Winter 2008 By Brad Feld, Co-founder, Foundry Group

As a venture capitalist, I’m constantly on the receiving end of pitches from entrepreneurs looking for capital. Over time, I’ve found that these pitches fall into three categories: (1) The Introduction, (2) The First Shot, and (3) The Full Pitch. The same mistakes regularly appear in each category—following are some of the common ones and what you can do about them. The Introduction Don’t spam 157 VCs with a “Dear Sir” email. It’s bad enough to receive a generic email from someone; it’s even worse when they include all 157 recipients in the “To” line on the email. Remember to target your audience first and then personalize your emails to them. Oh—and if my name is “Brad,” please don’t send me an email that starts off “Dear Fred.” Don’t forget to know your audience. I invest in early-stage software and Internet companies in the United States. There is a lot of information about me (www.feld.com) and my firm (www.foundrygroup.com) on the Web. I’m always amazed when someone reaches out to me to invest in a telecom company, a retail products company, a clean tech business, or a biotech company. Do your research and make sure the VCs you target invest in the products or services your company provides. Don’t send a 73-page business plan via the U.S. mail. While this might have been the right approach in 1972, these days you should start with a short email that includes two or three paragraphs introducing you and your company. If you must, attach a short (less than four-page) executive summary. Make it easy for the VCs to either engage or say they aren’t interested. Don’t forget to include all of your contact information. I can’t tell you the number of times that I’ve received an email from someone without any contact info. It’s hard to take jimbofishcakes@msn.com seriously when they are asking for $17 million for a fast-growth software company but don’t include a URL to a real website or even an address or telephone number. And don’t forget your Twitter handle. The First Shot Don’t ask the VC to sign an NDA. This is a stupid idea perpetuated by lawyers. No reputable VC will sign a non-disclosure agreement. All you are doing is putting up a barrier to getting the VC’s attention and demonstrating your naiveté. Don’t use the wrong materials at the wrong stages. When you are raising money, you should have an arsenal of material ready to go. However, dumping it all on the VC with one big thud is rarely effective. Start off slow and spoon feed me. Give me access to a demo of whatever you are working on. Send me your PowerPoint presentation before we sit down to go through it so I have a chance to look at it and spend the time talking with you (if I want) instead of getting pitched.

Don’t name-drop other VCs. If I get interested in your company, I might ask you who else you are talking to, but don’t start off by name-dropping. It probably won’t have any positive benefit, and if I know the other folks you are talking to, I might reach out to them. If I hear they are lukewarm, or worse, have no idea who you are, you just blew it. Don’t list 27 advisors but only one co-founder. Advisory boards, especially at the very early stages of a company, are generally useless. Mentioning a few key advisors who have deep domain knowledge or experience in your industry is great, but a long list of lightly engaged people who have well-known names but aren’t really helping you takes away from your credibility. Don’t be obtuse or confusing. Often, I’ll read the first few paragraphs of an executive summary and say, “Huh?” At that point, I go into skim mode. At that point, you’ve done the opposite of “having me at hello.” Make it easy for me to understand what you do and why you think it is important.

The Full Pitch Don’t think there are rules that apply to all situations. Each VC is different. Do your research and learn what you can beforehand so you can fine-tune your approach to each VC. Don’t ramble. Showing up with a 57-page PowerPoint presentation and then trying to go through every slide is not good form. You should be able to tell your full story with no more than 15 slides. Keep it tight. Don’t forget to leave time for questions. Some VCs (OK, most VCs) will interrupt you during your presentation to ask questions. However, some will sit still and wait until the end. In either case, make sure you know how much time you have (ask in advance) and then assume the questions and answers will take up 50% of the time you have. If you finish early, that’s OK, as the VCs all have plenty of email to respond to. Don’t sell past the close. It’s usually obvious when the meeting is over. Let it be over. Don’t try to keep it going. Ask for the next steps, listen carefully, and then graciously say goodbye. If I’m interested, I’ll get back to you quickly. If you try to keep me in the room, I’m probably just going to get annoyed. And that’s not helpful to your mission. ______ Brad Feld has been an investor and entrepreneur for more than 20 years. He is co-founder of the Foundry Group, a venture capital firm focused on investing in early-stage information technology companies. Prior to his tenure at the Foundry Group, Brad had been a co-founder of Mobius Venture Capital and founder of Intensity Ventures. He also served as chief technology officer of AmeriData Technologies, a $1.5 billion publicly traded company that was acquired by GE Capital in 1996. Brad can be reached at brad@feld.com. How Do I Get Meetings with Investors? By Babak Nivi and Naval Ravikant, Founders, Venture Hacks “VCs are generally bombarded by requests for meetings, so a warm introduction helps an entrepreneur’s request float to the top of the list.” You’re not the only entrepreneur in the world who is trying to raise money. Investors get more requests for meetings than they can accommodate in this lifetime or the next. So they use introductions to prioritize and filter meeting requests. You could send investors a cold email, but your traction, team, or product better be mind-blowing—and it probably isn’t. Getting an introduction is a test of your entrepreneurial skills. If you can’t convince a middleman to make an introduction, how will you convince employees to join your company? How will you convince customers to buy from you? How will you convince investors to put their money in your pocket? So don’t spam investors with your business plan. Instead, convince middlemen to introduce you to investors. An effective middleman is simply someone investors listen to. Who makes the best introductions? Not all middlemen are created equal. The quality of the middleman helps investors prioritize meeting requests—it’s easier to land a meeting with a high-quality middleman, and if the middleman is weak, you won’t get a meeting. Who makes the best introductions? In rough order of effectiveness:

Use this list to measure a middleman’s potential. But the details of a middleman’s relationship with investors are more important than this list. So ask your middleman questions like: How do you know the investor? What have you done together? What companies have you sent him that he has subsequently backed? What makes our company interesting enough for you to make an introduction? Who makes the worst introductions? There are some introductions that hurt more than they help. First, investors who decline to invest in your company may offer to introduce you to other investors. An introduction by an investor who makes it a habit to invest in businesses like yours but doesn’t want to invest in you is a useless introduction. So skip these introductions if the first investor doesn’t have a good reason to not invest. Instead, ask the first investor whom he wants to introduce you to. Then get your own introductions to these investors. Second, you don’t want introductions from middlemen whom investors barely know. Or middlemen whom investors don’t trust. These introductions just make you look bad. Use the questions in the previous section to weed out these middlemen. If an introduction starts with “I don’t know if you remember me,” you’re in trouble.

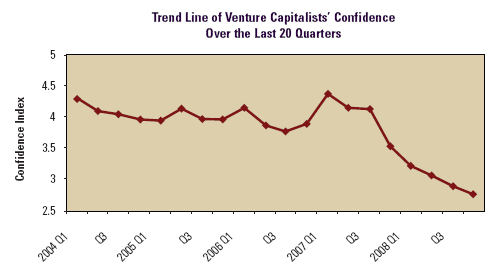

How do I get an introduction? Pick up the phone and call everyone you know who knows investors well and will listen to you. Call in all your favors to get the attention of middlemen. Explain why investors will appreciate the introduction by using your high-concept or elevator pitch. If you’re building an interesting company, people will offer to introduce you to investors. It makes them look good. In Hollywood, content is king. In Silicon Valley, deal flow is king. Get the middleman to focus on making a single great introduction. Three weak email introductions won’t do anything, but one strong phone call might. If you’re not having any luck convincing middlemen to make introductions, consider making them advisors as an incentive or reward. If that doesn’t work, ask the middleman to recommend investors or other middlemen: “Can you suggest just one person we should be talking to? We’ll find our own way to him or her, and we won’t use your name.” If you can’t find middlemen who know investors at all, start asking people, “Who do you know, who knows investors?” Finally, if you can’t get a single introduction to an investor who makes it a habit to invest in companies like yours, go back to the drawing board. Grow your company to the point where investors get interested. Go work at a start-up and make the right connections. Hang out in the lobby of conferences and develop the right contacts. Start blogging about your company. Sit down with your team and brainstorm about how to get introductions or grow your company to the point where you can get an introduction. And see Marc Andreessen’s “When the VCs Say ‘No’” for more advice: tinyurl.com/yutrb8. Nobody said this was fast or easy. What should I send middlemen? Send an elevator pitch that the middleman can forward to investors with a thumbs-up. Also consider attaching a deck. Don’t ask for a non-disclosure agreement from the investor or the middleman. Don’t send a business plan or executive summary. We cover all of these topics in Pitching Hacks. This is an excerpt from the book Pitching Hacks, available at http://venturehacks.com. ______ Babak Nivi and Naval Ravikant are the founders of Venture Hacks, a popular blog offering advice for entrepreneurs. In the course of their careers, they have founded companies like Epinions; helped start companies backed by Sequoia, Benchmark, Kleiner Perkins, and Atlas; worked at funds like Bessemer; and invested $20 million in companies like Twitter. They can be reached at team@venturehacks.com. Silicon Valley Venture Capitalists Confidence Declines to Lowest Level in Five Years By Mark V. Cannice, Ph.D., Associate Professor of Entrepreneurship, University of San Francisco Confidence among consumers, executives, and other constituents of our market economy has been closely monitored for years, as confidence is thought to be a necessary element for the proper functioning of our capitalist system. Over the last 18 months as the credit crisis has taken hold, confidence in our financial institutions clearly has been tested and continues to be questioned. While the sentiment of consumers and managers does play a significant role in our prosperity, confidence among the professional investors who advise and finance the high-potential new ventures that propel entrepreneurial growth is also critical to the long-run health and competitive advantage of the U.S. economy, as it is their investment decisions that determine, in large part, the pace of innovation in our nation. However, confidence among professional venture capitalists had not been systematically tracked. Beginning in early 2004, I began to gauge venture capitalists’ confidence in the future high-growth entrepreneurial environment in the San Francisco Bay Area with a quarterly survey and report. My expectation was that an ongoing indicator of VC sentiment could be informative to entrepreneurs who are seeking equity financing and also provide key insight to the functioning of our high-growth entrepreneurial economy. To date, I have completed 20 of these quarterly surveys and reports and thus can provide trend data in Silicon Valley venture capitalists’ confidence in addition to the current absolute level. Further, most of the responding venture capitalists provided additional insight into the reasoning behind their sentiment. The Silicon Valley Venture Capitalist Confidence Index (Bloomberg ticker symbol: USFSVVCI) for the fourth quarter of 2008, based on a January 2009 survey of 33 San Francisco Bay Area venture capitalists, registered 2.77 on a 5 point scale (with 5 indicating high confidence and 1 indicating low confidence). This quarter’s reading fell from the previous quarter’s reading of 2.89 to a fifth consecutive new low since the Index was originated in Q1 2004 and indicates a continuing downtrend in venture capitalists’ confidence.

The deepening global financial market turmoil and economic decline remained at center stage as a negative influence on venture capitalists’ confidence for the recent quarter. In particular, the beaten-down financial markets and the resulting negative impact of the liquidity prospects of most venture-backed portfolio firms weighed on confidence. This protracted delay of most liquidity events (both IPOs and M&As) has led to significant strain on the venture business model for the near term. While these ongoing concerns did predominate, a fundamental belief in the power of innovation, the prowess of entrepreneurs, and the unique strength of the Silicon Valley ecosystem for enterprise creation remained strong. In fact, several venture capitalists saw this harsh economic time as an ideal moment for thoughtful innovation and the creation of new products that would more directly solve customer needs. Timing, though, does appear to be central to sentiment. That is, while most respondents anticipate that 2009 will be another difficult year, the prospect of pent-up demand for new entrepreneurial ventures and investment alternatives is expected to surface by 2010. While the exact nature of the reemergence remains to be seen, lower valuations of new ventures, a laser focus on positive-cash-flow operations, and the long-term perspective of patient venture capital bodes well for an eventual recovery. Still, with the quarterly confidence index at its lowest point in its five-year history, the coming months and quarters appear to present a very challenging venture environment. Caution has grown with the continued unraveling of the broader financial system, but hope for the medium term remains. Kirk Westbrook of invencor was concerned over the ongoing economic environment but impressed by the robust government response. He stated, “Although I believe the global economy slid to the edge of the precipice during Q4 08, I am encouraged that the atypical and expeditious reactions by governments around the world may have prevented a fall into a much darker, 30’s era economic crevice. . . . Disciplined cash focus will be mission critical, but those concerns that are good at both the management and the articulation of the value proposition will likely see opportunity in a less-cluttered environment as they move toward mid-2009.” Stemming from the public market decline is the decreasing availability of liquidity events for venture-backed firms. To this point, Igor Sill of Geneva Venture Management argued, “We have certainly hit the low ebb of a very dry cycle period for venture liquidity as measured by IPOs. . . . With this liquidity void, we will see few, if any, new venture firms emerging, and frankly, few fundraising efforts from established firms. Some will even close down. We’ll be trying to salvage, sell, or merge the promising start-ups and dispensing with those requiring too much runway and capital to break even. As for new start-ups getting first-round funding, it will be tough going.” Some responding venture capitalists envisioned that a new direction for the venture capital industry may emerge from the macro economic malaise. For example, Joe Mandato of De Novo Ventures stated, “Given the uncertainty in the environment, the industry is trying to figure out what its course should be in the face of this environment.” And Dan Lankford of Wavepoint Ventures explained, “[T]here is a good chance that the venture industry is ‘de-evolving’ toward its roots of small, early-stage funds where the partners made most of their money from capital appreciation.” A Darwinian perspective was offered by some venture capitalists who expect that the current harsh environment will help identify the strongest firms with sustainable business models that make for good venture investments. For example, Eric Buatois of Sofinnova Ventures said, “In these difficult times, only strong and motivated entrepreneurs building companies on very strong foundations will get funding. We are likely to see very strong companies created in the next two years.” And confidence in the ability of entrepreneurs to continue to innovate and in the Silicon Valley ecosystem remained strong. For instance, David Spreng of Crescendo Ventures declared, “Silicon Valley innovation and entrepreneurial spirit will help America lead the way out of economic crisis beginning in 2009, sooner than most people think.” And Shomit Ghose of Onset Ventures reasoned, “The macro economy is looking like the ‘08 Detroit Lions, with no hope of recovery till 2010 at the earliest. But Silicon Valley continues to produce entrepreneurs with the talent and drive of the ‘72 Dolphins. There are daunting challenges in the next 18 months, to be sure, but there’s also reason for optimism over the long term.” To conclude, the continuing fallout from the credit crisis and downward economic spiral (lack of exits, squeezed capital commitments, and fewer customers for portfolio firm products) has led to the lowest level of venture capitalists’ confidence in the five-year history of this quarterly survey. Expectations for an ongoing malaise in the public capital markets and a shrinking economy portend a continued difficult operating environment for new growth enterprises and their venture backers. As some respondents have suggested, the intense economic pressures on several aspects of the venture business model may necessitate an eventual adjustment to it. And entrepreneurs, given lower public valuations, a longer holding period to liquidity, and fewer bidders, can expect more modest valuations for their enterprises. However, current increasingly stringent financing criteria and lower valuations may mean that many of today’s investments eventually will earn significantly positive returns. Further, a confidence in the resilience of entrepreneurs and the unique support structure of the Silicon Valley entrepreneurial ecosystem remains strong. This underlying confidence coupled with the belief that even stronger enterprises, tried by fire in this harsh environment, will emerge more vibrant and sustainable when the broader economic environment finally recovers, leaves cause for optimism in the long-term resilience of the Silicon Valley venture capital and entrepreneurial machine. The complete Q4 report and historical reports may be seen at www.Cannice.net. ______ Dr. Mark Cannice is an associate professor of entrepreneurship at the University of San Francisco, where he has taught since 1996. He also is the founder and executive director of the USF Entrepreneurship Program. Mark publishes a quarterly report on Silicon Valley VC confidence that has been widely referenced in the business media (including the Wall Street Journal, New York Times, Bloomberg, Reuters, Investor’s Business Daily, USA Today, etc.), as well as a similar report on China VC confidence. His articles on venture capital and technology management appear in numerous academic journals; he has co-authored a textbook in global and entrepreneurial management (published by McGraw Hill in four languages); and he is a contributing writer for The Industry Standard. Mark can be contacted at cannice@usfca.edu. From the WSGR Database: Financing Trends By Doug Collom, Partner (Palo Alto Office) With the continuing turmoil in the national economy, the fourth quarter of 2008 witnessed a significant decline from previous quarters in the number of equity financings that were completed. Although the venture capital industry has not been impacted nearly to the degree experienced by private equity as a discrete asset class, it is apparent that no asset class and no industry sector are immune from the recessionary forces that have gripped the current financial markets. The backdrop for venture activity levels in the fourth quarter of 2008 and continuing into the first quarter of 2009 includes a number of well-publicized and alarming developments:

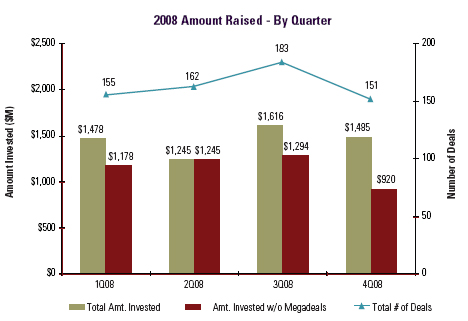

These developments all clearly have had a negative effect on the investment climate for the start-up company, and the data from the financing transactions captured in our database is further evidence of the impact of these developments. The number of financing transactions of all types declined from a peak of 183 in the third quarter of 2008 to 151 in the fourth quarter, representing a falloff of almost 20%. There was also a decline in the aggregate dollar investment in the fourth quarter. The data in the chart below includes the number and dollar amount of transactions resulting from a category of “megadeals,” i.e., single financing transactions each involving an amount in excess of approximately $100 million. If this megadeal category (three transactions in the third quarter, and three transactions in the fourth quarter) is eliminated from the data, then the fourth-quarter decline in the aggregate dollar investment for financing transactions is even more dramatic.

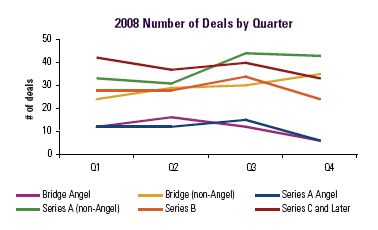

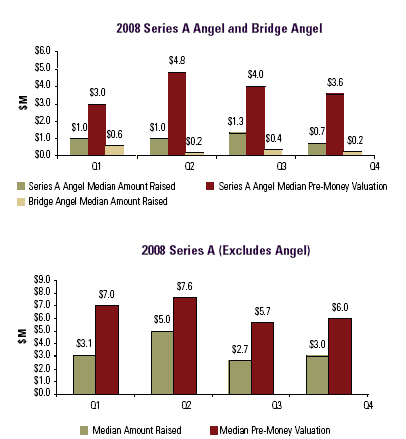

As indicated by the chart below, the number of Series A financing rounds by angels and angel groups for the fourth quarter is down significantly when compared with the third quarter of 2008. The decline in both the amount raised—a median of $700,000 compared with $1.3 million—and the pre-money valuation—a median of $3.6 million compared with $4.0 million for the previous quarter—is also notable. Similarly, there were six angel bridge transactions in the fourth quarter, representing half of the angel bridge transactions from the previous quarter. These declines in equity and debt financing transactions may be attributed to a number of possible causes, including the decline in personal net worth among individual angel investors as well as a growing sense of conservatism in the suitability of investments that even angel investors are willing to consider.

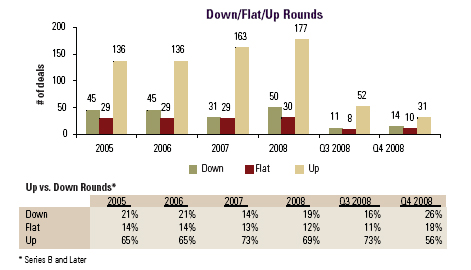

Similarly, the number of Series B as well as Series C and Later financing rounds for the fourth quarter also has dropped materially when compared with the previous quarter. It is likely that these decreases in levels of activity are attributable to heightened conservatism and risk aversion, increased time dedicated to the diligence undertaken by venture firms prior to making an investment, and perhaps other factors as venture firms manage the deployment of capital to their existing portfolios of companies that, in general, are looking at a prolonged period of operations before the likelihood of an acceptable exit transaction. In contrast to these clearly downward trends, the first round of equity financing by an institutional investor (i.e., not an angel round)—the true Series A equity financing round—for the fourth quarter appears in the aggregate to compare favorably with the activity levels for the third quarter of 2008. Not only does the fourth quarter log in on parity with the previous quarter as to number of financings—43 financings compared with 44 financings from the previous quarter—this data for the fourth quarter is approximately 30% higher than for the first or second quarters of 2008. We believe that the first quarter of 2009 will provide a more definitive view of the trend line for this stage of financing transactions. Not surprisingly, non-angel bridge transactions are on the rise in this difficult economic environment, with 114 bridge financings for 2008 compared with 61 for 2007. In the fourth quarter of 2008, there were a total of 25 bridges, compared against 18 for the same period in 2007. All of these bridge transactions were executed for the purpose of providing additional capital between investment rounds (i.e., not for seed-round financings for raw start-up companies). Bridge transactions, consisting of convertible debt, typically are used where previously funded companies needing additional working capital have little success in locating an outside investor to lead a new equity round. In these circumstances, if the company is to remain viable, the existing investors have no choice but to put up an additional investment, usually in the form of convertible notes, until an outside investor can be identified to lead an equity round. On a similar note, the number of “down-round” financing transactions—transactions where a company’s valuation declines from the last round, resulting in a price per share of the new security that is less than the price of the preferred stock issued in the last round—is on the rise. In the fourth quarter of 2008, the number of down-round transactions (including down rounds that included a complete capital restructuring of the company) as a percentage of all equity financing transactions jumped to 26%, from 16% in the previous quarter. Similarly, flat rounds, i.e., equity rounds that are priced at approximately the same price as the previous round, jumped to 18% in the fourth quarter compared with 11% in the previous quarter. Again, this data relating to flat- and down-round financings follows from all the challenges faced by the business community in the national and global economies—deterioration of the customer base, declining customer budgets for product purchasing, lack of available credit, pressure on product pricing, and the like—compounded by fewer exits, longer exit horizons, and lower exit valuations. This trend also may find some explanation in the depressed level of venture activity evidenced by the data in the fourth quarter of 2008. With a lower level of venture activity in the early-stage company sector, in effect, the demand-and-supply dynamics for investment money are fundamentally altered.

In the charts below, we show median amounts raised against median pre-money valuation, broken down by series of equity financing. The fourth quarter of 2008, compared with previous quarterly periods during the year, reflects notable declines in numbers for Series A angel rounds and for Series B rounds. The median amounts raised in angel bridge transactions are not predicated on a pre-money valuation.

In contrast, the median amount raised and pre-money valuation actually have increased slightly in non-angel Series A rounds. In Series C and Later rounds, while the median amount raised has decreased slightly, the median pre-money valuation has increased 27% against the previous quarter. Although the data for the Series C and Later rounds for this purpose includes financing transactions in the megadeal category, the effect on the median data is not material. We would expect to develop a better sense of the trend lines across these different financing phases in the first and following quarters of 2009.

The data in the tables above not surprisingly signifies a major shift in the investment climate that, while beginning in earlier quarters in 2008, became fully apparent by the fourth quarter. Early returns for the first quarter of 2009 indicate that the intensity of this shift is continuing and is likely to continue well into the current year. Outsourcing: A Tool for Survival By Suzanne Bell, Partner (Palo Alto Office), and Daniel Stevenson, Associate (Seattle Office) In an economic environment where virtually every CEO’s mandate includes cost-cutting, smart and strategic use of outsourcing may differentiate companies that survive this downturn from those that will not make it. Outsourcing is not a new cost-saving strategy, but over the last decade, the outsourcing-service-provider market has matured in a way that makes outsourcing an option for companies of all sizes. Niche-focused service providers have emerged, offering outsourcing possibilities that previously were not available to start-up companies. What Is Outsourcing? Ask 10 people what “outsourcing” means and you are likely to get 10 different responses. Part of the reason for this is that outsourcing covers many different areas. For one respondent, it may mean manufacturing, for another it may mean a help desk, while for another it may mean payroll processing. At its essence, outsourcing is hiring a service provider to do something (anything from hosting data to software development to customer service) that the company could do for itself, but is better and less expensively done by the service provider. Because outsourcing can be integrated into a company’s strategy in many different ways, there is no one-size-fits-all answer for what and how a company should outsource. Successful outsourcing arrangements are founded on a careful evaluation of what functions the company is currently performing that could be done better and less expensively by a service provider. Does Outsourcing Really Result in Cost Savings? Outsourcing in general has proven to be an effective cost-saving strategy because it gives a company access to less-expensive work forces and allows the company to delay upfront capital investments. In a recent study by Deloitte Consulting, 83% of the 300 executives participating in the study reported that their outsourcing projects met their ROI goals of more than 25%.1 These responses suggest that outsourcing certainly can be a powerful cost-saving tool. To increase the likelihood of realizing a company’s ROI goals, it is important to keep track of hidden costs (e.g., travel, vendor selection, and legal fees, as well as transition costs) when modeling an outsourcing arrangement.

Additional Reasons to Outsource In addition to cost savings, there are other compelling reasons to outsource. In many instances, these reasons provide companies with the greatest ability to differentiate themselves from competitors through outsourcing. They include:

Outsourcing Can Be Scary As great as outsourcing can be for a company’s bottom line, it is not without its risks. Careless outsourcing can irreversibly affect a company’s culture, damage customers’ perception of a company’s products, and heighten the risk of losing intellectual property. Outsourcing may be what a company needs to make it through this downturn, but careful execution is crucial to avoiding the risks and reaping the rewards of a successful strategy. Keys to Successful Outsourcing Given that outsourcing is, or will likely be, a key component of most companies’ cost-saving strategies, here are some important issues to consider: Plan with the big picture in mind. Almost every company can find additional cost savings through outsourcing, but some types of outsourcing, regardless of the potential cost savings, will not be a good fit for certain companies. To find the right fit, a company should consider where its core competencies and greatest competitive advantages lie. Functions and processes that don’t fall within the core-competency circle are all candidates for outsourcing. In many instances, after some internal evaluation, it makes sense to seek the help of a consultant who specializes in outsourcing to help maximize the value the company can find. Watch out for legal pitfalls. Each outsourcing transaction needs to be considered for its particular legal issues, of course, but there are certain legal pitfalls that tend to apply to most outsourcing arrangements. Perennial legal pitfalls include: (1) data privacy laws, (2) employment laws, (3) export controls, and (4) intellectual property protection. These issues can be especially thorny in international transactions. For example, under the European Union Data Privacy Directive, which is implemented independently by each EU member state, personally identifiable information about an employee or customer who is a citizen of the EU can only be transferred to another country that has privacy laws as protective of personal data as the EU. Because U.S. law is not deemed to provide EU-level protection to personal data, transfer of this information to the U.S. (or to typical offshoring locations) needs to be handled in a particular manner.

Select the right vendor. Just as when a company hires an employee, there needs to be a good cultural match when selecting an outsourcing vendor. Identifying the right vendor requires good due diligence, including checking references and, in some cases, a competitive bidding and parallel negotiation process. The information learned in the solution architecture and contract negotiation process regarding the vendor’s attitude and approach to risk-sharing should not be discounted, as these traits are often magnified after contract-signing. In the Deloitte Consulting study referenced above, of the executives who were not very satisfied with outsourcing, 55% wished they had spent more time on vendor evaluation and selection. Describe the services carefully. The scope of services in an outsourcing agreement typically is set forth in a statement of work. Sometimes clients are tempted to handle a statement of work without help from their legal counsel because such statements “contain only business terms.” But experience shows that most disputes arising from an outsourcing agreement can be tied back to a disagreement over the scope of the services. Allowing legal counsel to carefully review the statement of work to make sure the services are clearly described can help identify potential areas of disagreement and eliminate them. Create flexibility in the agreement. An outsourcing agreement needs to be dynamic and flexible. Conceptually, from a cost-saving standpoint, one of the greatest advantages of outsourcing is that the company should only pay for what it uses. In most cases, the pricing in the agreement should reflect this advantage with variable pricing based on consumption. Additionally, a good outsourcing agreement needs to account for changes and improvement to the services, acquisitions and divestitures by the company, and termination rights. Build a contract that delivers early warning of potential failure points. A well-drafted outsourcing agreement is a living document. Rather than being stashed in a drawer after signature, the outsourcing agreement should be used as a ready-reference handbook setting the parameters to guide the parties through day-to-day operations. Through well-crafted service levels, reporting policies, and governance procedures, the contract should flag issues well before they get out of hand, provide incentives for the service provider to resolve issues quickly, and give both parties ample opportunity to get things right before business operations are adversely affected. Focus on transition. Transition is the phase in which the work that was being performed inside the company is transferred to the service provider. Like an airplane takeoff on a runway, the transition stage is crucial in an outsourcing agreement. A successful launch requires careful planning and communication, much of which happens after the contract is signed. Because of the politics that can be involved with an outsourcing agreement, a failed transition can result in much more harm than just the lost time and transition fees. Doomed launches are often marked by an over-reliance on the service provider and ignoring milestones and other critical deliverables that were agreed to in the contract. Manage the contract after signature. Successful outsourcing requires careful management of the relationship after signature of the agreement. In many ways, the outsourcing vendor needs to be managed like an internal division of the company would be managed. Because management of the agreement will have a dramatic impact on the overall success of the arrangement, the manager should be chosen carefully, keeping in mind that the skills required to manage the vendor often differ from the skills required to perform the services themselves. While the risks of outsourcing are real, the opportunity for start-ups to successfully leverage outsourcing never has been greater. If implemented thoughtfully and carefully, outsourcing can be a powerful cost-saving strategy that can help companies get more out of their money and maximize their competitive advantages. 1“Why Settle For Less?,” Deloitte Consulting 2008 Outsourcing Report, Deloitte Development LLC, 2007 Avoiding Trouble: Provisions in Previous Employment Documents that Every Start-Up Company Founder Needs to Review By Yokum Taku, Partner (Palo Alto Office) A potential founder of a start-up company needs to review various documents they signed with their previous employers in order to avoid unnecessary problems in the future. Most employees have signed an offer letter and a confidential information and invention-assignment agreement, as well as other documents such as a stock option agreement. Depending on the company and the employee, other relevant documents might include an employment agreement, an employee handbook, a conflict-of-interest policy, or a severance/separation agreement. These documents should be reviewed carefully for provisions that may inhibit the activities of the future start-up company. Enforceability of some provisions in these documents, such as non-compete clauses, generally depends on the state where the employee is located. Founders should review the relevant documents for the following provisions and consult with legal counsel: Confidentiality. All technology companies require employees to sign a confidentiality agreement that prevents employees from using or disclosing employer confidential information except for the benefit of the employer. These confidentiality provisions are usually for an indefinite period of time, as opposed to a finite period such as five years in a typical confidentiality agreement between companies. In any event, most states prohibit the misappropriation of trade secrets as a matter of law, regardless of whether or not the employee signed a confidentiality agreement. Thus, a potential start-up company founder needs to ensure that he or she does not use former employer confidential information in connection with the new company. Invention assignment. All technology companies also require employees to assign inventions created during employment to the employer. In California, there is an exception to this requirement to assign inventions if: Some companies may have invention-assignment clauses that require the employee to assign inventions created for a certain period of time after termination of employment, such as from six months to a year. These clauses may be enforceable depending on the state and the facts and circumstances of the situation. Invention disclosure. Even if an employer does not require post-termination invention assignment, some employers include provisions in standard documents that require the employee to disclose inventions created (or patents filed) for a certain period of time after termination of employment. This is less common and may be enforceable if it is reasonably necessary to protect the company’s business interests. Non-compete clauses. In many states, non-compete clauses are enforceable if they are reasonable in scope and duration. However, non-competes are generally not enforceable in California except for limited exceptions, including in connection with the sale of a business. Therefore, most start-up companies located in California do not have non-compete provisions in their standard employee documents. If a potential start-up company founder is subject to a non-compete, the founder needs to review carefully the scope and time period of the non-compete. Non-solicitation of customers and vendors. Some employment documents also include a prohibition on soliciting the employer’s customers and vendors. In states like California where non-competes are generally not enforceable, provisions on non-solicitation of customers and vendors are likely to be considered a restraint on trade and also not enforceable. Non-solicitation of employees. Most technology companies require employees to refrain from soliciting employees for a specified term, such as one year after termination of employment. Thus, start-up companies where founders intend to hire their former co-workers need to carefully navigate the bounds of permissible action under these clauses. Please also note that key employees of a company may be subject to fiduciary duties to the company and may be subject to claims of breach of fiduciary duty, fraud, and intentional interference with contract for soliciting co-workers even in the absence of written agreements. No moonlighting. Some employment documents contain explicit provisions that prevent employees from working on business activities unrelated to their employer, even if it is after hours. This may limit pre-resignation activities of the potential founder. No conflicting stock ownership or directorships. Some company conflict-of-interest policies prevent an employee from investing or holding outside directorships in other companies. This may limit pre-resignation incorporation of a new company. Potential start-up company founders need to be aware of these issues and identify them for their legal counsel as soon as possible prior to starting a new company. ENTREPRENEURS COLLEGE In 2006, Wilson Sonsini Goodrich & Rosati launched its Entrepreneurs College seminar series. Presented by our firm’s attorneys, the seminars in each session address a wide range of topics designed to help entrepreneurs focus their ideas and business strategies, build relationships, and access capital. In response to attendee demand, there also are occasional additional sections that address issues of concern to particular industries. Currently offered every spring, the sessions are held at our Palo Alto campus and are webcast live to our national offices. These events are available to entrepreneurs and start-up company executives in the Wilson Sonsini Goodrich & Rosati network, which includes leaders in entrepreneurship, venture capital, angel organizations, and other finance and advisory firms. For more information about our Entrepreneurs College and other programs, please contact Norilyn Ingram. SPRING 2009 SESSION Overview & Valuation, April 8 Business Plans & Fundraising, April 22 Forming & Organizing the Start-Up & Founders Stock, May 6 Compensation & Equity Incentives, May 20 Intellectual Property, June 3 Term Sheets, June 17 Clean Tech Session, July 1 Exits & Liquidity, July 15 Biotech Session, July 29 Click here for a printable version of The Entrepreneurs Report Editorial Staff: Doug Collom, editor-in-chief (Palo Alto Office); Mark Baudler (Palo Alto Office); Herb Fockler (Palo Alto Office); Craig Sherman (Seattle Office); Yokum Taku (Palo Alto Office)

This communication is provided for your information only and is not intended to © 2009 Wilson Sonsini Goodrich & Rosati, Professional Corporation |