Infringement Case

On April 30, 2012, Mylan Inc. announced that its subsidiary Mylan Pharmaceuticals has launched the first generic version of Doryx® 150 mg tablets following a favorable decision by the U.S. District Court for the District of New Jersey in a patent infringement lawsuit brought by Warner Chilcott. Following a bench trial, the court held that Mylan’s product does not infringe the subject patent. WSGR represented Mylan in the matter. To read Mylan’s press release, please visit http://investor.mylan.com/releasedetail.cfm?ReleaseID=668717.

WSGR Earns Top Rankings from Dow Jones VentureSource, LMG Life Sciences,

and BioPharm Insight

Wilson Sonsini Goodrich & Rosati recently received third-party recognition for its achievements by Dow Jones VentureSource, LMG Life Sciences, and BioPharm Insight.

Dow Jones VentureSource’s recent legal rankings for issuer-side venture financing deals in the first half of 2012 placed Wilson Sonsini Goodrich & Rosati ahead of all other firms by the total number of rounds of equity financing raised on behalf of clients. The firm is credited as legal advisor in 157 rounds of financing, far outdistancing its nearest competitor, which advised in 86 rounds of financing.1 Of particular interest, Dow Jones VentureSource ranked WSGR No. 1 nationally for issuer-side deals in the healthcare2 and medical devices and equipment industries.

Also, several of the firm’s life-sciences-related practices were recognized in the inaugural edition of LMG Life Sciences, a guide published by the UK-based Euromoney Legal Media Group. Wilson Sonsini Goodrich & Rosati was “highly recommended” in the areas of patent prosecution, patent strategy and management, and licensing and collaboration, and “recommended” in the areas of corporate and competition/antitrust. Rankings for the 2012 edition of LMG Life Sciences were based on a review of nearly 1,000 interviews and surveys completed by individuals active in the life sciences industry.

In addition, WSGR ranked highly on several biotechnology and pharmaceutical league tables published by BioPharm Insight based on the value and volume of its licensing agreements. Select rankings include:

- Ranked No. 1 by global volume and No. 7 by global value of biotech and pharma licensing agreements in Q2 2012

- Ranked No. 1 by global volume and No. 2 by global value of biotech and pharma licensing agreements in the 12 months preceding June 2012

- Ranked No. 1 by volume and No. 2 by value of biotech and pharma licensing agreements in North America in the 12 months preceding June 2012

- Ranked No. 1 by volume and No. 8 by value of biotech and pharma licensing agreements in the Asia-Pacific region in the 12 months preceding June 2012

1As VentureSource continues to collect data and update its database, newly reported deals from a given time period may alter previously reported results.

2Healthcare consists of the biopharmaceutical and medical devices/equipment subsectors. |

[back to top]

Life Sciences Events

WSGR Hosts Successful 20th Annual Medical Device Conference

On June 21, 2012, Wilson Sonsini Goodrich & Rosati hosted its 20th Annual Medical Device Conference, at which a variety of industry experts addressed topics of critical importance to medical device companies today. More than 550 executives, entrepreneurs, investors, and in-house counsel from medical device companies attended the daylong event, which was held in San Francisco, California.

In a series of panels, industry CEOs, venture capitalists and other investors, industry strategists, investment bankers, and market analysts addressed such topics as venture and debt financing strategies, the complexities of commercializing medical device products in China, best practices for physician payments, patent due diligence, grant funding from the National Institutes of Health and the Department of Defense, recent changes to U.S. patent laws, and the current market for med-tech M&A and IPO transactions.

In addition, the event's lunch session featured an interview with representatives from Bard, a leading multinational developer of innovative medical technologies in the fields of vascular, urology, oncology, and surgical specialty products, and Lutonix, an early-stage medical technology company developing a proprietary drug-eluting balloon. The discussion, moderated by David Cassak, vice president of content and managing director of medical devices for Elsevier Business Intelligence, included David Gottlieb, Bard's senior vice president of strategy and business development, and Dr. Dennis W. Wahr, Lutonix's co-founder and former president and CEO. Topics of discussion included Bard's recent acquisition of Lutonix and Bard's increasingly active business development strategy.

Please visit http://www.wsgr.com/news/medicaldevice/conference-agenda.htm to view the conference agenda and access video and audio files of the presentations.

rEVOLUTION Symposium

October 3-5, 2012

The St. Regis Washington D.C.

Washington, D.C.

http://www.wsgr.com/news/revolution

Now in its seventh year, the rEVOLUTION Symposium has become the place to discuss the most important strategic problems facing pharma and biotech chief scientific officers. The event will examine the organization and management of R&D to uncover new disruptive discovery and development models and assess the continued impact of pricing, reimbursement, regulation, and globalization on our industry.

Phoenix 2012: The Medical Device and Diagnostic Conference for CEOs

October 11-14, 2012

Montage Laguna Beach

Laguna Beach, California

http://www.wsgr.com/news/phoenix

Phoenix 2012 will serve as the 19th annual conference for chief executive officers and senior leadership of medical device and diagnostic companies. The conference will provide an opportunity for top-level executives from organizations ranging from large healthcare to small venture-backed companies to discuss financing, strategic alliances, and other industry issues.

Wilson Sonsini Goodrich & Rosati’s Biotech Board of Directors Reception

January 9, 2013

Clift Hotel

San Francisco, California

The Biotech Board of Directors Reception is an exclusive networking event geared toward executives and directors of biotech companies.

Wilson Sonsini Goodrich & Rosati’s Medical Device Conference

June 2013

San Francisco, California

http://www.wsgr.com/news/medicaldevice

Wilson Sonsini Goodrich & Rosati’s 21st Annual Medical Device Conference, aimed at professionals in the medical device industry, will feature a series of panels and discussions addressing the critical business issues facing the industry today.

[back to top]

Casey McGlynn, a leader of the firm's life sciences practice, has editorial oversight of The Life Sciences Report and was assisted by Elton Satusky and Scott Murano. They would like to take this opportunity to thank all of the contributors to the report, which is published on a semi-annual basis.

|

Click here for a printable version of The Life Sciences Report

This communication is provided for your information only and is not intended to

constitute professional advice as to any particular situation.

© 2012 Wilson Sonsini Goodrich & Rosati, Professional

Corporation |